Colombia navigates fiscal challenges following S&P rating revision.

In Colombia’s local fixed-income market, the Títulos de Tesorería (TES) fixed-rate curve appreciated across its entire structure over the last month. As of March, the total balance of TES in circulation stood at 747.9 trillion COP. Despite this positive market valuation, macroeconomic headwinds remain a central concern for the Ministerio de Hacienda y Crédito Público. The fiscal balance of the Gobierno Nacional Central (GNC) reported an accumulated deficit of 1.7% of GDP through February.

These persistent fiscal imbalances were cited as the primary driver behind the recent decision by S&P Global (NYSE: SPGI) to downgrade Colombia’s sovereign credit rating. The administration continues to manage these debt instruments against a backdrop of tight monetary conditions, which remain a primary focus for institutional investors holding Colombian sovereign paper.

Colombian fixed-income markets show valuation gains despite a recent S&P credit downgrade linked to ongoing fiscal imbalances.

The international fixed-income landscape experienced notable shifts between March 25 and April 23, 2026. The yield curve for US Treasury bonds displayed mixed performance, defined by a decrease in short-term rates and an increase in long-term yields. Analysts attribute this volatility primarily to conflicting signals regarding the ongoing conflict in the Middle East.

Economic indicators released by the Bureau of Labor Statistics show that annual consumer inflation, measured by the Consumer Price Index (CPI), accelerated by 0.9 percentage points to reach 3.3% in March. This data triggered a rebound in short-term inflation expectations within the Treasury bond market, while medium and long-term outlooks remained stable. Consequently, the Intercontinental Exchange (NYSE: ICE) MOVE index—which tracks public debt market volatility—and the Cboe (NYSE: CBOE) VIX—which monitors S&P 500 equity volatility—both registered significant declines during the period.

Central bank hike aims to stabilize inflation amid global volatility.

The upcoming monetary policy meeting of the Banco de la República, scheduled for April 30, takes place as the balance of financial risks has shifted significantly compared to the first quarter of 2026. Analysts from Bancolombia (NYSE: CIB) expect the Junta Directiva to increase the benchmark interest rate by 75 basis points, bringing the policy rate to 12.00%.

The convergence of elevated inflation, recent reversal episodes, and misaligned market expectations has reinforced the perceived need for a restrictive monetary stance. This strategy aims to contain domestic demand while preserving the institutional credibility of the central bank. Unlike previous sessions, the current decision-making process is influenced by a shifting global environment where markets have moved toward a higher-for-longer interest rate scenario amid increased uncertainty.

Recent discussions regarding the participation of the Ministro de Hacienda in the Junta Directiva sessions have introduced an additional element of analysis. However, current assessments suggest this does not alter the fundamental policy diagnosis, and no disruptions to the decision-making process are anticipated. Monetary policy is expected to maintain consistency, with the strategic focus shifting from reaching a contractive level to determining the necessary duration of that posture.

Analysts project Banco de la República will raise rates to 12.00% to combat inflation despite slowing domestic economic growth.

The international economic context provides a mixed backdrop for the Colombian decision. Private sector activity in the US appeared to accelerate in April, following a 1.7% monthly increase in retail sales during March. In contrast, the Eurozone reported a contraction in economic activity during April. Energy markets have also seen volatility, with US crude inventories rising in the second week of April while gasoline stocks saw a significant decline. Furthermore, crude prices surged following reports of new security incidents in the Strait of Hormuz.

Domestically, the Departamento Administrativo Nacional de Estadística reported that the Índice de Seguimiento a la Economía grew by 1.6% in February. While imports maintained growth during the same month, the urban unemployment rate across the 13 primary metropolitan areas continued a downward trend through March 2026. In the fixed income market, the central government reported debt levels at 64.2% of GDP for the first quarter, with internal debt accounting for 71.2% of that total.

Market movements reflected these broader trends as the US Treasury curve saw valuation increases driven by investor caution. In the region, Colombia, Brazil, and Uruguay emerged as the primary beneficiaries of the J.P. Morgan (NYSE: JPM) GBI index rebalancing in March. Locally, fixed-rate Títulos de Tesorería experienced devaluations across the entire curve last week. According to the April Encuesta de Opinión Financiera, these devaluations are expected to persist in the coming months. In currency markets, the COP appreciated last week against a backdrop of global and local factors, while the Euro lost ground against the USD.

Headline photo: Bogotá headquarters of Banco de la República (Banrepublica). Photo credit Juan Enrique Rodríguez, courtesy Banrepublica

Sector adapts to investment decline through secondary asset markets.

The mining industry in Colombia is undergoing a structural transformation as companies prioritize operational efficiency to navigate a challenging economic environment. Recent industry data shows the mining Producto Interno Bruto (GDP) contracted by approximately 8%, while foreign direct investment has experienced a notable downturn. This trend has prompted firms to seek innovative financial strategies to maintain sustainability and competitiveness.

A primary strategy gaining traction is the rotation of underutilized industrial assets. By leveraging industrial auctions, companies are liquidating idle machinery—such as excavators, drilling rigs, and heavy-duty power equipment—to recover capital without the necessity of maintaining internal commercial structures. Superbid, a multinational industrial auction platform, has emerged as a key facilitator for these transactions within the region.

“Asset rotation is becoming a strategic decision to free up capital and improve operations.” — Maria Paula Villa Velez, Superbid

This operational shift toward asset-light business models will be a central topic at MINEXPO Colombia 2026, which is scheduled to take place on April 15 and 16 at Plaza Mayor Medellín. The event serves as a platform for mining producers, suppliers, and investors to discuss strategies for financial optimization and industrial reindustrialization.

The secondary market for industrial equipment has expanded significantly as mining companies divest assets no longer essential to their core operations. This machinery is being repurposed in the infrastructure, construction, and energy sectors, thereby extending the lifecycle of the assets and contributing to circular economy objectives. Market participants have observed increased competition for this equipment, with buyers consistently acquiring assets at market-determined values.

Looking toward the remainder of 2026, industry analysts expect the integration of these efficient asset management models to accelerate, particularly in regions such as Antioquia, where the nexus of mining and infrastructure projects remains a critical economic driver.

“Today the mining sector is understanding that efficiency is not only in producing, but in better managing its resources,” stated Maria Paula Villa Velez, sub-manager at Superbid Medellin. “Asset rotation is becoming a strategic decision to free up capital and improve operations.”

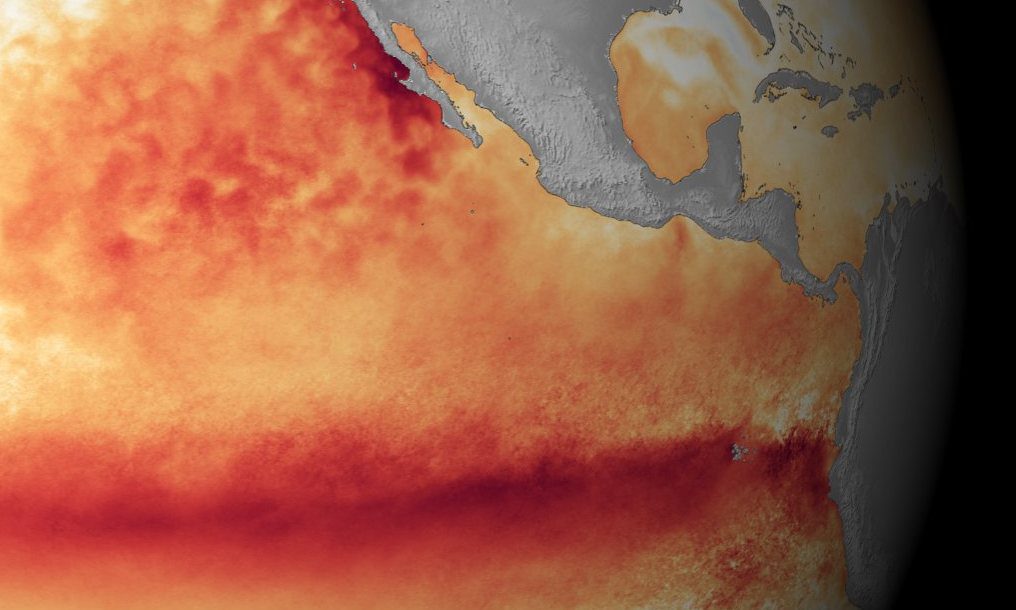

Escalating drought risk is potential bad news for rural communities, power consumers.

The National Oceanic and Atmospheric Administration (NOAA) and the Climate Prediction Center (CPC) have confirmed that ENSO-neutral conditions are currently present in the equatorial Pacific Ocean. However, technical indicators suggest a rapid transition, with a 61% probability of El Niño emerging between May and July 2026. For international investors and executives operating in Colombia, this shift indicates a looming period of increased operational costs, specifically within the energy and agricultural sectors.

The El Niño Southern Oscillation (ENSO) is a recurring climate pattern involving changes in the temperature of waters in the central and eastern tropical Pacific Ocean. During El Niño, trade winds weaken, allowing warm water to move toward the west coast of South America. Conversely, La Niña is characterized by stronger trade winds and cooler ocean temperatures. These fluctuations disrupt global atmospheric circulation, altering rainfall and temperature patterns across the planet.

In Colombia, the effects of these phenomena are distinct and significant. El Niño typically results in a sharp decrease in precipitation and a rise in average temperatures. Because Colombia relies on hydroelectricity for more than 60% of its total power generation, extended dry periods lead to lower reservoir levels. This forces the grid to rely on more expensive thermal generation fueled by natural gas and coal, which historically drives up spot market electricity prices for industrial and residential consumers.

“There is a 25% probability that the index reaches or exceeds +2.0°C during the Northern Hemisphere winter,” according to the National Oceanic and Atmospheric Administration.

The current technical diagnostic from NOAA shows that while the sea surface temperature index in the Niño-3.4 region was recently -0.2°C, the easternmost indices have already moved into positive territory. Furthermore, the equatorial subsurface temperature index has increased for five consecutive months. This accumulation of ocean heat is a primary driver behind the high probability of El Niño persistence through the end of 2026. Some models, including those from the European Centre for Medium-Range Weather Forecasts (ECMWF), suggest a 25% chance of a “strong” or “very strong” event, where temperatures exceed the 2.0°C anomaly threshold.

The Ministerio de Minas y Energíaand the Comisión de Regulación de Energía y Gas (CREG) are monitoring these developments closely. A strong El Niño would place additional stress on a natural gas system already facing structural supply constraints. Reduced hydroelectric output coupled with a potential deficit in gas supply could lead to significant energy price volatility. In past events, such as the 2015-2016 cycle, these conditions resulted in substantial financial pressure on the national utility system and necessitated emergency conservation measures.

Agricultural productivity is equally at risk. The Instituto de Hidrología, Meteorología y Estudios Ambientales (IDEAM)has identified the Caribbean and Andean regions—including departments such as La Guajira, Magdalena, and Antioquia—as highly vulnerable. During El Niño, these areas face increased risks of forest fires, water scarcity, and crop failure. For agribusinesses and exporters, this translates to disrupted planting cycles and higher production costs for staples like corn, potatoes, and vegetables, which can fuel domestic food inflation.

Conversely, when La Niña is in effect, Colombia faces the opposite extreme. The cooling of the Pacific leads to excessive rainfall, which can cause devastating landslides and flooding in mountainous terrain. While La Niña can replenish reservoirs, it often damages infrastructure and logistics networks, complicating the transport of goods to port. The current transition out of a La Niña phase provides a brief window of ENSO-neutral stability, which the CPC estimates has an 80% chance of lasting through June 2026.

For the international business community, the significance of these weather cycles extends to macro-economic stability. Persistent dry weather can impact GDP growth by raising the cost of basic services and reducing agricultural output. Strategic planning for 2026 and 2027 must account for these climatic variables. Meteorologists at Colorado State University note that El Niño also tends to reduce hurricane activity in the Atlantic, which may provide some relief for coastal logistics, but the primary threat remains the inland hydrological deficit.

As the Ministerio de Ambiente y Desarrollo Sostenible activates preventive mechanisms, companies are encouraged to review their energy procurement strategies and water management protocols. The next comprehensive diagnostic update from NOAA is scheduled for May 14, 2026, which will provide further clarity on the intensity of the projected warming trend. Understanding the mechanics of the ENSO cycle is no longer a matter of environmental interest but a necessity for risk mitigation in the Colombian market.

Satellite sea surface temperature departure in the Pacific Ocean for the month of October 2015, where darker orange-red colors are above normal temperatures and are indicative of El Niño. (Image credit: NOAA)

Economic activity in Colombia expanded at an estimated annual rate of 2.1% during the first quarter of 2026. According to the latest NowCast report issued by the Grupo Cibest, unit of Bancolombia (NYSE: CIB, BVC: BCOLOMBIA), this outcome reflects a loss of momentum compared to the rolling quarter ended in February. That previous period recorded a growth of 2.2%, which was revised downward by 10 basis points from an initial estimate of 2.3%.

The 2.1% growth rate for the quarter indicates a slowdown relative to both the market consensus average of 2.7% and the internal growth forecast of 3.3% held by the bank. On a month-over-month basis, the seasonally adjusted series of the NowCast index posted a 1.3% contraction in March 2026. When compared to March 2025, economic activity grew by 2% year over year, representing a 50-basis-point decline from the 2.5% reading recorded the previous month.

“Overall, these results suggest that the economy is beginning to lose steam, amid multiple sources of uncertainty.” — NowCast Bancolombia Report

Analysis at the sector level reveals a broadly weaker growth profile, with deceleration appearing across most productive areas. Slower momentum was identified in trade, manufacturing, recreation, real estate, and financial services. Manufacturing expansion cooled to 1.0% in March 2026, while financial services recorded marginal growth of 0.6%. The real estate sector maintained a steady growth rate of 1.9%.

Construction and communications were the only sectors to record negative growth during the period. The construction sector saw a significant downturn, contracting by 2.3% in March 2026 after having posted 1.4% growth in February. The information and communications sector contracted by 0.4%, marking its fourth consecutive month in contractionary territory. Conversely, acceleration was noted in public administration, which grew by 5.1%, agriculture at 3.7%, and mining at 0.8%.

The NowCast family of indicators is prepared by Grupo Cibest through the processing and aggregation of transaction data from the bank’s various payment channels. Using advanced quantitative tools, the index provides high-frequency estimates of Colombian productive activity to complement official data from the Departamento Administrativo Nacional de Estadística. The report was authored by Arturo Yesid González Peña, Head of Quantitative and Analytics, and Sebastián Ospina Cuartas, Data Controller.

The report also incorporates data from the Bloomberg platform and FocusEconomics Consensus Forecasts to provide broader economic context. While the national economy remains in expansionary territory, the analysts suggest that the current results indicate the market is losing steam due to various sources of domestic uncertainty.

Credit downgrade is an indictment of the Petro administration’s fiscal management, including suspension of the fiscal rule.

On April 8, 2026, S&P Global Ratings (NYSE: SPGI) lowered its long-term foreign currency sovereign credit rating on Colombia to BB- from BB and its long-term local currency rating to BB from BB+. The outlook for both ratings is stable, reflecting expectations that the Government of Colombia will gradually reduce its fiscal deficit while sustaining moderate growth in the national gross domestic product.

The rating action follows persistent fiscal imbalances and a policy environment that has become less predictable since the pandemic-related recession. The government decision to suspend the national fiscal rule in 2025 marked a significant shift in the policy framework. Pro-cyclical fiscal policies have provided marginal support for employment and consumption, but have also contributed to higher inflation expectations and a wider current account deficit. S&P expects the general government fiscal deficit to reach 5.6% of the national gross domestic product in 2026, compared to 5.3% in 2025.

“We expect Colombia to have consistently large fiscal deficits over the next few years.” — S&P Global Ratings

Institutional stability remains a key factor in the rating, though challenges persist. A fragmented legislature followed the March 2026 elections, where Pacto Histórico and Centro Democrático emerged with the largest minorities. The upcoming presidential election, scheduled for May 31, 2026, adds further uncertainty. Candidates such as Iván Cepeda of Pacto Histórico, Paloma Valencia, and Abelardo de la Espriella have proposed varying approaches to fiscal consolidation. The new administration will inherit spending pressures related to domestic security, rising healthcare costs, and pension payments linked to minimum wage increases.

The Banco de la República, the independent central bank of the country, has maintained a tight monetary policy to combat inflationary pressures. Annual inflation reached 5.3% in February 2026, prompting the bank to increase reference rates to 11.25%. S&P anticipates that inflation will not return to the target range of 3% +/- 1% until early 2029. While the independent status of the central bank provides a buffer against external shocks, high interest rates and lower-than-expected revenue collections have contributed to the widening deficit since 2024.

Economic growth is projected at 2.5% for 2026, slightly below the 2.6% recorded in 2025. Per capita growth is estimated at $9,900 USD for 2026, with real growth expected to average just above 2% through 2029. Despite being a net energy exporter, the performance of the US economy and international energy prices continue to influence national outcomes. Hydrocarbon exports declined to 35% of goods exports in 2025, down from 67% in 2013, showing some diversification even as the sector remains a primary source of volatility.

Net general government debt is forecast to approach 66% of the national gross domestic product by 2029, rising from 60.4% in 2025. S&P notes that the government interest burden will average 12.3% of general government revenue over the next three years. The shift toward issuing shorter-term debt instruments has reduced reported interest payments but increased vulnerability to interest rate fluctuations. External indicators remain a concern, with narrow net external debt expected to stabilize at 130% of current account receipts through 2029. Foreign direct investment is expected to be the primary source for funding the current account deficit, which is projected to stabilize around 2.6% of the national gross domestic product.

President Gustavo Petro has triggered a rare institutional confrontation with the Central Bank after he ordered to “break relations” following an modest interest rate increase, raising concerns over economic policy independence just two months before the May 31 presidential election.

The board of Banco de la República voted on March 31 to raise its benchmark rate by 100 basis points to 11.25 per cent, defying government pressure for looser policy. Finance minister Germán Ávila denounced the move as “disproportionate” and withdrew from the board, accusing policymakers of privileging financial sector interests over economic growth.

The decision marks an unprecedented rupture in Colombia’s macroeconomic governance framework. By stepping away from the board, Ávila has effectively deprived it of the quorum required to meet under existing statutes, raising the prospect of a policy deadlock just as inflation remains above target.

At stake is more than a disagreement over rates. The confrontation exposes deeper tensions between a government focused on growth and redistribution and a technocratic central bank committed to price stability. It also risks undermining one of Colombia’s most respected institutions at a time of heightened global uncertainty.

Governor Leonardo Villar defended the rate hike, insisting the bank’s constitutional mandate to control inflation could not be subordinated to political considerations. He said the board remained focused on steering inflation back to its 3 per cent target, noting that price pressures — currently running at 5.29 per cent annually — remain elevated despite signs of moderation.

“The decisions are based on technical criteria,” Villar said, rejecting accusations of bias towards the financial sector. He also warned that the government’s withdrawal runs counter to institutional norms.

Markets are now watching whether the government intends to sustain its boycott. Under Colombian law, the presence of a Finance Minister is required for board meetings, meaning continued absence could paralyse rate-setting decisions in the coming months. Three key meetings — in April, June and July — are scheduled before the end of Petro’s term, with the latter two falling after a decisive first-round of the presidential elections.

Business leaders have reacted with alarm. Camilo Sánchez, head of utilities association Andesco, described the breakdown in coordination as “dire”, warning that permanent dialogue between fiscal and monetary authorities is essential for economic stability.

Analysts say the government may be using institutional leverage to halt further rate increases, given that a majority of board members had signalled a tightening bias to anchor inflation expectations. A prolonged standoff could, however, carry significant costs.

Colombia has long been viewed by investors as a regional outlier for its strong central bank independence. Any perception that political pressure is eroding that autonomy could weigh on the peso, increase borrowing costs and deter foreign investment.

The dispute comes against a complex macroeconomic backdrop. Inflation has been fuelled in part by a sharp increase in the minimum wage and higher public spending, while external risks — including rising energy prices linked to the war in the Middle East and closure of the Strait of Hormuz by Iran.

For Petro, the rate hike reinforces a long-standing critique that tight monetary policy is stifling growth and employment. Writing on social media, the president accused the central bank of pursuing a “suicidal” policy that harms the wider economy.

Yet economists warn that weakening institutional credibility could ultimately prove more damaging than high interest rates. “The risk is not just policy error,” one Bogotá-based analyst said. “It is the erosion of the rules of the game.”

The coming weeks will test whether the standoff is a negotiating tactic or the start of a more fundamental shift in Colombia’s economic governance. Either way, the episode has already injected a new layer of uncertainty into one of Latin America’s most closely watched economies.

Stronger peso and oil prices shift Colombian investment landscape.

The Colombian peso (COP) experienced a 2.1% appreciation during March 2026, driven by a recovery in global oil prices and key domestic developments. According to the latest analysis from Bancolombia (BVC: BCOLOMBIA / NYSE: CIB), the performance of the currency coincided with the results of national legislative elections and recent monetary policy adjustments by the Banco de la República.

Global energy markets recorded a significant increase in crude prices throughout the month. Brent crude rose 63% to end March at $118 USD per barrel, while West Texas Intermediate (WTI) increased 51% to close at $101 USD per barrel. These price movements have been largely attributed to geopolitical tensions in the Middle East, which continue to influence international commodity flows and investor sentiment.

On the domestic front, the Gran Coalición por Colombia primary election recorded a turnout of more than 5 million voters. Market analysts indicated that the high participation rate was viewed as a positive indicator of institutional stability. Simultaneously, the Board of Directors of the Banco de la República increased the national policy interest rate by 100 basis points, bringing the benchmark rate to 11.25%. This decision aligns with regional efforts to manage inflationary pressures through tighter monetary control.

International market conditions also reflect a shift in expectations regarding the Federal Reserve. Due to ongoing conflict in the Middle East and persistent economic indicators, markets currently anticipate that the US central bank will maintain existing interest rates without cuts for the remainder of the year.

Looking forward to April, the research team at Bancolombia—led by Chief Economist Laura Clavijo, Macroeconomic Manager Jose Luis Mojica, and International and FX Analyst Maria Paula Gonzalez—projects that the exchange rate will trade within a range of $3,625 COP to $3,725 COP. This forecast accounts for continued volatility and heightened uncertainty in both global and domestic financial markets.

Finance Minister Germán Ávila walked out of a central bank board meeting, accusing it of going against Colombia’s national interests and deepening institutional tensions.

Colombia’s Finance Minister Germán Ávila abandoned a meeting of the board of the central bank (Banco de la República), on April 1 in protest over two decisions by the institution: the release of an internal document without prior consultation, and a 100-basis-point increase in the benchmark interest rate, which was raised to 11.25%.

According to the finance minister, the disclosure of the document, which involved both institutions and was linked to a draft government decree, constituted an “abuse.”

He also described the rate hike, the second so far this year, as “irresponsible and inconvenient,” arguing that it contradicts the government’s economic growth strategy.

The central bank said the decision was approved by a majority of its board: “four members voted in favor of the increase, two supported a 50-basis-point cut, and one proposed keeping the rate unchanged.”

The bank justified the move by noting that inflation stood at 5.4% in January and 5.3% in February, above the 5.1% recorded at the end of 2025. It also warned of external risks, including the impact of the conflict in Iran on the global economy, which could increase the cost of key imports such as gas and fertilizers and add to inflationary pressures later this year.

It remains unclear whether Ávila’s withdrawal from the board will be temporary or permanent, but the episode marks a new point of institutional tension that could influence the direction of monetary policy in Colombia in the coming months.

Clash between monetary policy and government strategy

Ávila criticized the decision, saying the central bank is overlooking the country’s economic progress. “The decision taken by the central bank is repetitive and continues to ignore the national government’s efforts to ensure fiscal stability and sustained economic growth,” he said.

He also argued that the increase is disproportionate compared with global trends. “There is not a single economy in the world proposing a 200-basis-point increase in the benchmark rate in the current global context,” he said, referring to the fact that the bank had already raised rates by 100 basis points in February, meaning a total increase of 200 basis points in just four months.

The government maintains that macroeconomic conditions remain stable, pointing to controlled inflation, a relatively stable Colombian peso (COP) against the dollar, declining unemployment and solid productive growth, and argues that tighter monetary policy is unnecessary.

Debate over central bank independence

The Finance Ministry said the minister’s decision to leave the meeting does not seek to challenge the independence of the central bank, but rather to highlight the need for its decisions to align with the country’s economic and social reality.

However, the move has raised legal and institutional concerns. Central bank chairman of the board, Leonardo Villar noted that the finance minister has a constitutional obligation to attend board meetings, as he “not only represents the government but also lead the meetings” said in a public interview broadcasted by media outlet like La República.

He warned that an indefinite absence could amount to a breach of legal duties and urged President Gustavo Petro to appoint an “ad hoc” delegate if the minister decides not to attend future meetings.

Experts say the minister’s absence could affect the board’s ability to make decisions. According to Andrés Pardo, former deputy finance minister and head of Latin America macro strategy at XP Investments, in an interview with Valora Analitik, “current regulations require at least five members, including the finance minister or a delegate, for the board to deliberate and decide”.

This could mean that, without his presence, the central bank may be legally unable to adopt monetary policy decisions.

Economic impact

The rate increase could have significant effects on the real economy. According to the Finance Ministry, a move of this magnitude could slow economic recovery, increase borrowing costs for households and businesses, and raise debt servicing costs.

Small and medium-sized companies, construction, retail and tourism are expected to be among the most affected sectors, along with households holding variable-rate loans.

Lower-income groups could face the greatest impact, as reduced purchasing power and tighter access to credit may deepen economic inequality.

Colombia’s unemployment rate dropped to 9.2% in February from 10.3% a year earlier, marking the lowest level for the month since 2001, according to official data.

In February 2026, Colombia’s unemployment rate stood at 9.2%, a decrease of 1.1 percentage points compared with the same month in 2025 and the lowest figure for a February since 2001, according to the government through the National Administrative Department of Statistics (DANE).

According to the report, “at the national level, the employed population increased by 624,000 people compared with the previous year.” The sectors that contributed most to job creation were professional, scientific and technical activities, with 250,000 new positions, and the public sector (administration, education and health), with 244,000. In contrast, agriculture lost 363,000 jobs and the transportation sector 86,000 compared with February 2025.

President Gustavo Petro highlighted the result on his X account, stating that “we return to a single-digit unemployment rate, 9.2%, the lowest since 2018. More reasons not to accept the mistake of the right parties in claiming that raising the minimum wage to a living wage would bring an employment catastrophe. That was not true: we have the lowest unemployment of this century for the month of February.” The president also defended the minimum wage increase, which reached 23.7%, the highest recorded in the country.

Volvemos a un dígito de tasa de desocupación, 9,2%, la más baja desde el 2018.

Más razones para no aceptar la equivocación de la derecha al afirmar que el subir el salario mínimo al nivel del salario vital traería una catástrofe del empleo.

When analyzing the December–February rolling quarter, the unemployment rate stands at its lowest level in the past ten years, according to DANE reports. The figure rose from an average of 10.7% in 2017–2018 to a peak of 15.7% in 2020–2021, a period marked by the impact of the COVID-19 pandemic, before declining steadily to 9.2% in February 2026.

For the same period in 2025, the rate stood at 10.4%, representing a reduction of more than one percentage point.

These figures are consistent with estimates by the International Labour Organization (ILO) in Colombia, which had projected a gradual decline in unemployment from around 16% in 2020 to an estimated 8.3% for the previous year.

Chart showing unemployment in Colombia from February 2016 to February 2021, including the presidents in office during that period. Image shared by Pacto Histórico Representative David Racero.

Gaps and challenges in the labor market

Despite the overall improvement, the DANE report also highlights challenges in terms of labor inclusion. In February 2026, the unemployment rate for men was 7.4%, while for women it reached 11.7%, representing a gender gap of 4.3 percentage points.

However, the government noted that this gap has been narrowing, as it stood at 5.2 percentage points in the previous month.

The data come from “The Great Integrated Household Survey” (La Gran Ecuesta Integrada de Hogares – GEIH), DANE’s statistical instrument that provides information on the labor market, income, monetary poverty and the sociodemographic characteristics of Colombia’s population.

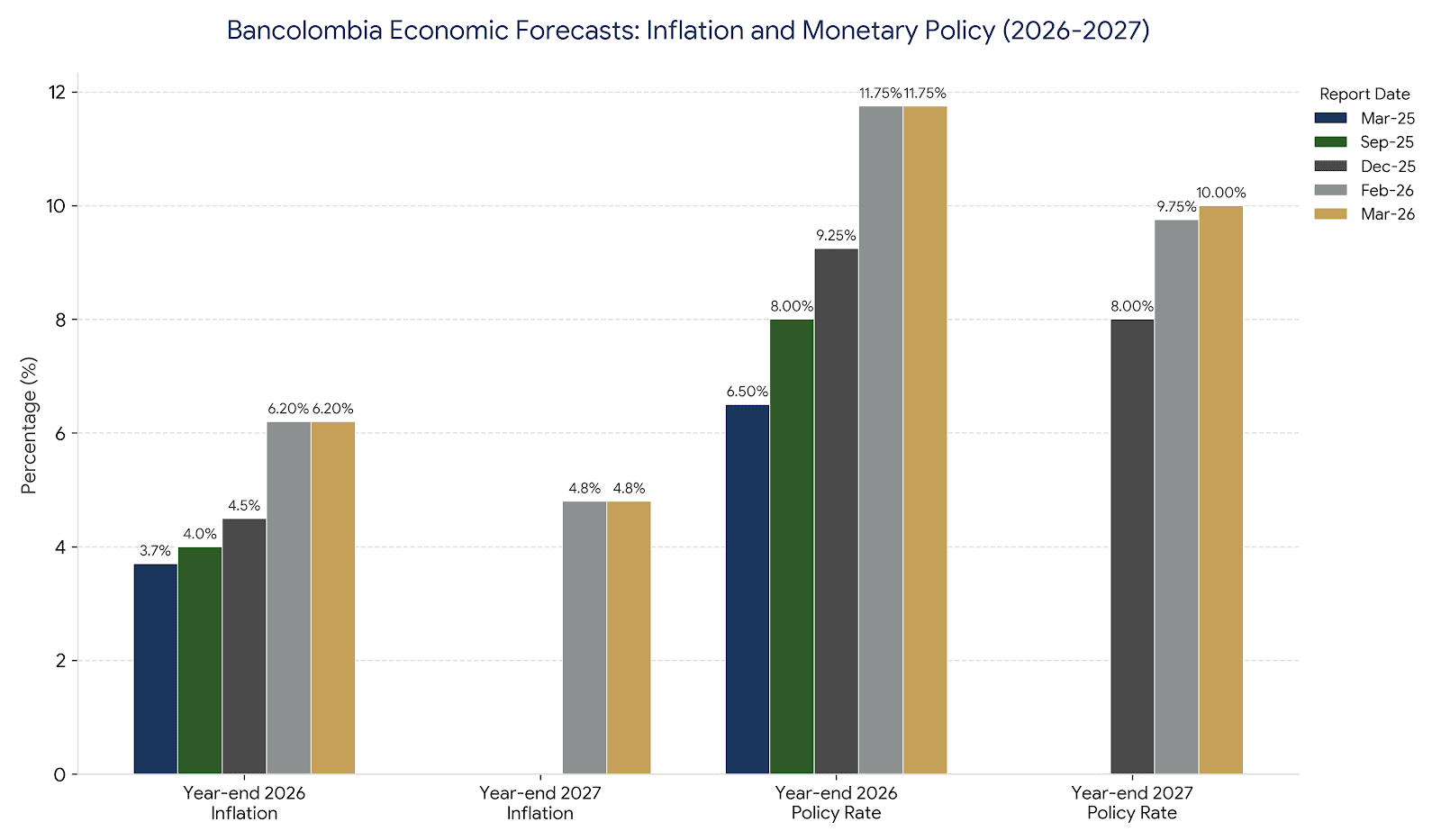

Bancolombia’s analysts expect the Junta Directiva of the Banco de la República to increase its policy interest rate by 100 basis points, bringing it to 11.25 percent. This forecast suggests that the first half of 2026 will be characterized by a more aggressive tightening cycle than previously anticipated, with the rate potentially reaching 12.75 percent.

The international landscape is playing an increasingly decisive role in these local policy configurations. A recent week of central bank decisions globally revealed a shift in tone among major financial institutions, primarily due to rising uncertainty stemming from the conflict in Iran. This geopolitical tension has directly impacted costs for energy, transportation, and agricultural inputs.

In the US, economic activity shows signs of moderation, yet producer price inflation in February exceeded expectations. The yield curve for US Treasuries, managed by the US Department of the Treasury, has shown mixed behavior as the conflict escalates, with the spread between 10-year and 3-month bonds reaching levels not seen since 2023. Inflation expectations in the US have rebounded in the short term, though they remain anchored over longer horizons.

Forecast Category

Mar-25

Sep-25

Dec-25

Feb-26

Mar-26

Year-end 2026 Inflation

3.7%

4.0%

4.5%

6.2%

6.2%

Year-end 2027 Inflation

—

—

—

4.8%

4.8%

Year-end 2026 Policy Rate

6.50%

8.00%

9.25%

11.75%

11.75%

Year-end 2027 Policy Rate

—

—

8.00%

9.75%

10.00%

Domestically, the business indices from think-tank Fedesarrollo showed mixed results for February. However, there are positive indicators in the labor market, as the urban unemployment rate across the 13 primary metropolitan areas continued its downward trend. Additionally, goods exports recorded an advance during the same period.

In the local fixed-income market, the TES fixed-rate curve saw a recovery last week. However, the March Financial Institutions Survey suggests that devaluations of TES may persist in the short term. Long-term TES Class B placements in the first quarter reached 1.0 percent of the GDP.

Chart based on data from Grupo Cibest & the Banco de la República.

Energy markets remain volatile as crude oil inventories in the US increased beyond expectations in the third week of March. Despite this, the price of Brent crude rose toward the end of the week, driven by skepticism regarding a potential ceasefire in the Middle East. The Colombian peso appreciated over the past week, tracking the intensity of the regional conflict.

The equity market results for the fourth quarter of 2025 remained neutral and aligned with market expectations. Global volatility continues to be shaped by energy shocks, geopolitical strife, and a cautious approach toward investments in artificial intelligence.

The projected rate hike by the Banco de la República is intended to send a definitive signal of commitment to price stability. This adjustment reflects not only recent inflation trends but also a strategic effort to prevent the further deterioration of expectations in a high-risk environment.

Headline image: Bogotá headquarters of Banco de la República (Banrepublica). Photo credit Juan Enrique Rodríguez, courtesy Banrepublica

Governance concerns and profit drops dominate shareholder assembly.

The Ecopetrol (NYSE: EC, BVC: ECOPETROL) General Shareholders’ Meeting concluded at the Corferias convention center in Bogotá, marked by a decline in annual profits and an intensifying debate regarding the continuity of the company’s president, Ricardo Roa. During the assembly, shareholders approved a dividend of $121 COP per share for minority holders and a total payment of $4 trillion COP to the Colombian government, which serves as the majority shareholder. The government’s payout is scheduled for distribution in two installments, to be completed by June 30, 2026.

Click on above image to view shareholder meeting

The financial results for the 2025 fiscal year revealed a significant contraction in net income, which fell to $9 trillion COP from the $14.9 trillion COP reported in 2024. Roa attributed this decline primarily to the volatility of international crude prices. He noted that the average price of Brent crude dropped from $80 USD per barrel to $68 USD per barrel over the period. According to company data, every $1 USD drop in the price of Brent corresponds to a reduction of approximately $500 billion COP in net profit and $700 billion COP in EBITDA. Despite the lower earnings, the company maintained a production level of 745,000 barrels per day and achieved a reserve replacement rate of 121%, the highest in five years.

Governance issues remained the primary focus of the assembly. Minority shareholders expressed concern over the legal challenges facing Roa, who is currently under investigation by the Fiscalía General de la Nación for alleged influence peddling. Additionally, the Consejo Nacional Electoral (CNE) has raised accusations regarding the alleged violation of spending caps during the presidential campaign of Gustavo Petro, which Roa managed. Angela Maria Robledo, Chair of the Board of Directors, defended the decision to retain Roa, stating that the board has activated a evaluation protocol while respecting the constitutional principle of the presumption of innocence.

Shareholders Erupt In Anger At CEO Ricardo Roa:

Abuchean a Ricardo Roa en asamblea de Ecopetrol

“¡Fuera, fuera!”: Este es el momento del tenso abucheo de los accionistas al presidente de la empresa

“Ecopetrol is listed on the New York Stock Exchange; we are governed by the strict regulations of US federal agencies. Agencies like OFAC and the SEC could intervene in the company and could even accelerate the payment of financial obligations, which would be extremely grave for Ecopetrol,” stated Martín Ravelo, President of the USO.

The Unión Sindical Obrera (USO), the primary labor union representing nearly one-third of the company’s workforce, has issued an ultimatum for Roa’s removal. Martin Ravelo, president of the USO, warned that the union will initiate a national strike and affect crude production if Roa is not aparted from his position by Monday, March 30. Ravelo expressed concern that Ecopetrol, which is subject to the regulations of the Securities and Exchange Commission (SEC) and the Office of Foreign Assets Control (OFAC), could face federal intervention. He highlighted that Ecopetrol’s current debt has reached $30 billion USD, exacerbated by rising interest rates, and warned that the company lacks the cash flow to respond to potential demands for early repayment of international obligations.

President Gustavo Petro responded to the union’s concerns via social media, stating that the executive branch will take measures to shield the company’s financial future. Petro emphasized the importance of maintaining investment during periods of high oil prices to prepare for future market downturns. He also criticized past administrations for failing to invest sufficiently in clean energy during previous price cycles. In contrast, Ravelo called for the board to maintain its independence from political influence, noting that four of the nine board members have already left formal records supporting Roa’s departure.

Ecopetrol also addressed the national gas supply, with Roa announcing that new regasification alternatives at Puerto Bahía and on the Pacific coast are expected to begin operations in the second half of 2026. These projects are intended to contribute between 186 and 430 Gbtud to the national grid. A third regasification facility in Coveñas is projected to start operations in 2029 with a capacity of 400 Gbtud. Despite these operational plans, the immediate focus of the international investment community remains fixed on the board’s upcoming meeting on Monday, where the leadership deadlock must be resolved to avoid a potential halt in national production.

Headline photo: Former Senator Jorge Robledo admonishes the Ecopetrol board of directors at the March 2026 shareholders’ meeting.

This mobile cinema initiative in Medellín provides training for 4,000 creators to boost local digital advertising and entrepreneurship.

MEDELLÍN — The mobile film festival SMARTFILMS announced the launch of its third edition in the “City of the Eternal Primavera” on March 17, 2026. The initiative aims to democratize cinema and foster local creative talent through technology and audiovisual narratives. The program’s goal is to train 4,000 participants in the technical skills required to produce films using mobile devices.

The launch is supported by the Alcaldía de Medellín (Medellín mayor’s office), which is providing 3,300 training slots, the Área Metropolitana del Valle de Aburrá (Aburrá Valley metropolitan area) with 300 slots, and the Cámara de Comercio de Medellín para Antioquia with 250 slots. Additional strategic partners include EPM and Fenalco Antioquia, organizations that focus on regional innovation and commercial development. The official opening, led by CEO Yesenia Valencia, took place at the Poblado branch of the Chamber of Commerce,

“SMARTFILMS is not just a festival; it is a platform that demonstrates that to tell a great story, one only needs a good idea and the device everyone carries in their pocket.”

The 2026 program utilizes a four-phase methodology designed to transition creators into digital entrepreneurs. The first phase involves mass training for 4,000 individuals in mobile audiovisual production. In the second phase, 400 selected participants will attend a specialized bootcamp at the Cámara de Comercio de Medellín para Antioquia featuring industry experts. The third phase focuses on business skills for 40 finalists, covering marketing, digital advertising, budgeting, and legal contracts.

In the final stage, participants must produce advertising content for three local neighborhood businesses to assist in their digital transition. Financial incentives include prizes of $10 million COP for first place, $5 million COP for second place, and $3 million COP for third place. Additionally, finalists receive seed capital of $1.5 million COP per person for recording equipment. Registration is managed through the cineconcelular.com platform.

The festival reports a significant regional economic impact, generating 115 direct jobs and over 300 indirect jobs. The direct positions include 33 payroll staff and 82 contractors based in Medellín. Since its inception, the model has trained 8,000 people and led to the creation of 120 businesses nationwide. These creative enterprises currently report monthly revenues ranging from $2 million COP to $10 million COP.

The 2026 version of the project seeks to expand its reach across all districts of the metropolitan area to stimulate the development of cultural companies and social transformation. Documentation from the organizers highlights a 0% desertion rate among participants over the last two years.

The move targets a high-value niche in the European bioeconomy, offering a scalable model for sustainable Amazonian exports.

The Colombian government has formally submitted a technical and scientific dossier to the European Union seeking authorization to market cacay flour as a “Novel Food.” This regulatory category governs the entry of non-traditional food products into the European market.

The submission is the first of its kind for an Amazonian product from Colombia. It follows a 2024 initiative involving the Ministry of Commerce, Industry, and Tourism and the [suspicious link removed]. The process was supported by the Sustainable Forest Territories (Territorios Forestales Sostenibles or TEFOS 3) project, a program funded by the British Embassy and the German Cooperation GIZ.

Diana Marcela Morales Rojas, the Minister of Commerce, Industry, and Tourism, stated that the application positions cacay as a strategic component of the national portfolio of high-value natural ingredients. The technical dossier was structured according to the guidelines of the European Food Safety Authority (EFSA). To meet these standards, Colombia provided evidence of safe historical consumption for at least 25 years, alongside data on nutritional profiles, safety, traceability, and sustainable production processes.

The administrative validation phase is expected to take one month, followed by a technical and scientific evaluation by EFSA that may last up to nine months. Six Colombian companies participated in the drafting of the expediente, providing technical data and validating industrial processes to demonstrate the feasibility of large-scale production under international standards.

“This step positions the cacay as a strategic ingredient within the Colombian portfolio of high-value-added natural products.” — Diana Marcela Morales Rojas, Minister of Commerce, Industry, and Tourism.

The cacay nut, native to the Amazon and Orinoquia regions, produces a seed containing up to 60% oil rich in omega-6 and omega-9. The flour, a byproduct of the oil extraction process, contains approximately 40% protein and high fiber content. Beyond its nutritional applications, the crop is integrated into agroforestry systems aimed at restoring degraded lands and promoting biodiversity.

Currently, the cacay value chain involves more than 500 peasant and indigenous families. If approved, the flour would join Colombia’s non-traditional export basket to Europe, reinforcing a bioeconomy model based on fair trade and the sustainable use of biodiversity.

The bank’s analysts say that the increase still doesn’t include the effects of Gustavo Petro’s 23% decreed increase in the country’s legal minimum wage.

According to a report by the Economic, Industry & Market Research Area of Bancolombia (BVC: BCOLOMBIA, NYSE: CIB), annual inflation in Colombia rose by 25 basis points to 5.35% in January 2026. This monthly increase of 1.18% represents the highest inflation level since October 2025.

The data, originally prepared by the National Administrative Department of Statistics (DANE), indicates that 70% of the January inflation print was concentrated in the services and regulated components. These two sectors contributed 83 basis points of the total 118-point monthly increase, largely driven by the initial stages of annual cost pass-throughs associated with high indexation.

Businesses should prepare for more intense inflationary pressures in February and March 2026 as the full impact of the minimum wage increase and renegotiated supplier contracts take effect.

Sectoral Impacts and Service Acceleration

Annual inflation in the services category accelerated by 40 basis points to reach 6.33% in January, its highest level since April 2025. The monthly variation of 1.18% in this sector was nearly double the historical January average of 0.63%.

Bancolombia analysts attribute this acceleration to early adjustments linked to the 23% minimum wage increase for 2026 and indexation to previous years’ inflation. Notable increases were observed in:

Full-service restaurant meals: 3.36%

Prepared meals consumed outside the home: 2.38%

Domestic services: 5.16%

Imputed rent: 0.43%

The regulated group also saw an acceleration, with annual inflation rising to 5.47% from 5.40%. This was primarily explained by adjustments in urban transportation, vehicle fuels, natural gas, and tolls.

Food and Goods Price Momentum

Annual food inflation edged up slightly to 5.10% from 5.06%. Perishable foods saw an acceleration to 4.69% due to seasonal and supply factors affecting products such as tomatoes, potatoes, and plantains. Processed foods, including beef, milk, and poultry, reflected early-year cost pass-throughs, though annual inflation in this sub-group eased to 5.23%.

The goods category reached its highest level since March 2024, at 2.93%. Price hikes in this segment were driven by new taxes on alcoholic beverages enacted under the economic emergency, as well as pharmaceutical products. Conversely, price declines were noted in personal hygiene products, vehicles, and appliances, benefiting from the recent appreciation of the exchange rate.

Monetary Policy Implications and Forecasts

The Central Bank of Colombia (Banco de la República) faces continued challenges in converging toward its 2% to 4% target range. Core inflation, excluding food and regulated items, reached its highest level since November 2024, indicating persistent upward pressure.

Bancolombia forecasts that year-end inflation will reach 6.4%. The analysts suggest that the full impact of the minimum wage increase has not yet been reflected in consumer prices, as many firms are still operating with inventories purchased at previous cost levels.

Consequently, the Central Bank is expected to continue raising its monetary policy rate to anchor inflation expectations. Bancolombia anticipates the policy rate could rise to 11%, noting that the challenging outlook introduces a hawkish bias to future decisions.

The surprise ruling is a temporary win for employers, but creates even more uncertainty. The Council of State has ruled that Petro’s 23% raise in minimum wage violates technical limits established by law.

The Colombian Council of State has issued a provisional suspension of the government decree that established a 23% increase in the national minimum wage for 2026. The judicial decision halts the implementation of the adjustment, which had set the monthly salary at $1,750,905 COP plus a transportation assistance allowance, totaling approximately $2,000,000 COP.

The suspension follows several legal challenges arguing that the administration of President Gustavo Petro exceeded its authority by setting an increase significantly higher than the 5.1% inflation rate recorded in 2025. The court found reasonable doubt regarding whether the executive branch adhered to the technical criteria mandated by Law 278 of 1996, which requires adjustments to be based on inflation, productivity, and economic growth.

Immediate Regulatory Timeline and Compliance

The high court has granted the Ministry of Labor an eight-day window to issue a new provisional decree. During this period, employers are instructed to maintain current payment levels until the new administrative act is published.

Legal experts emphasize that the ruling does not have retroactive effects. Juan Pablo López, managing partner at López & Asociados, told daily El Tiempo that payments made between January 1 and the issuance of the new decree remain valid. Companies are legally prohibited from discounting or requesting the return of the additional 23% already paid to employees for January and the first half of February.

Vicente Umaña, partner at Posse Herrera Ruiz, clarified to the same publication that while payments currently due must honor the 23% increase, the forthcoming decree will likely establish a lower rate. This adjustment will subsequently impact other costs indexed to the minimum wage, including administration fees, fines, and transport costs.

Economic and Labor Market Projections

The initial 23% hike sparked concerns among economic think tanks regarding formal employment and inflation. Fedesarrollo published an analysis suggesting that such an increase could lead to the loss of up to 600,000 formal jobs and a three-percentage-point rise in labor informality.

Economic researchers at Bancolombia (BVC: BCOLOMBIA, NYSE: CIB) estimated potential job losses could reach 734,000. Their data highlights specific sectors at risk:

Professional activities: 390,537 jobs

Commerce: 71,917 jobs

Construction: 54,537 jobs

Manufacturing: 42,774 jobs

According to Medellín-based El Colombiano, Camilo Cuervo, partner at Holland & Knight, noted that the Council of State’s language suggests the original decree may not survive a final merits review. Luis Fernando Mejía, CEO of Lumen Economic Intelligence, indicated that the suspension could serve to stabilize price escalations observed in early 2026.

Business Community and Government Reactions

The National Federation of Merchants (FENALCO) and the National Business Association of Colombia (ANDI) have addressed the ruling. Jaime Alberto Cabal, president of FENALCO, described the suspension as a necessary correction to an adjustment that did not reflect economic realities. Bruce Mac Master, president of ANDI, stated that the ruling establishes important jurisprudence for technical responsibility in wage setting.

Mauricio Montealegre, partner at Pérez-Llorca Gómez-Pinzón, observed that while the government could theoretically attempt to justify the same figure in a new decree, the president has called for a new concertation table to align with the court’s criteria.

Guidance for Employers

Business owners and human resources departments operating in Colombia should consider the following steps:

Maintain Current Payroll: Continue paying the 1,750,905 COP base salary until the new decree is officially published in the government gazette.

Avoid Retroactive Deductions: Ensure that no attempts are made to recoup the 23% increase already paid to staff for previous periods.

Monitor the New Decree: Prepare for a mid-month adjustment in the second half of February, as the new rate will apply immediately upon publication.

Contractual Review: Assess contracts and service agreements tied to the minimum wage to prepare for downward adjustments in indexed costs if the new rate is lower.

Colombian President Gustavo Petro on Sunday mounted a forceful defence of his government’s 23.7% minimum wage increase for 2026, pledging to issue a temporary decree to keep the so-called “vital wage” in place after the Council of State provisionally suspended the original measure.

Speaking in a televised address on Feb. 15, Petro said that while he disagreed with the high court’s decision, he would respect the judicial process and comply by issuing a transitory administrative decree, pending a final ruling.

“The vital wage will remain in place until the new decree is issued,” Petro said, rejecting claims that the increase had triggered inflation or job losses and insisting that workers’ purchasing power must not be subordinated to shifting economic variables.

The Council of State questioned the technical justification and procedural basis of the December decree that lifted the monthly minimum wage to 1.75 million pesos ($470) – close to 2 million pesos including transport subsidies – forcing the government to revisit the measure barely six weeks after it took effect on Jan. 1.

Rather than retreating, Petro escalated the confrontation, calling for nationwide demonstrations on Feb. 19 to defend what he described as a historic social gain for Colombian workers.

“We’ll see each other in all public squares across Colombia,” the president wrote on social media, framing the dispute as a struggle over dignity and constitutional labour rights rather than a technical wage-setting debate.

Petro anchored his argument in Constitutional Court ruling C-815 of 1999, which he said obliges governments to consider not only inflation and productivity but — “with prevailing character” – the constitutional mandate to guarantee a minimum, vital and mobile wage.

Even higher wage not ruled out

In a move that further unsettled markets and business groups, the government signalled that the revised decree could maintain – or even exceed – the original 23.7% increase.

Labour Minister Antonio Sanguino said on Monday that “nothing is ruled out” as the government reconvenes the Permanent Commission on Wage and Labour Policy, bringing unions and employers back to the negotiating table.

The president himself suggested that a true “vital wage” should be closer to 2.15 million pesos, well above the current level.

Sanguino said the commission would review updated economic indicators from the national statistics agency DANE and the finance ministry, including inflation data for early 2026 and labour market trends from 2025.

Inflation and employment debate intensifies

Petro dismissed warnings that the wage hike could fuel inflation or unemployment, arguing that recent data contradict those claims. In a post on “X”, he said that even with Central Bank’s inflation forecasts near 6.4%, wage growth would remain strong and support domestic production and productivity. “It would be a national stupidity to lower the vital wage,”added Petro, affirming also that the country’s first leftist administration would still listen to business leaders.

Economists and employers, however, remain sceptical. Financial analysts claim the suspension highlights institutional concerns over policy predictability, and fear the standoff could undermine investor confidence at a time when Colombia is grappling with deep fiscal debt and high labour informality.

The wage dispute has sharpened tensions between Colombia’s Executive, judiciary and private sector, just three months before first-round presidential elections in May 31.

The outcome of the Council of State’s final ruling – and whether the Executive succeeds in forging a late compromise with employers — will shape not only labour costs in 2026 but also a broader debate over economic governance and the autonomy of the Banco de la República.

For now, the minimum wage remains in legal limbo — enforced by decree, contested in court, and to be defended by his political base this week on the street.

Petro’s emergency order has been put on hold while the constitutional court examines its legality further. What does this mean for your pocket and the country’s future?

More money in your pocket?

For the first time in Colombian history, the constitutional court on Thursday overruled a presidential order and temporarily negated Gustavo Petro’s declaration of an economic emergency. He had done that in order to get his budget through, essentially bypassing the need to get it through parliament. That’s now been put on hold.

The decree hasn’t actually been struck down, just paused while the court makes a decision on the constitutionality of the order. This means weeks of uncertainty while they deliberate. The decision was taken 6-2 with two abstentions, meaning that there’s a clear majority in favour of negation at this point.

#LaCorteInforma | La Corte suspende provisionalmente el Decreto 1390 de 2025 “Por el cual se declara el Estado de Emergencia Económica y Social en todo el territorio nacional”, mientras se profiere una decisión de fondo.

Petro’s declaration of economic, social and ecological emergency was known officially as Decreto 1390 of 22 December 2025. No measures deriving from the decree can be implemented yet, although it will stay formally on the books for now, until the final decision is taken on whether it can stand.

Predictably, he’s reacted furiously to the news, saying that the public should decide. He claims it’s a political decision aimed at protecting the establishment and countering his progressive aims. Furthermore, he says that the court has not properly studied the executive’s arguments.

Cuando desde hace décadas la Corte Constitucional prohibió suspender provisionalmente un decreto de emergencia, la actual Corte Constitucional, sin estudiar nuestras razones, decidió hacerlo.

Se trata literalmente de prejuzgar, pero además se hace por dos razones: por que es un…

Even more provocatively, he’s presenting this as a rupture of constitutional order. This should not be taken lightly: he’s essentially arguing for fewer checks and balances on the presidential office. This is a common theme in caudillo politics and one that many in Latin America will recognise.

The large increase in the minimum salary is being dragged into the argument in what appears to be an attempt to win support for the president’s emergency measures. The latter is a dry matter that few take interest in and the former is something that everyone can see and many support.

While there is little to no chance of the minimum salary increase being revoked, it does stir emotions more effectively than a constitutional affair that many take no interest in. He’s also making the argument that this is class war and the working people should not have to bear the cost of the deficit.

His controversial sidekick Armando Benedetti, currently Interior Minister after a string of previous positions has also come out swinging, saying that the court does not have the right to overrule the head of state and that they are protecting the megarich.

No hay derecho. Al suspender provisionalmente la Emergencia Económica se está protegiendo a los megarricos. pic.twitter.com/0UlK6Elzti

While the ruling by the Corte Constitucional is unprecedented, it was not a big shock. Petro was quite clearly playing politics with the decree and is now dealing with the consequences. It was seen in December as an unusual and authoritarian move which had a good chance of being denied. A freeze was always likely, with full rejection absolutely possible.

The court justified its decision by arguing that the financial problems the country has are not exceptional circumstances that demand emergency measures, such as COVID-19 or a natural disaster. Rather, they are structural problems that require a regular solution.

More tellingly, the tribunal noted that the motivation behind the decree was not clearly defined and likely political. It went on to point out formal irregularities and problems with the legal design of the decree.

There had been significant pushback from elected officials to the plan, with 17 departmental governors refusing to implement decree 1474, a follow-on from the economic emergency decree, claiming it was potentially unconstitutional and that this would put them at financial risk if it failed.

This opens serious questions as to the limits on the president’s power, the position of the constitutional court and the viability of future tax reforms. It also sets the clock ticking for a decision, as the Senate and House elections are coming up fast, on March 8th. If this matter is not resolved by the time presidential elections are happening, things will get complicated.

So what does it mean for my pocket?

In the short term, all the planned tax hikes are frozen. That means there likely won’t be price drops, just that some things that were set to rise significantly won’t do so. In fact, as inflation remains high, expect plenty of sticker shock anyway.

Some booze, yesterday

Full-rate IVA (VAT or sales tax) was due to go onto liquor and wine, so it’s good news for rum drinkers, winos and aguardiente fans. Gamblers, too, have a reprieve as there will also be no IVA increase for online betting. Finally, smokers won’t see extra taxes on tobacco consumption.

The planned USD$50 limitation on tax-exempt gifts won’t go into effect, making buying from overseas relatively cost-effective for a while longer.

The wealth tax will stay where it is for now, with the bar remaining at COP$3.6bn and progressive rates not coming into play. However, those in debt with local tax revenue authority DIAN will not see a reduction in either interest payments or penalties for late payment.

Elsewhere in the economy, the bankers have avoided a 15% extra supertax and there will be no new charges levied on natural resource extraction. The latter were in any case only designed to be temporary.

It’s technically possible, but very unlikely, that monies already gathered will be returned. The corte constitucional has traditionally avoided retroactive economic decisions, preferring to rule in favour of protecting the state’s finances. That means some COP$800bn that has been collected will stay in limbo for now but almost certainly be unfrozen whatever happens.

What happens next?

Immediately, political and economic uncertainty, as this is only a temporary suspension to revise the legal position. That means weeks more of companies not knowing where they stand for the medium term and politicians taking the opportunity to grandstand and indulge themselves.

There are two paths from here: either the court decides that the economic emergency declaration was valid, in which case we simply revert to the original measures set out in the decree, or it is struck down and everything is up in the air.

Petro is correct when he points out that this will mean he has to borrow more to finance the running of the state, which will increase the national debt. The deficit also still stands and continues to grow, meaning in turn so does the debt. This is long-term unsustainable.

Somewhere down the line, a Colombian president will have to do something to address the deficit the country has been running for years since the collapse of the natural resource boom. However, Duque’s attempt to reform the tax system was met with massive protests and Petro has fared no better while also increasing spending.

There are no signs that any of the candidates in this year’s election are likely to fare any better. Expect to see plenty of grandiose plans and vague suggestions but little fine detail in any manifestos. Quite simply, running on a platform of promising to increase taxation is a death knoll for any candidate.

All of the measures that could be taken are politically poisonous. Cutting spending is hard to do once people have become accustomed to it, stealth taxes abound and business rates are already high. A more progressive income taxation system would need to involve widening the tax base, which will mean more voters paying tax for the first time.

For many regular folk, just keeping their head above water is already hard enough without extra costs suddenly appearing. They won’t vote for more taxes, or even any taxes, as many are simply not taxed directly. At the same time, without significant natural resources popping up, the only way out of the middle-income trap is tax reform.

There’s also the question of the role played by the constitutional court. While nominally independent, it is supported or decried by all sides of the political spectrum depending on who it’s perceived to favour at any one point. There are already calls to ignore it in the name of the ‘people’s will’, conveniently undefined. Expect those to grow in number.

Where will Colombia go in the short term? Probably nowhere, as kicking the can down the road is still possible for a few years more. It’s likely that state spending will slow down, minor budgetary changes will get through and the country will muddle along.

Having already lost investment grade status after Duque’s botched reform, the country hasn’t much to lose for now. There are also promising economic signs, meaning that strong GDP growth could alleviate the situation considerably. However, the national debt will be hanging like the sword of Damocles over future presidents.

A federal jury in the United States has awarded coal producer Drummond Company Inc. $256 million after finding that a prominent human-rights attorney and his associates orchestrated a campaign of false accusations linking the company to paramilitary violence in Colombia.

The verdict, delivered on January 15 in the U.S. District Court for the Northern District of Alabama, marks one of the largest legal victories Drummond has secured in its long-running effort to counter claims alleging ties to illegal armed groups during Colombia’s internal conflict.

Jurors ruled unanimously that Washington-based attorney Terrence P. Collingsworth and his organization, International Rights Advocates (IRAdvocates), knowingly made false and defamatory statements accusing Drummond of financing paramilitary organizations operating in Colombia. The panel also found that Collingsworth and IRAdvocates violated the Racketeer Influenced and Corrupt Organizations Act (RICO), determining they engaged in a coordinated scheme involving extortion, bribery of witnesses, witness tampering, wire fraud, money laundering, obstruction of justice and conspiracy.

According to court filings and testimony presented at trial, the defendants allegedly used fabricated narratives and paid testimony to pressure Drummond through lawsuits and media campaigns in the United States, Colombia and Europe. Jurors concluded there was “clear and convincing evidence” that Collingsworth either knew his claims were false or acted with reckless disregard for the truth.

Drummond had brought two lawsuits against Collingsworth and his network: one alleging defamation and another invoking the federal RICO statute. The jury awarded $52 million in damages for defamation and $68 million under the RICO claims. Under U.S. law, RICO damages are automatically tripled, bringing the total award to $256 million.

The case centered heavily on payments made to Colombian witnesses who had testified in earlier lawsuits accusing Drummond of supporting right-wing paramilitary groups. Evidence showed that more than $400,000 had been paid to individuals including Jaime Blanco Maya and Jairo de Jesús Charris, also known as “El Viejo Miguel,” without disclosure to courts.

The jury further found that other alleged co-conspirators were involved in the broader scheme, including Colombian attorney Iván Alfredo Otero Mendoza and Dutch businessman Albert van Bilderbeek, both of whom were also held liable under RICO.

Drummond’s lead trial counsel, Trey Wells of Starnes Davis Florie LLP, said the verdict vindicated the company after decades of reputational damage. “This verdict is further proof that Drummond has never had any ties whatsoever to illegal armed groups,” Wells said in a statement. “For years the company endured malicious accusations and false narratives that have now been categorically rejected by an American jury.”

Drummond has operated in Colombia since the late 1980s and is one of the largest exporters of Colombian coal. The company has faced multiple lawsuits over the past two decades in U.S. courts alleging it supported paramilitary groups blamed for killings near its mining operations — claims Drummond has consistently denied. The Company said the ruling exposesd a coordinated effort to damage Drummond’s reputation and extract financial settlements through legal pressure based on false testimony. “The case documents demonstrate a deliberate strategy to harm Drummond commercially and reputationally through fabricated allegations,” the company noted.

Drummond reiterated its commitment to ethical operations in Colombia, stressing that it has complied with national laws since beginning activities in the country and maintains strict corporate governance standards.

The verdict is expected to have far-reaching implications for ongoing and future transnational litigation involving corporate accountability claims, particularly cases reliant on testimony sourced in conflict zones.

A new analysis released by the Observatorio Fiscal de la Pontificia Universidad Javeriana reveals that Colombian municipalities remain heavily dependent on the central government for funding, with 50% of their total income derived from national transfers. The report highlights a significant lack of fiscal autonomy, particularly among smaller municipalities, and points to structural disparities in local revenue generation for the year 2024.

According to the data presented by the university, total territorial income in Colombia reached $197.5 trillion COP in 2024. Of this aggregate figure, municipalities accounted for $146.5 trillion COP, while departments received $51 trillion COP.

The breakdown of these municipal funds indicates that transfers from the nation were the primary source of liquidity, totaling $72.8 trillion COP. Own-source revenue (resources generated locally) amounted to $49.6 trillion COP (34%), while capital resources contributed $24.1 trillion COP (16%). The observatory notes that this structure demonstrates a high dependence on conditioned resources, which limits the ability of local governments to make independent fiscal decisions.

Disparities in Local Revenue Generation

The report emphasizes that fiscal autonomy is directly linked to the generation of own resources, which totaled $49.6 trillion COP for the period. Of this amount, 86% corresponded to tax revenues and 14% to non-tax revenues. However, the distribution of these funds is highly uneven across the country’s 1,103 municipalities.

Only municipalities classified as “Special Category”—typically major urban centers—finance more than half of their budgets through own resources. In contrast, municipalities in categories four through six, which often represent smaller or rural towns, generate only 15% to 20% of their funding locally. The Pontificia Universidad Javeriana researchers attribute this gap to differences in economic and administrative capacities between regions.

Taxation and Structural Challenges

In terms of tax revenue, municipalities collected $42.7 trillion COP in 2024. The Industry and Commerce Tax (ICA) was the largest contributor, generating $17.2 trillion COP (40% of tax revenue), followed by the Property Tax (Predial) at $12.4 trillion COP (29%).

While these two taxes are the primary revenue drivers for larger cities, their weight diminishes significantly in smaller municipalities. In these areas, local governments rely more heavily on gasoline surcharges and “estampillas” (fiscal stamps), which can sometimes constitute the primary source of tax income. The observatory warns that outdated cadastral (property) valuations and the heterogeneity of the ICA tax structure continue to limit the efficiency of the territorial tax system.

Non-tax revenues, such as fines, fees, contributions, and the sale of goods and services, totaled $6.9 trillion COP. These sources are particularly critical for category four through six municipalities, helping to offset weaker tax collection capabilities.

Dependence on the General System of Participations (SGP)

The report provides detailed statistics on the extent of reliance on the General System of Participations (SGP), the main mechanism for national transfers. In 2024, the SGP contributed $46.1 trillion COP, representing 63% of all national transfers.

The level of dependence is widespread:

In 695 municipalities, the SGP represents at least 40% of total income.

In 332 municipalities, it represents 50% of total income.

In 95 municipalities, it accounts for more than 60% of total income.

While recent reforms to the SGP are expected to increase these resource flows, the observatory states that the positive impact will depend on improved management capacity and the avoidance of budget under-execution in smaller jurisdictions.

Capital Resources and Budget Execution

A key concern raised in the report is the composition of capital resources, which reached $24.1 trillion COP. These funds are dominated by “recursos del balance”—unexecuted balances from previous fiscal years—which represent 55% of the total capital resources. The high prevalence of these rollover funds suggests a low capacity for budget execution in a large portion of Colombian municipalities.

The Observatorio Fiscal concludes that the combination of high transfer dependence, weak local revenue generation, limited credit access, and low budget execution restricts local autonomy and deepens economic gaps between municipalities. The organization suggests that strengthening tax collection and administrative capabilities are essential steps toward effective fiscal decentralization.