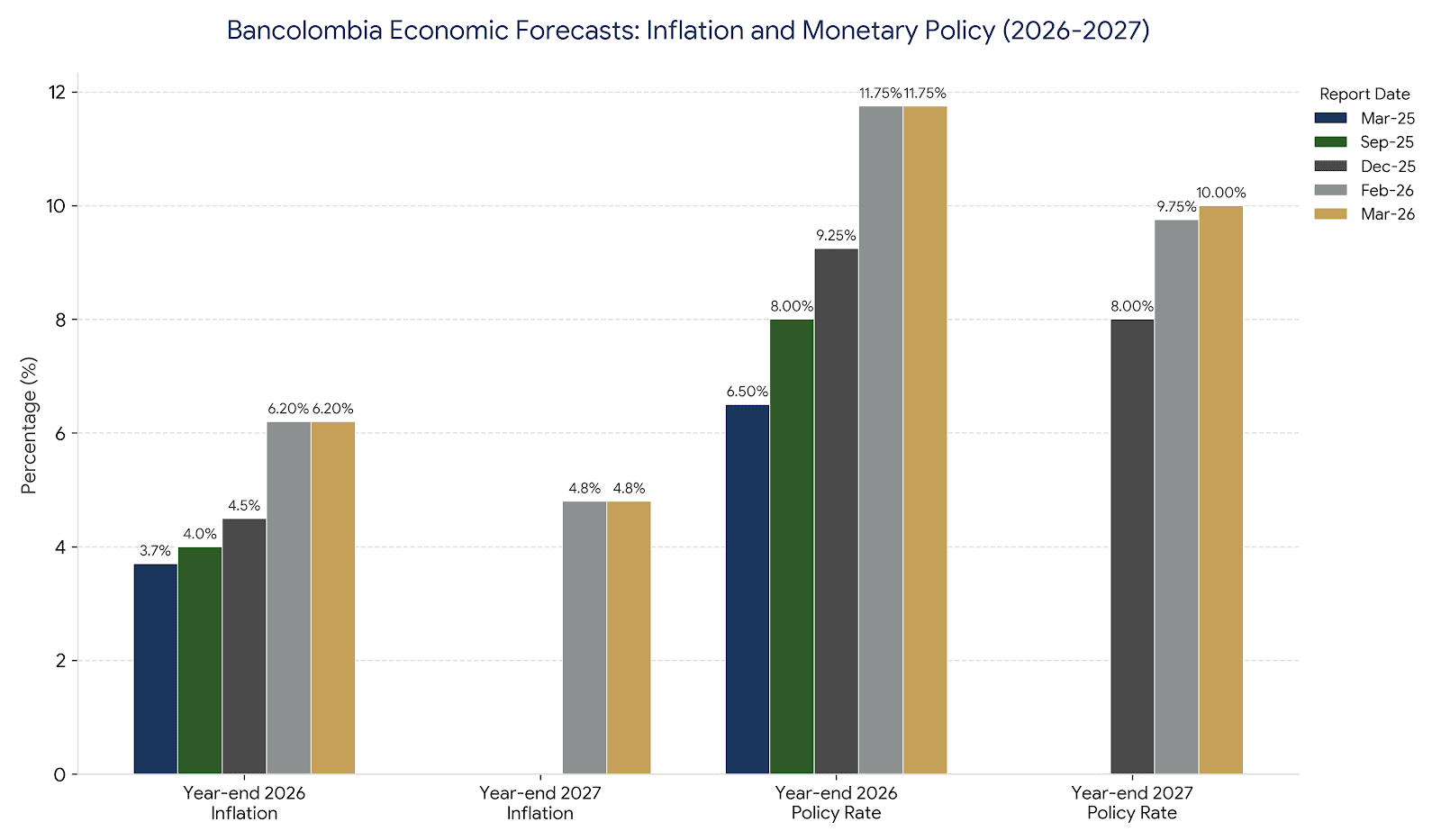

Colombia’s Central Bank Prepares to Raise Policy Rate to an Expected 12.00%

Central bank hike aims to stabilize inflation amid global volatility.

The upcoming monetary policy meeting of the Banco de la República, scheduled for April 30, takes place as the balance of financial risks has shifted significantly compared to the first quarter of 2026. Analysts from Bancolombia (NYSE: CIB) expect the Junta Directiva to increase the benchmark interest rate by 75 basis points, bringing the policy rate to 12.00%.

The convergence of elevated inflation, recent reversal episodes, and misaligned market expectations has reinforced the perceived need for a restrictive monetary stance. This strategy aims to contain domestic demand while preserving the institutional credibility of the central bank. Unlike previous sessions, the current decision-making process is influenced by a shifting global environment where markets have moved toward a higher-for-longer interest rate scenario amid increased uncertainty.

Recent discussions regarding the participation of the Ministro de Hacienda in the Junta Directiva sessions have introduced an additional element of analysis. However, current assessments suggest this does not alter the fundamental policy diagnosis, and no disruptions to the decision-making process are anticipated. Monetary policy is expected to maintain consistency, with the strategic focus shifting from reaching a contractive level to determining the necessary duration of that posture.

Analysts project Banco de la República will raise rates to 12.00% to combat inflation despite slowing domestic economic growth.

The international economic context provides a mixed backdrop for the Colombian decision. Private sector activity in the US appeared to accelerate in April, following a 1.7% monthly increase in retail sales during March. In contrast, the Eurozone reported a contraction in economic activity during April. Energy markets have also seen volatility, with US crude inventories rising in the second week of April while gasoline stocks saw a significant decline. Furthermore, crude prices surged following reports of new security incidents in the Strait of Hormuz.

Domestically, the Departamento Administrativo Nacional de Estadística reported that the Índice de Seguimiento a la Economía grew by 1.6% in February. While imports maintained growth during the same month, the urban unemployment rate across the 13 primary metropolitan areas continued a downward trend through March 2026. In the fixed income market, the central government reported debt levels at 64.2% of GDP for the first quarter, with internal debt accounting for 71.2% of that total.

Market movements reflected these broader trends as the US Treasury curve saw valuation increases driven by investor caution. In the region, Colombia, Brazil, and Uruguay emerged as the primary beneficiaries of the J.P. Morgan (NYSE: JPM) GBI index rebalancing in March. Locally, fixed-rate Títulos de Tesorería experienced devaluations across the entire curve last week. According to the April Encuesta de Opinión Financiera, these devaluations are expected to persist in the coming months. In currency markets, the COP appreciated last week against a backdrop of global and local factors, while the Euro lost ground against the USD.

Headline photo: Bogotá headquarters of Banco de la República (Banrepublica). Photo credit Juan Enrique Rodríguez, courtesy Banrepublica