Twenty-Year Debt Arc Resets Colombia’s Sovereign Risk Outlook

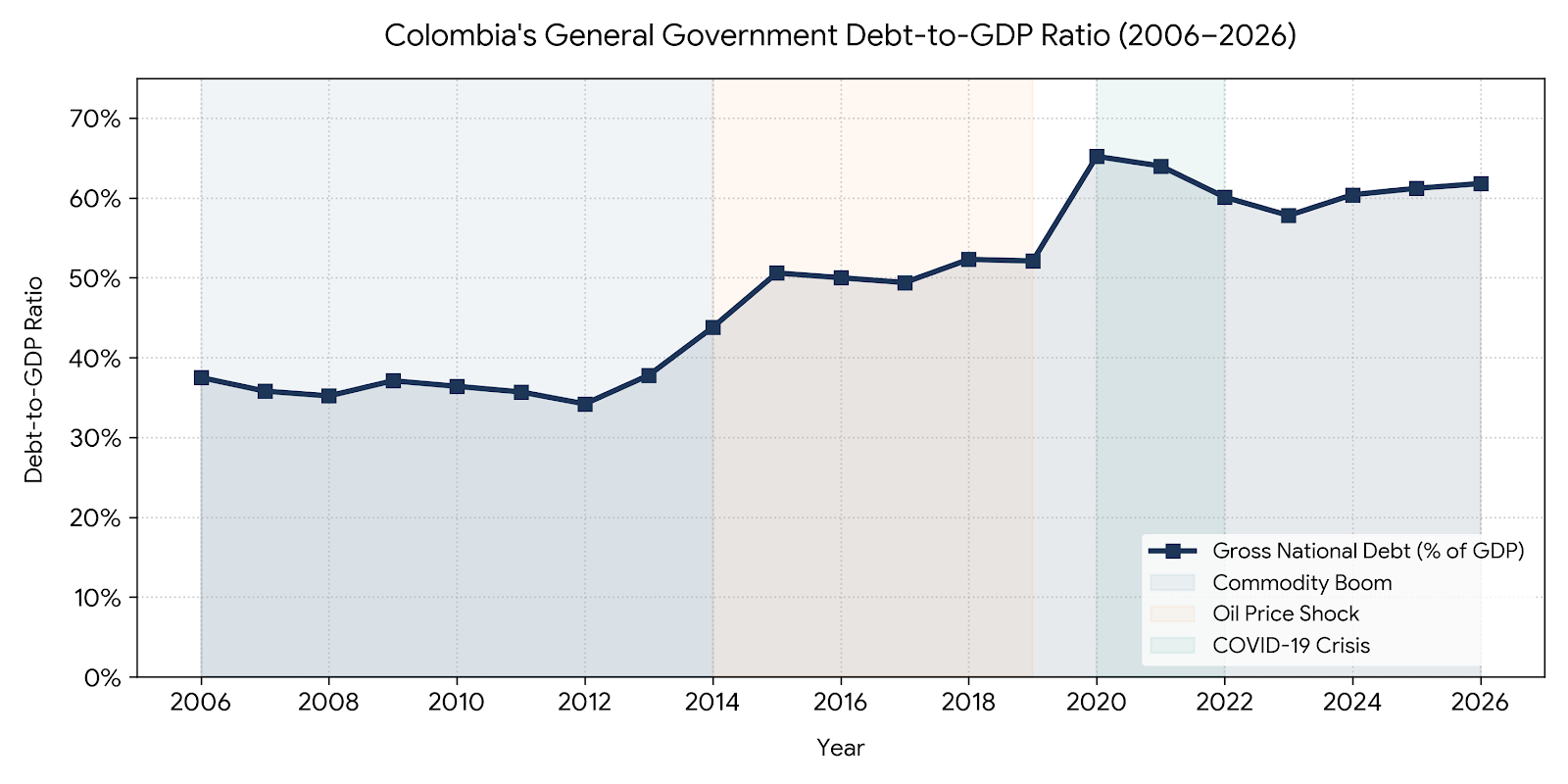

Two decades of fiscal data show that Colombia’s gross general government debt has moved through four distinct macroeconomic phases, ending the current cycle at a level that is materially higher than its pre-pandemic baseline. Persistent annual fiscal deficits, currency volatility, an emergency spending shock and weaker-than-projected tax revenues have combined to push the ratio of public debt to gross domestic product from the mid-30s percent range in the mid-2000s to a band of roughly 60 to 62 percent at the start of 2026, according to figures published by the Ministerio de Hacienda y Crédito Público and the Banco de la República.

The shift carries direct implications for sovereign bondholders, multinationals operating in Colombia and any investor pricing country risk in the Andean region. All three major rating agencies — S&P Global Ratings, Moody’s Ratings and Fitch Ratings — now place Colombia in speculative-grade, or junk, territory, with consecutive downgrades through 2025 and into early 2026.

“The activation of the escape clause confirms that the deterioration observed in 2024 will not be corrected in 2025.” — Renzo Merino, sovereign analyst, Moody’s Ratings

The commodity cushion: 2006 to 2014

During the global commodity supercycle, Colombia benefited from sustained gross domestic product growth and steady government revenue. Hydrocarbon and mining receipts — channeled through Ecopetrol (NYSE: EC; BVC: ECOPETROL) and the broader extractive sector — supplied a substantial share of national tax intake. The debt-to-GDP ratio remained relatively stable during this period, generally hovering between 34 and 38 percent. Even with chronic primary deficits, nominal growth in the denominator absorbed new borrowing, masking the underlying structural imbalance that the Comité Autónomo de la Regla Fiscal (CARF) would later flag as the persistent driver of fiscal stress.

The currency and revenue shock: 2014 to 2019

The mechanics of the ratio changed sharply when Brent crude prices collapsed in late 2014. Reduced hydrocarbon royalties widened the fiscal gap just as the Colombian peso depreciated against the US dollar. Because a significant share of Colombia’s sovereign liabilities is denominated in foreign currency, the peso’s slide automatically inflated the local-currency value of outstanding external debt when measured against domestic GDP. The combined effect — wider deficits funded by new borrowing, plus a valuation effect on existing dollar-denominated obligations — pushed the ratio steadily higher through the late 2010s.

The structural revenue weakness that surfaced during this period has remained a recurring theme in subsequent fiscal assessments from Fedesarrollo and the Pontificia Universidad Javeriana Observatorio Fiscal, both of which have noted that successive tax reforms failed to fully close the gap between commitments and ordinary income.

The pandemic ceiling: 2020

The combination of emergency social spending under the Ingreso Solidario program, expanded health outlays and a sharp contraction in nominal GDP drove the ratio to a historic peak above 65 percent in 2020. The Ministerio de Hacienda reports the all-time high at 65.3 percent of GDP that year. The government activated the escape clause of the regla fiscal — Colombia’s fiscal rule, codified in Law 1473 of 2011 and modified by Law 2155 of 2021 — to accommodate the spending response, suspending the rule for 2020 and 2021.

That episode also triggered the first sovereign downgrade cycle: S&P Global Ratings cut Colombia’s long-term foreign currency rating to BB+ from BBB- in May 2021 after the administration of then-president Iván Duque withdrew a tax reform bill following street protests, costing the country its investment-grade status with that agency.

The new baseline: 2023 to 2026

Strong post-pandemic nominal growth briefly pulled the debt ratio down toward 57 percent in 2023. The decline did not hold. Structural spending pressures, elevated international interest rates and tax collections below budgeted projections pushed the ratio back up, establishing a new operating band around 60 to 62 percent of GDP. The Ministerio de Hacienda reported government debt to GDP at 61.3 percent for 2024.

The administration of President Gustavo Petro and Finance Minister Germán Ávila Plazas activated the regla fiscal escape clause for a second time in June 2025, with the Consejo Superior de Política Fiscal (Confis) approving a three-year suspension covering 2025 through 2027. The decision came despite an unfavorable technical opinion from the Comité Autónomo de la Regla Fiscal, which concluded that legal conditions for activating the clause were not met outside of a national emergency. The clause had previously been invoked only during the COVID-19 pandemic.

According to the Marco Fiscal de Mediano Plazo (MFMP) presented by the Ministerio de Hacienda, net public debt to GDP is projected to rise from 53 percent in 2023 to 61.3 percent in 2025 and approximately 63 percent in 2026. The fiscal deficit for 2025 was initially projected at 7.1 percent of GDP and later revised to roughly 6.2 percent of GDP, with the administration targeting a deficit below 6 percent of GDP for 2026.

Debt service consumes a larger share of the budget

The cost of servicing this debt has reshaped the structure of the national budget. The 2026 draft budget presented by Minister Ávila totals $557 trillion COP, equivalent to roughly $134.7 billion USD, and represents 28.9 percent of GDP. Of that, debt servicing costs are projected at $102.5 trillion COP, or 5.3 percent of GDP, down from 6.2 percent of GDP in 2025.

The figures published by the Ministerio de Hacienda for domestic debt service in 2026 are higher when measured against tax intake alone: of an estimated $130 trillion COP in domestic debt service, $79 trillion COP corresponds to principal that can be rolled over through new issuances, while $51 trillion COP represents interest payments funded directly from the budget. Against projected tax revenue of approximately $300 trillion COP, that implies roughly one in every three pesos collected by the central government is allocated to interest on existing debt.

Rating agencies reprice the sovereign

The rating cycle has accelerated alongside the fiscal trajectory. Moody’s Ratings downgraded Colombia to Baa3 and subsequently into junk territory in 2025, citing the suspension of the fiscal rule. S&P Global Ratings issued a further downgrade in April 2026, its second cut in less than a year, on the same persistent deficit and debt concerns. Fitch Ratings also moved Colombia deeper into speculative grade in December 2025.

The Banco de la República reported external debt — combining public and private liabilities — at $238.7 billion USD at the close of November 2025, equivalent to 54.8 percent of GDP, an increase of $15.8 billion USD from January of the same year. The Colombian economy is currently valued at approximately $435 billion USD.

What investors are watching next

The Comité Autónomo de la Regla Fiscal has stated in its most recent reports to Congress that the 2025 primary balance target was missed by a wide margin even after the escape clause was activated, and that incoming projections for 2026 raise the bar for any return to the original fiscal rule by 2028. Business groups including Fenalco and the Consejo Gremial Nacional have publicly opposed the suspension and signaled potential legal challenges.

The 2026 financing plan disclosed by the Ministerio de Hacienda includes approximately $4.6 billion USD in global bond issuances, primarily to refinance a one-year Swiss-franc Total Return Swap operation valued at roughly $9.3 billion USD. The ministry has stated that the issuance does not constitute net new external debt. Updated debt and deficit targets are scheduled for release in the next iteration of the Plan Financiero.

For executives operating in Colombia or evaluating new investment, the baseline shift from a mid-30s to a low-60s debt-to-GDP environment alters several variables simultaneously: peso volatility tied to refinancing cycles, the trajectory of corporate tax policy as Congress weighs successive reform proposals, and the path of domestic interest rates set by the Banco de la República as it manages inflation alongside elevated sovereign funding costs. Detailed historical and forward-looking debt data is published by the Investor Relations Colombia office of the Ministerio de Hacienda.

Colombia’s General Government Debt-to-GDP Ratio (2006-2026) (image: Google)