Apple today

announced financial results for the second fiscal quarter of 2026, which corresponds to the first calendar quarter of the year.

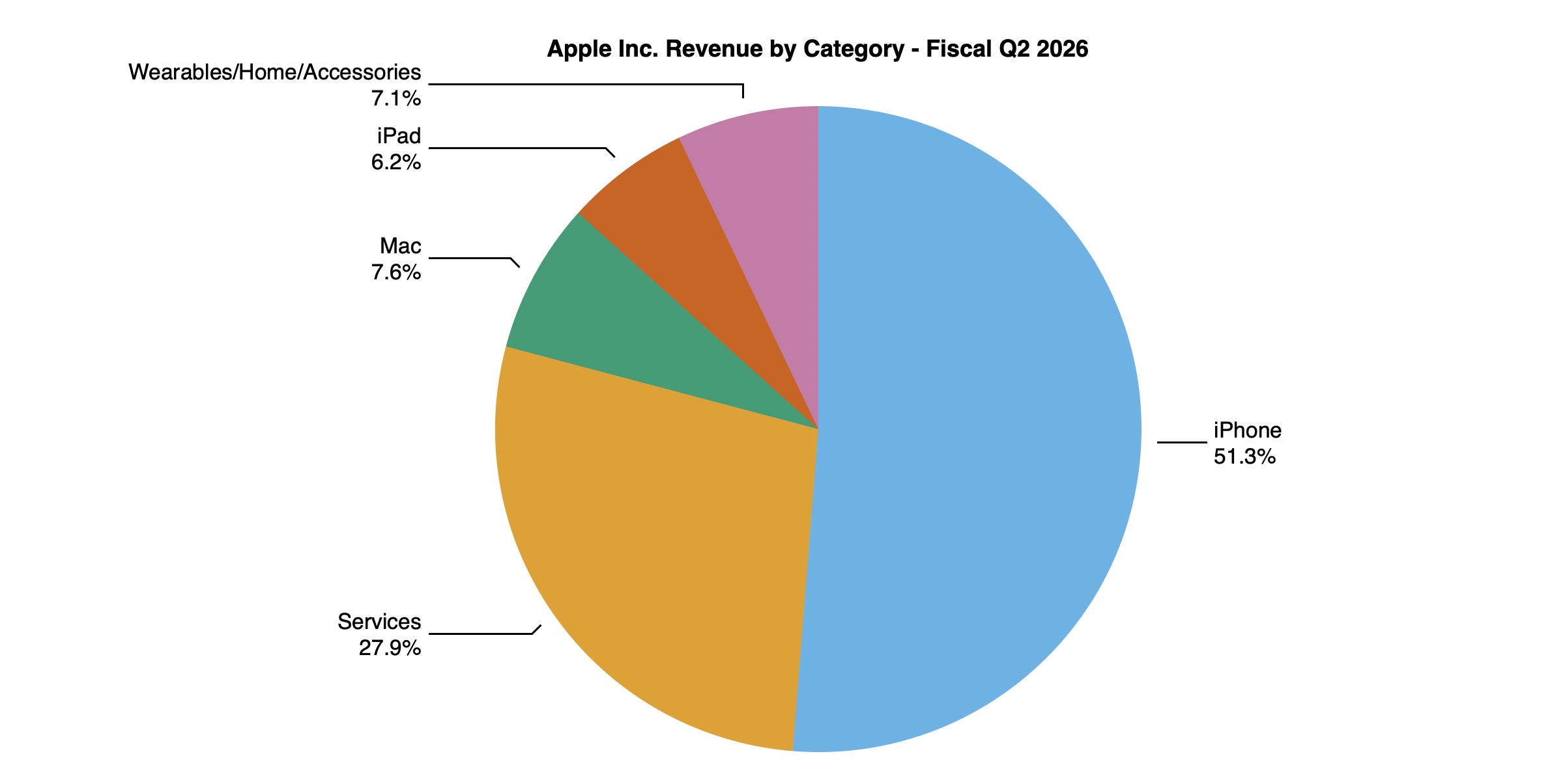

For the quarter, Apple posted revenue of $111.2 billion and net quarterly profit of $29.6 billion, or $2.01 per diluted share, compared to revenue of $95.4 billion and net quarterly profit of $24.8 billion, or $1.65 per diluted share, in the

year-ago quarter. Services revenue again reached an all-time high during the quarter, while company revenue, earnings per share, and iPhone revenue all set March quarter records.

Gross margin for the quarter was 49.3 percent, compared to 47.1 percent in the year-ago quarter. Apple's board of directors also authorized an additional $100 billion for share repurchases and declared an increased dividend payment of $0.27 per share, up from $0.26 per share. The dividend is payable May 14 to shareholders of record as of May 11.

"Today Apple is proud to report our best March quarter ever, with revenue of $111.2 billion and double-digit growth across every geographic segment," said Tim Cook, Apple's CEO. "iPhone achieved a March quarter revenue record, fueled by such extraordinary demand for the iPhone 17 lineup. During the quarter, Services achieved yet another all-time record, and we were excited to introduce remarkable new products to our strongest lineup ever. That included the addition of the iPhone 17e and the M4-powered iPad Air, along with the launch of MacBook Neo, which is captivating customers all around the world."

Apple will

provide live streaming of its fiscal Q2 2026 financial results conference call at 2:00 pm Pacific, and

MacRumors will update this story with coverage of the conference call highlights.

Conference call recap ahead...

1:39 pm: Apple's share price is currently down approximately 0.5% in after-hours trading following the earnings release, after rising by around 0.5% in regular trading today.

1:39 pm: "Our strong business performance during the March quarter generated over $28 billion in operating cash flow and drove new March quarter records for both operating cash flow and EPS," said Kevan Parekh, Apple's CFO. "Continued strong customer demand for our products and services once again helped us achieve a new all-time high for our installed base of active devices across all major product categories and geographic segments."

1:42 pm: All five of Apple's revenue categories saw year-over-year increases in the quarter: iPhone up 21.7%, Services up 16.3%,

iPad up 8.0%, Mac up 5.7%, and Wearables, Home and Accessories up 5.0%.

1:44 pm: All five of Apple's geographic segments also saw year-over-year increases: Americas up 11.9%, Europe up 14.7%, Greater China up 28.1%, Japan up 15.1%, and Rest of Asia Pacific up 25.3%.

1:58 pm: In a few minutes, Apple's quarterly earnings call and Q&A with analysts will begin. Typically, Apple CEO

Tim Cook and CFO Kevan Parekh host, but we could get an appearance from incoming CEO John Ternus. He takes over for Cook in September.

2:01 pm: The call is beginning with standard boilerplate about forward-looking statements from Investor Relations head Suhasini Chandramouli.

2:01 pm: On the call is Apple CEO Tim Cook. John Ternus will join for a "brief set of remarks" followed by CFO Kevan Parekh.

2:03 pm: "Good afternoon everyone, and thanks for joining the call. Before we get into the quarter, I wanted to take a moment to talk about the transition we recently announced."

2:03 pm: This is Tim's 89th earnings call.

2:03 pm: Tim: "I'll always be proud of the impact Apple has had on our users' lives, and I can't begin to express how grateful I am for our amazing teams. It's because of them that there is no company like Apple, and I truly believe there never will be."

2:04 pm: Tim: "This moment for the transition is the right one for a number of reasons. First, our business has been performing extremely well. The first half of this year was very strong, growing double digits year over year. Second, our road map is incredible. And most importantly, we have the right leader ready to step into the role."

2:04 pm: Tim: "As I have said, There is no one on this planet I trust more to lead Apple into the future than John Ternus. John is a brilliant engineer, a deep thinker, a person of remarkable character and a born leader. I know he will push us to go further than we think is possible in order to deliver the greatest products and services for our users I have been so proud to call him a colleague and a friend and I will be even more proud to call him Apple CEO."

2:05 pm: Tim: "Over the coming months, John and I will be working closely together to make sure this transition is perfectly smooth. I very much look forward to stepping into the role of executive chairman on September 1... I will be here to support him in any way he needs and in any way I can. I am incredibly optimistic about Apple's future, and I know we have the right team in place to deliver on the promise of this company."

2:05 pm: Tim: "I also want to take just a moment to share my profound gratitude for our shareholders, especially our long term shareholders, for believing in Apple and for your support over the years. It means a great deal to all of us."

2:06 pm: John Ternus, making his first remarks: "In my view, Tim is one of the greatest business leaders of all time. Stepping into the role of CEO is an incredible honor, and it means a great deal to me to have Tim's trust and confidence. I want to echo Tim's sentiment about our shareholders, especially those who have been with us for many years. Thank you so much for your confidence in our company."

2:06 pm: Ternus: "As you know, one of the hallmarks of Tim's tenure has been a deep thoughtfulness, deliberateness and discipline when it comes to the financial decision making of the company. And I want you to know that is something Kevan and I intend to continue when I transition into the role in September. This is an especially exciting moment for Apple. As Tim mentioned, we have an incredible roadmap ahead. And while you're not going to get me to talk about the details of that roadmap, suffice it to say this is the most exciting time in my 25 year career at Apple to be building products and services. There are so many opportunities before us, and I couldn't be more optimistic about what's to come for now, let me simply say I am deeply grateful to Tim, to the executive team and to everyone at Apple, and I look forward to all of the important work ahead."

2:07 pm: Tim is back: Apple revenue grew 17% from a year ago, to a March quarter record and above the high end of the guidance range. Grew despite supply constraints, with a March quarter record on iPhone, an all-time record on Services, and a March quarter record earnings per share of $2.01, up 22% year over year.

2:08 pm: Tim: "We recently marked Apple's 50th anniversary with celebrations in our retail stores and with users around the world. It was a special moment for us to reflect on the incredible journey we've shared with our users, to thank everyone who's been a part of it, and to look forward to writing the next chapter in our story of innovation. We have always believed that people who think different can change the world and we have been proud to build tools and technologies that allow them to do just that."

2:09 pm: Starting with iPhone, generating $57 billion in revenue, despite supply constraints. Launched the

iPhone 17e during the quarter. "The most powerful, capable and versatile iPhone family we've ever created."

2:11 pm: Tim is talking about Apple's current iPhone lineup, noting that the

iPhone 17 family is the most popular lineup in its history, and mentioned that the Artemis II astronauts took photos and videos with the

iPhone 17 Pro Max during their trip around the moon.

2:12 pm: Moving to the Mac, revenue was $8.4 billion, up 6% from a year ago. Set March quarter records for upgraders and customers new to the Mac. "Tremendous enthusiasm for

MacBook Neo."

2:13 pm: Turning to iPad, revenue was $6.9 billion, up 8% year over year.

2:13 pm: "Today, our iPad lineup is stronger than ever, led my the M4-powered

iPad Air. It raises the bar for what users can do on iPad."

2:14 pm: Wearables, Home and Accessories revenue came in at $7.9 billion, up 5% from a year ago.

2:15 pm: He's touting the various Apple Watch and AirPods in the lineup.

2:16 pm: Tim: "What truly sets Apple apart is how Apple intelligence is woven into the core of our platforms powered by Apple silicon and designed from the ground up to deliver intelligence that is fast, personal and private, this is not AI as a standalone feature but AI as an essential, intuitive part of the experience across our devices."

2:17 pm: "It builds on years of innovation from the neural engine to advanced on device processing, enabling capabilities that are not only incredibly powerful, but also respectful of user privacy. Increasingly, that same foundation is drawing developers and researchers to our products as powerful platforms for building and running agentic AI thanks to the unique combination of performance, efficiency, and on device capabilities."

2:17 pm: Moving to Services, generated $31 billion in sales, with double-digit growth across developed and emerging markets, with all-time revenue records across most Services categories.

2:18 pm: Apple Retail set a March quarter revenue record, with very high levels of store traffic throughout the quarter.

2:19 pm: Tim: "At Apple, we believe powerful innovation and uncompromising quality can go hand in hand with sustainability. Over the last year, we've reached new milestones in the environment, including the use of recycled content in 30% of the materials and all of our products, shipped in 2025, the most we've ever had. That includes the use of 100% recycled cobalt in all Apple design batteries and 100% recycled rare earth elements in all magnets. We've also achieved our goal of removing plastic from packaging with every Apple product now shipping in fiber based packaging."

2:20 pm: Tim: "We're also making great progress in advancing American Supply Chain Innovation as part of our $600 billion commitment to the US. We were pleased to share recently that

Mac mini production is coming to America later this year, expanding our factory operations in Houston with a brand new facility. In March, we were thrilled to welcome four new companies to our American manufacturing program to help manufacture essential materials and components for Apple products sold worldwide."

2:20 pm: Tim: "These include sensors that support key iPhone features like camera stabilization and integrated circuits, essential for features like crash detection and activity tracking. These efforts build on the progress we've made in the American manufacturing program, including the work we're doing to advance an end to end silicon supply chain across the US."

2:21 pm: Tim: "These efforts build on the progress we've made in the American manufacturing program, including the work we're doing to advance an end to end silicon supply chain across the US. At TSMC's Arizona facility, for example, Apple is on track to purchase well over 100 million advanced chips."

2:22 pm: Tim: "Whether around the world or in our own backyard, we're proud of the difference Apple has made to enrich lives and support the communities we serve. Looking ahead, we're delighted to welcome developers back to

Apple Park for WWDC 26. We can't wait to share what we've been working on, from AI advancements to exciting new software and developer tools, it's going to be an incredible week."

2:22 pm: Tim: "As always, we remain in relentless pursuit of even more powerful innovations, guided by our North Star, our users, as we celebrated 50 Years of Apple, we are even more excited and more optimistic about the next 50 years and beyond."

2:23 pm: Kevan: Saw strong performance with revenue records in every geographic segment. FX was 2.5 percentage point tailwind to the March quarter growth rate. We believe if you remove the favorable benefit from foreign exchange and add back the unfavorable impact from supply constraints, we would have had a higher growth rate for total company revenue.

2:23 pm: Products revenue was $80.2 billion, up 17% year over year. Company gross margin was 49.3%, up 110 bp sequentially. Products gross margin was 38.7%, down 200bp. Services GM was 76.7% up 20bp sequentially.

2:24 pm: Net income was $29.6 billion, and diluted earnings per share of $2.01, with $28.7 billion in operating cash flow.

2:24 pm: iPhone revenue was $57 billion, up 22% year over year, driven by the iPhone 17 family. iPhone grew double-digits in the majority of markets tracked.

2:24 pm: iPhone active install base grew to an all-time high, and set a March quarter record for iPhone upgraders. iPhone was the top-selling model in the US, urban China, the UK, Australia and Japan.

2:25 pm: Customer sat for iPhone 17 family was recently measured at 99% by 451 Research.

2:25 pm: Mac revenue was $8.4 billion, driven by the strength of recent product launches and up 6% year over year. In the US, customer sat was 97%.

2:26 pm: iPad revenue was $6.9 billion, up 8% year over year. All-time high for the install base, with more than half of iPad customers new to the product. Emerging markets revenue grew by double digits including in India, Mexico and Thailand. Customer sat of iPad was 98% in the US.

2:27 pm: Wearables, Home and Accessories was $7.9 billion, up 5% year over year, driven by Wearables and Accessories. More than half of Apple Watch buyers were new to the product. Customer sat of Apple Watch was 96%.

2:27 pm: Services revenue hit $31 billion, up 16% year over year, with all-time records in both developed and emerging markets, and all-time revenue records in most Services categories. More than 2.5 billion active devices, and transacting and paid accounts reached all-time highs in the quarter.

2:28 pm: Apple is touting its improvements in business and enterprise, especially for AI development.

2:29 pm: Kansas City Public Schools are switching their high school students from Windows laptops and Chromebooks to MacBook Neo, moving to an all-Apple district.

2:31 pm: Apple has $147 billion in cash, reflecting $5.8 billion in debt maturities, commerical paper at $2 billion, and Apple has $85 billion in total debt, with net cash of $62 billion. Returned $15 billion to shareholders, with $3.8 billion in dividends and $11 billion in open market repurchases of 42 million Apple shares.

Moving ahead, we will no longer provide "net cash neutral" as a formal target. Apple has reduced net cash by over $100 billion since 2018.

2:33 pm: Color on forward-looking statements, assumes that global tariffs and policies stay in effect. Revenue to grow 14-17% year over year, with constrained supply and an A16-powered iPad compare from last year. Services revenue to grow similarly to the March quarter year over year, with FX tailwinds removed. Gross margin between 47.5% and 48.5%. OpEx between $18.8b and $19.1b. OINE around $250 million, tax rate around 17%.

2:33 pm: Tim and Kevan are taking questions, not John Ternus.

2:35 pm: Q: How much did demand outpace supply for iPhone and Mac in the quarter, and did June reflect supply constraints for those segments?

A: The constraints were primarily driven by the availability of the advanced nodes our SOCs are produced on. The constraints will be primarily on several Mac models given the high levels of demand we're seeing and we have less flexibility in the supply chain than we would normally have.

On Mac mini and

Mac Studio, both are amazing platforms for AI and agentic tools, and the customer recognition of that is happening faster than what we predicted so we have higher than expected demand. Customer response to MacBook Neo has been off the charts, and March quarter record for customers new to the Mac partly due to the Neo. Looking forward, the Mac mini and Mac Studio may take several months to reach supply demand balance.

2:37 pm: Q: Re net cash neutral not being a formal target, are we thinking about different types of capital return policy, it doesn't seem so but can you give some more detail about investments, is that organic vs inorganic?

A: Our goal of net cash neutral has served us well and has been a valuable framework for us. We're evaluating cash and debt independently and to make optimal economic decisions around how we best utilize debt and cash to support the business. We believe we can do this while being very efficient and remaining disciplined. We remain committed to returning excess cash to shareholders. We look to invest in the business. We've returned over a trillion dollars to shareholders, $850 billion through share repurchases. Added a new $100 billion buyback authorization, so capital return is something very important to us.

2:39 pm: Q: There's been some commentary around an agentic smartphone, I don't even know what that means, but comment about AI on the edge and that agents could catalyze smartphones, but also shift the smartphone form factor. With the rise of agents, how would you like us to think about that? Are new products coming of a totally new form factor or anything high level about that trend or non-trend?

A: You know we don't get into our future roadmap so I don't want to give too much info there, but we're thrilled with how the iPhone is doing, growing 22% in the quarter, followed from an incredible Q1, having the strongest cycle that we've ever had in our history from the launch through the March quarter, we could not be happier with it.

2:41 pm: Q: To the question around constraints and whatnot, I'll try to do it nicely given my age, the big concern out there is how margins go after the June quarter given the components and trends and whatnot and all these constraints. Is there some kind of overarching philosophy that you want us to think about? Is 47-48 a range you think you can stay in or is there no visibility beyond June to answer this question? Any comfort there would be so helpful.

A: Let me talk about memory specifically which I think is the root of the question. I'll go back to December for a moment. In the December quarter, we had a minimal impact due to memory and you can see that in the gross margin results. We said it would be a bit more in the March quarter and we did see higher memory costs, partially offset by benefit from carry-in inventory. For June, and what's embedded in the guidance, we expect significantly higher memory costs. They are also partly offset by the benefit of carry-in inventory. Where we don't give color beyond June, beyond the June quarter, we believe memory costs will drive an increasing impact on our business. We will continue to evaluate this and we will look at a range of options.

2:43 pm: Q: Given success of MacBook Neo, can you talk about how it's driven penetration with new customer segments with education, value or emerging markets, and how do you think about opportunities in underpenetrated markets more broadly and how will the future product roadmap inform that?

A: We are supply constrained, we were very bullish on the product before announcing it, but we undercalled the level of enthusiasm that would be with it. It's very much focused on getting the Mac to even more people than we were reaching before. We're very focused on customers new to the Mac and customers that have been holding onto their Mac a very long period of time. We're doing well with both of those. As Kevan alluded to, we're seeing school systems that are switching from Chromebooks and Windows PCs to the MacBook Neo and hearing anecdotally of those kinds of stories happening at the school system level and at the consumer level. We could not be happier with how things are going at the moment.

2:45 pm: Q: Has new ad inventory on the

App Store been a noteworthy improvement to Services revenue on the store, and also adding ads to Maps this summer?

A: We did see year-over-year growth in ads, we did introduce additional ads to the App Store search results on platforms that users trust. This summer in the US and Canada,

Apple Maps will feature ads during key search and discovery moments. We believe it's possible to help business of all sizes to grow while preserving the user experience and letting people preserve their fundamental right to privacy.

2:46 pm: Q: You noted higher memory costs in the June quarter; you have a lot of supply chain efficiencies, relationships, relative to your competitors. Do you think that in times of such dislocation, Apple would be more focused on share gain or potentially you don't raise pricing and lower ends of the portfolio where competitors are struggling or more focused on profitability?

A: We will look at a range of options with memory costs increasing and I don't really want to go beyond that at this point.

2:47 pm: Q: How is Apple thinking about the broader monetization, what parts of the AI stack do you think Apple will be focused on internally versus leveraging your partners, early looks into where you're developing relationships? Where will Apple invest more heavily over the next several years, and does this relate to your net cash comments as we enter an AI-centric world?

A: We are investing more and you can see that in the OpEx numbers, and if you look at R&D you'll see that that is accelerating much higher than the company is, we're investing in products and services and see opportunities in both of those and could not be more excited in both of those. From the start we believe AI is a very important investment for Apple.

2:49 pm: Q: Going back to iPhone performance, you've had 20%+ growth despite supply constraints and that may continue into June. What are the levers driving this impressive growth despite constraints and what's the durability of the growth?

A: It's the iPhone 17 family driving it, that is as you point out, despite the supply constraints that we're experiencing, the things that are driving people to the 17 are people loving the design, the performance, the durability, they love the camera, Center Stage and that

Apple Intelligence is integrated across the platform. From where we're seeing the growth, we're seeing double-digit growth across the markets we track, and set a new March quarter record for upgraders as well. What's driving all this is that customer satisfaction for iPhone 17 family in the US is 99%, these numbers are unheard of. We're thrilled with how things are going.

2:51 pm: Q: What advice are you giving John to build on Apple's trends while shaping up the next chapter for hte company?

A: Steve's advice to me lifted a huge burden and that advice did well to me for 15 years. My advice is, one of the most important decisions he'll make is where to spend his time, and to spend it where the biggest benefit to the company and the users are. Remember the North Star to the company, making the best products in the world that really enrich other people's lives, and if you keep focusing on that and make your decisions around that, it will produce a great business and we'll be able to build more products and do it all over again.

2:53 pm: Q: Re supply constraints and your ability to acquire SOC and also memory?

A: The primary constraint in the March and June quarter is the availability of the advanced nodes our SOCs are produced on, not memory. I don't want to predict on our ability for supply and demand to match. If I look at Mac mini and Mac Studio, I think it will take several months to reach supply / demand balance. We're not at the point where we're saying this is going to end anytime soon. We just undercalled the demand. There are lead times to this, and it takes a while to correct that. The primary constraint from a product point of view, or the majority of it for this quarter, will be on the Mac. It's Mac mini, Mac Studio and MacBook Neo.

2:54 pm: Q: To the product mix within Services that are asymptotically difficult to scale that business from a profitability perspective, is there still low-hanging fruit in terms of value and leverage?

A: We have a wide range of businesses within the Services business, with different models and profitability, look at Q2, Services margin was up 20bp, but that was driven by mix. Some services improve in profitability as we scale, but we have a wide portfolio that grows in different rates at different times but we're encouraged by the overall trajectory that we've seen.

2:55 pm: Q: Your foundational models and the collaboration with Google, do you feel like you need to double down and invest more to balance those two priorities?

A: We're investing more, you can see that in the OpEx numbers, the collaboration with Google is going well, we're happy with where things are and happy with the work that we're doing independently as well.

2:58 pm: Q: For sequential moderation in gross margin is relatively muted compared to what we've seen over the last few year, was it mix?

A: Product margin dropped by 200bp, driven by seasonal loss of leverage and higher memory. Overall performance, sequential gross margin up 150bp was driven by FX, favorable mix, lower tariff costs, offset by seasonal loss of leverage and higher memory costs.

For March quarter, gross margin of 49.3% did include the impact of tariff-related costs, but tariffs in March vs December were lower because we had lower product volume sequentially from Q1 to Q2 and the full-quarter benefit in the reduction in the IEEFA tariff rates and the Section 122 tariffs. In filing a refund, we're following the processes and we plan to reinvest any amount we receive back into US innovation and advanced manufacturing. These would be new investments, and would be in addition to our prior commitments in the US.

3:00 pm: Q: What are you seeing specifically in China? From a competitive perspective, are you seing advantages from supply constraints impacting competitors?

A: First half of the year grew 33%, March quarter up 28%. The performance is driven by iPhone, which was also a March quarter record. If you look at the individual products, iPhone was the top-selling model in Urban China, Mac mini was the top desktop,

MacBook Air was the top laptop model. The traffic in our stores grew by double digits, we were celebrating Apple's 50th anniversary there and it's amazing to be a part of the community there. I'm really happy with how things have gone the first half of this year.

3:01 pm: Q: The same question for the India market, how are you seeing the market in India evolve around the base of iPhones and the opportunities of the rising middle class, the overall opportunity set in that market?

A: It's a huge opportunity for us, we've been focused on this for a while. It's the 2nd largest phone market and the 3rd largest PC market, we still have a modest share and I think that really speaks to the opportunity that we have. There are a lot of people moving into the middle class there and we've got some great products for them, both currently and coming. If you look at the majority of customers in all of our categories, from the iPhone to the Mac to the iPad to the Watch are new to that product there, it speaks very well to growing the install base there. Net net, I'm over the moon excited about India.

3:01 pm: That wraps the call, and leaves Tim Cook with one more earnings call before he moves from CEO to Executive Chairman.

This article, "

Apple Reports Record-Breaking 2Q 2026 Results: $29.6B Profit on $111.2B Revenue" first appeared on

MacRumors.comDiscuss this article in our forums