Fitch Analysis: Colombia’s High-Stakes Election Runoff to Shape Economic Policy

Fitch: June 21 Runoff Will Shape Colombia’s Fiscal Path

Colombia’s June 21 presidential runoff will have a significant bearing on the country’s economic policies and prospects, Fitch Ratings said in a commentary published this week.

In the first round of voting on May 31, right-wing candidate Abelardo de la Espriella — running under the Defensores de la Patria movement — received 43.7% of votes, defeating leftist senator Iván Cepeda of the governing Pacto Histórico, who received 40.9%. Neither candidate reached the absolute majority required to win outright, sending the election to a runoff.

De la Espriella’s stronger-than-expected first-round performance prompted a positive reaction in financial markets, reflecting expectations that he may be better positioned to address Colombia’s macroeconomic challenges that have intensified under outgoing President Gustavo Petro.

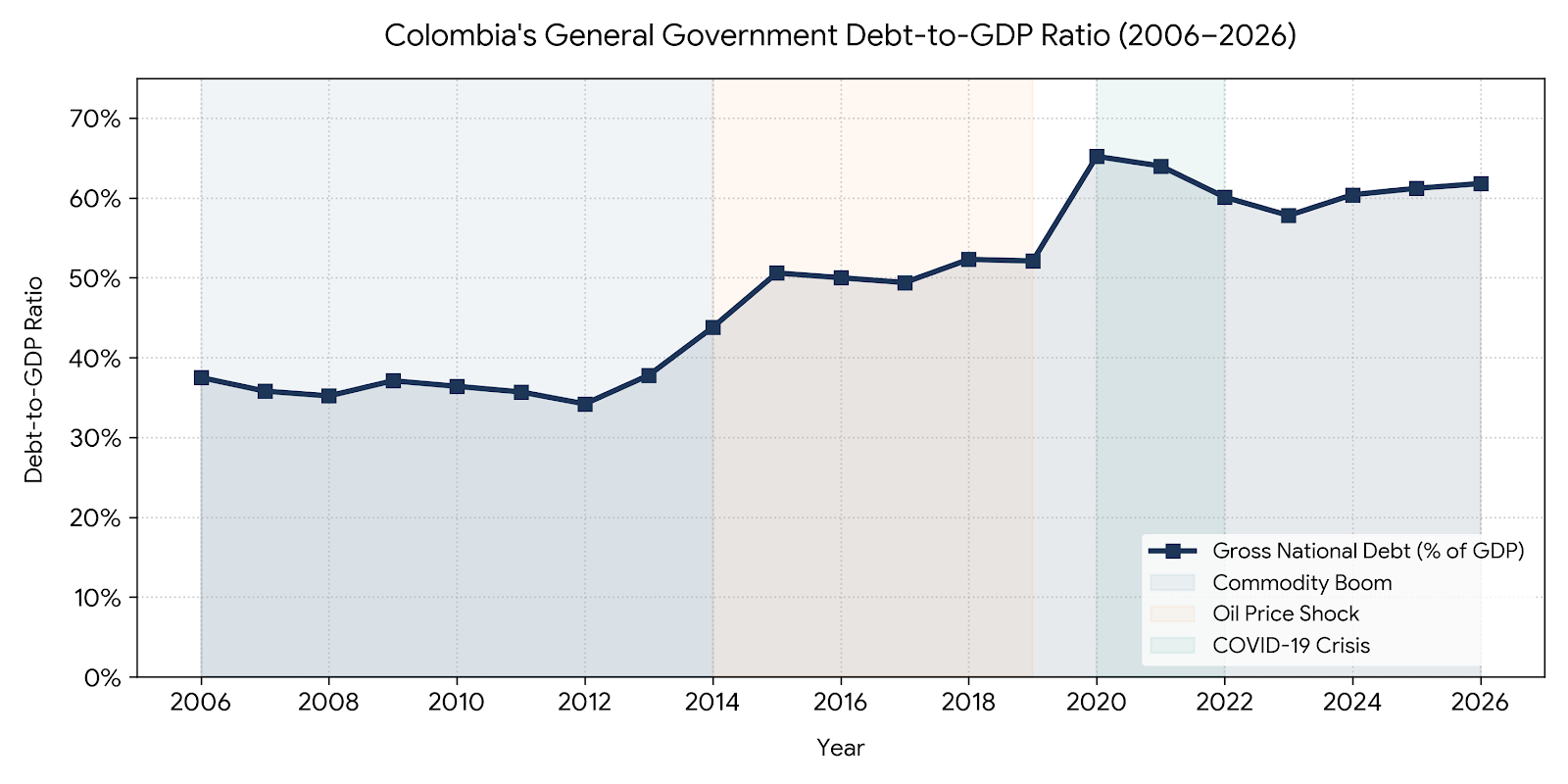

The next president will face the challenge of addressing Colombia’s wide fiscal imbalance. The central government deficit reached 6.4% of GDP in 2025, or 7.8% when net of a temporary reduction in interest costs from liability management operations. Fitch estimates that debt stabilization will require a fiscal adjustment equivalent to 4% of GDP. Higher global oil prices are expected to boost revenues via taxes and dividends in 2027, but Fitch cautioned that this support may not last.

“De la Espriella’s stronger-than-expected first-round performance prompted a positive reaction in financial markets, reflecting expectations that he may be better positioned to address Colombia’s macroeconomic challenges.” — Fitch Ratings

De la Espriella has pledged fiscal consolidation through a 40% reduction in the size of the state, while Cepeda has proposed restraining public-sector salaries and benefits. Budget rigidities and spending pressures tied to pensions, healthcare, and subnational transfers will make either adjustment difficult. Both candidates have also proposed higher spending — on defense and social welfare respectively. Capital spending could be trimmed as an adjustment variable, but only to a limited extent, with 2025 outlays of 2.7% of GDP.

The interest bill will be another source of pressure amid a higher local yield curve. Recent liability management operations have replaced lower-coupon bonds with higher-coupon ones, providing an up-front financial benefit while increasing future interest costs.

Given these spending constraints, durable fiscal consolidation is likely to require revenue-side measures. Colombia has a history of tax reforms, but new legislation is far from assured. De la Espriella has pledged to cut taxes, and while Cepeda supports revenue-raising measures, he could face obstacles in advancing reforms through Congress — as Petro’s administration found.

Uncertainties about Colombia’s trend growth persist. The economy expanded at an annual rate of 2.5% in 2019–2025, below the ‘BB’ median and below its own prior average of 3.5%–4%, supported by government transfers, a strong labor market, and minimum wage increases that kept private consumption buoyant at +4.2%. In contrast, investment contracted by an average of 1.6% annually, falling to 16% of GDP from 21%, affected in part by business concerns about the Petro administration’s more interventionist policy stance.

De la Espriella has pledged to boost growth through promotion of hydrocarbon development — including fracking — alongside tax cuts and steps to reduce administrative burdens on businesses. Cepeda has pledged continuity with Petro’s state-led development model, without concrete proposals to revive private investment.

Both agendas face implementation challenges. The next legislature will remain fragmented, requiring negotiation to pass any major legislation. As a political newcomer, de la Espriella could encounter difficulty advancing his program should he win. Social protests are a risk, particularly regarding his plans to cut spending and adopt a tougher security stance.

The election could also influence monetary policy, with implications for financial conditions and thus for public finances and growth. Despite rising inflation, the Banco de la República (Banrep) voted to hold its policy rate at 11.25% after swift prior increases of 200 basis points, amid explicit pressure from the executive branch for looser policy. The elections could influence Banrep’s next steps starting with its June 30 board meeting, and will also determine who fills two vacancies on its seven-member board in 2029.

Fitch’s downgrade of Colombia to ‘BB’/Stable in December 2025 reflected the agency’s view that the starting point for public finances had weakened considerably, and that improvement would take time regardless of the election outcome. Faster-than-expected fiscal adjustment, higher growth, and lower real rates that support debt stabilization could be positive for the rating. A worsening of these variables that steepens the debt trajectory could be negative.

Above image: Fitch Ratings