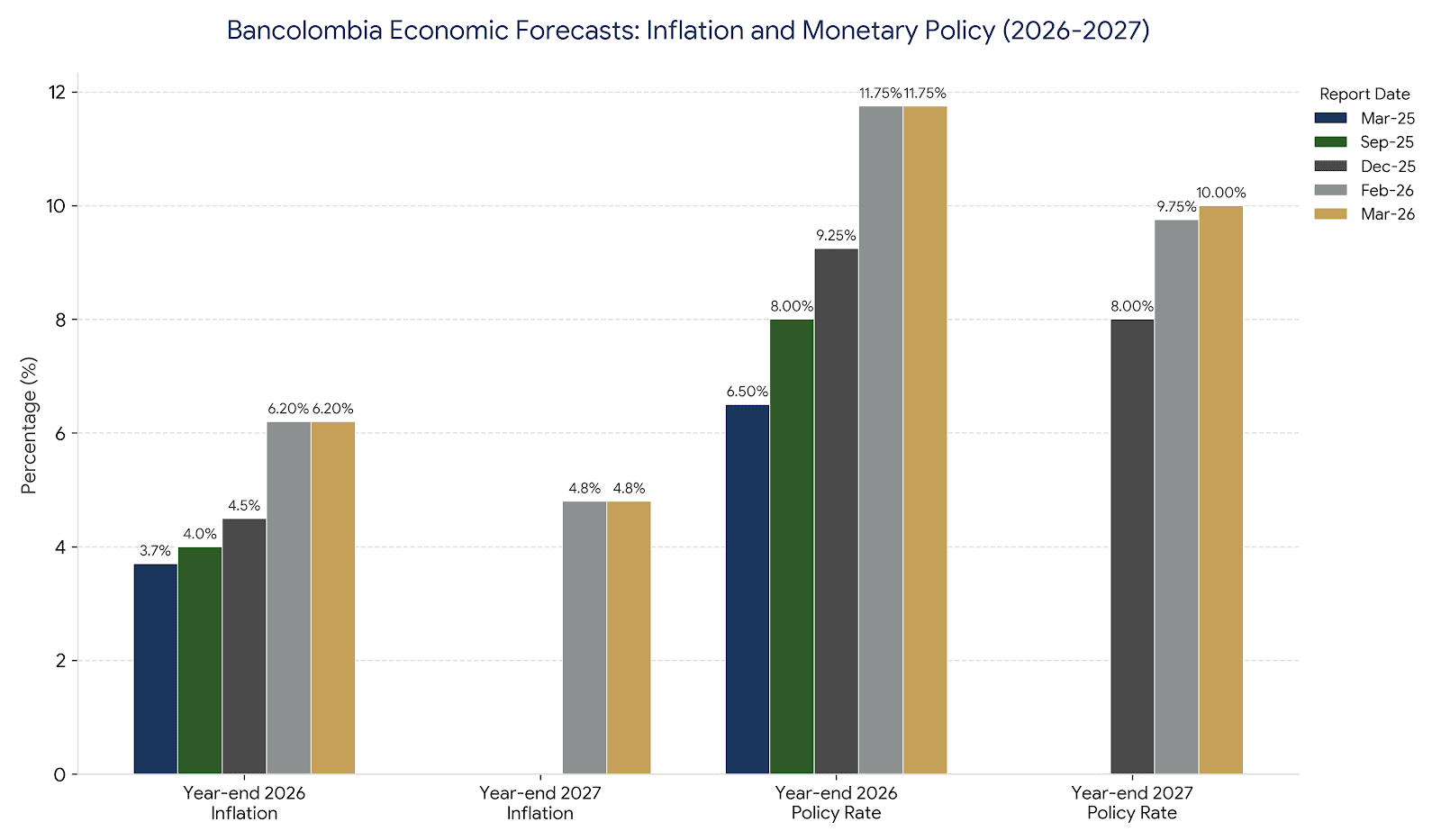

El Niño Warming Patterns Signal Operational Risks for Colombian Power and Agriculture

Escalating drought risk is potential bad news for rural communities, power consumers.

The National Oceanic and Atmospheric Administration (NOAA) and the Climate Prediction Center (CPC) have confirmed that ENSO-neutral conditions are currently present in the equatorial Pacific Ocean. However, technical indicators suggest a rapid transition, with a 61% probability of El Niño emerging between May and July 2026. For international investors and executives operating in Colombia, this shift indicates a looming period of increased operational costs, specifically within the energy and agricultural sectors.

The El Niño Southern Oscillation (ENSO) is a recurring climate pattern involving changes in the temperature of waters in the central and eastern tropical Pacific Ocean. During El Niño, trade winds weaken, allowing warm water to move toward the west coast of South America. Conversely, La Niña is characterized by stronger trade winds and cooler ocean temperatures. These fluctuations disrupt global atmospheric circulation, altering rainfall and temperature patterns across the planet.

In Colombia, the effects of these phenomena are distinct and significant. El Niño typically results in a sharp decrease in precipitation and a rise in average temperatures. Because Colombia relies on hydroelectricity for more than 60% of its total power generation, extended dry periods lead to lower reservoir levels. This forces the grid to rely on more expensive thermal generation fueled by natural gas and coal, which historically drives up spot market electricity prices for industrial and residential consumers.

“There is a 25% probability that the index reaches or exceeds +2.0°C during the Northern Hemisphere winter,” according to the National Oceanic and Atmospheric Administration.

The current technical diagnostic from NOAA shows that while the sea surface temperature index in the Niño-3.4 region was recently -0.2°C, the easternmost indices have already moved into positive territory. Furthermore, the equatorial subsurface temperature index has increased for five consecutive months. This accumulation of ocean heat is a primary driver behind the high probability of El Niño persistence through the end of 2026. Some models, including those from the European Centre for Medium-Range Weather Forecasts (ECMWF), suggest a 25% chance of a “strong” or “very strong” event, where temperatures exceed the 2.0°C anomaly threshold.

The Ministerio de Minas y Energía and the Comisión de Regulación de Energía y Gas (CREG) are monitoring these developments closely. A strong El Niño would place additional stress on a natural gas system already facing structural supply constraints. Reduced hydroelectric output coupled with a potential deficit in gas supply could lead to significant energy price volatility. In past events, such as the 2015-2016 cycle, these conditions resulted in substantial financial pressure on the national utility system and necessitated emergency conservation measures.

Agricultural productivity is equally at risk. The Instituto de Hidrología, Meteorología y Estudios Ambientales (IDEAM) has identified the Caribbean and Andean regions—including departments such as La Guajira, Magdalena, and Antioquia—as highly vulnerable. During El Niño, these areas face increased risks of forest fires, water scarcity, and crop failure. For agribusinesses and exporters, this translates to disrupted planting cycles and higher production costs for staples like corn, potatoes, and vegetables, which can fuel domestic food inflation.

Conversely, when La Niña is in effect, Colombia faces the opposite extreme. The cooling of the Pacific leads to excessive rainfall, which can cause devastating landslides and flooding in mountainous terrain. While La Niña can replenish reservoirs, it often damages infrastructure and logistics networks, complicating the transport of goods to port. The current transition out of a La Niña phase provides a brief window of ENSO-neutral stability, which the CPC estimates has an 80% chance of lasting through June 2026.

For the international business community, the significance of these weather cycles extends to macro-economic stability. Persistent dry weather can impact GDP growth by raising the cost of basic services and reducing agricultural output. Strategic planning for 2026 and 2027 must account for these climatic variables. Meteorologists at Colorado State University note that El Niño also tends to reduce hurricane activity in the Atlantic, which may provide some relief for coastal logistics, but the primary threat remains the inland hydrological deficit.

As the Ministerio de Ambiente y Desarrollo Sostenible activates preventive mechanisms, companies are encouraged to review their energy procurement strategies and water management protocols. The next comprehensive diagnostic update from NOAA is scheduled for May 14, 2026, which will provide further clarity on the intensity of the projected warming trend. Understanding the mechanics of the ENSO cycle is no longer a matter of environmental interest but a necessity for risk mitigation in the Colombian market.

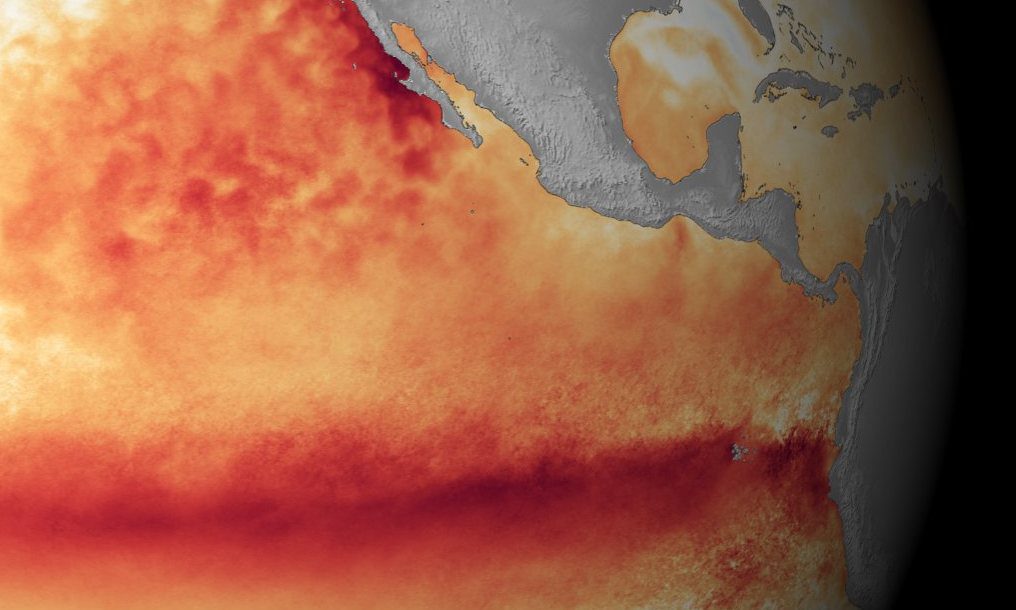

Satellite sea surface temperature departure in the Pacific Ocean for the month of October 2015, where darker orange-red colors are above normal temperatures and are indicative of El Niño. (Image credit: NOAA)

Headline photo: the Pacific Ocean from Guachalito Beach, Chocó, Colombia (photo © Loren Moss)