S&P Global Ratings Downgrades Colombia to BB- Amid Fiscal Concerns

Credit downgrade is an indictment of the Petro administration’s fiscal management, including suspension of the fiscal rule.

On April 8, 2026, S&P Global Ratings (NYSE: SPGI) lowered its long-term foreign currency sovereign credit rating on Colombia to BB- from BB and its long-term local currency rating to BB from BB+. The outlook for both ratings is stable, reflecting expectations that the Government of Colombia will gradually reduce its fiscal deficit while sustaining moderate growth in the national gross domestic product.

The rating action follows persistent fiscal imbalances and a policy environment that has become less predictable since the pandemic-related recession. The government decision to suspend the national fiscal rule in 2025 marked a significant shift in the policy framework. Pro-cyclical fiscal policies have provided marginal support for employment and consumption, but have also contributed to higher inflation expectations and a wider current account deficit. S&P expects the general government fiscal deficit to reach 5.6% of the national gross domestic product in 2026, compared to 5.3% in 2025.

“We expect Colombia to have consistently large fiscal deficits over the next few years.” — S&P Global Ratings

Institutional stability remains a key factor in the rating, though challenges persist. A fragmented legislature followed the March 2026 elections, where Pacto Histórico and Centro Democrático emerged with the largest minorities. The upcoming presidential election, scheduled for May 31, 2026, adds further uncertainty. Candidates such as Iván Cepeda of Pacto Histórico, Paloma Valencia, and Abelardo de la Espriella have proposed varying approaches to fiscal consolidation. The new administration will inherit spending pressures related to domestic security, rising healthcare costs, and pension payments linked to minimum wage increases.

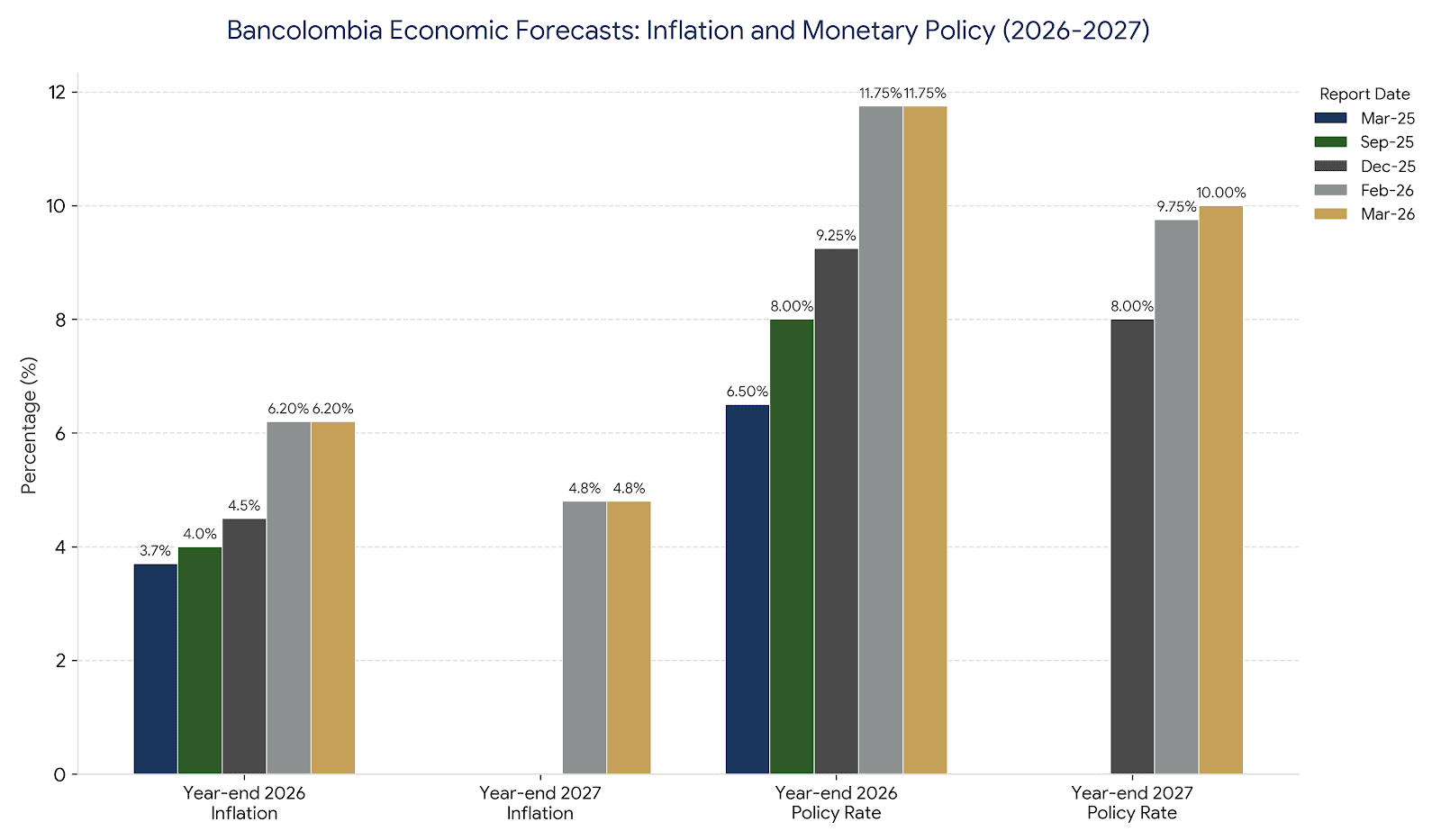

The Banco de la República, the independent central bank of the country, has maintained a tight monetary policy to combat inflationary pressures. Annual inflation reached 5.3% in February 2026, prompting the bank to increase reference rates to 11.25%. S&P anticipates that inflation will not return to the target range of 3% +/- 1% until early 2029. While the independent status of the central bank provides a buffer against external shocks, high interest rates and lower-than-expected revenue collections have contributed to the widening deficit since 2024.

Economic growth is projected at 2.5% for 2026, slightly below the 2.6% recorded in 2025. Per capita growth is estimated at $9,900 USD for 2026, with real growth expected to average just above 2% through 2029. Despite being a net energy exporter, the performance of the US economy and international energy prices continue to influence national outcomes. Hydrocarbon exports declined to 35% of goods exports in 2025, down from 67% in 2013, showing some diversification even as the sector remains a primary source of volatility.

Net general government debt is forecast to approach 66% of the national gross domestic product by 2029, rising from 60.4% in 2025. S&P notes that the government interest burden will average 12.3% of general government revenue over the next three years. The shift toward issuing shorter-term debt instruments has reduced reported interest payments but increased vulnerability to interest rate fluctuations. External indicators remain a concern, with narrow net external debt expected to stabilize at 130% of current account receipts through 2029. Foreign direct investment is expected to be the primary source for funding the current account deficit, which is projected to stabilize around 2.6% of the national gross domestic product.

Vise photo credit © Loren Moss