Analysis: In Sunday’s Election, Many Colombians Rejected The Political Status Quo. A Stark Right-Left Choice Remains

Colombia’s Runoff Could Reshape Investment, Energy, and Labor Policy

Colombia’s first-round presidential election, held Sunday, May 31, 2026, produced a result that crystallizes the country’s political exhaustion with both the governing left and the traditional right. Criminal defense attorney and political outsider Abelardo de la Espriella placed first with more than 10.3 million votes. Leftist Senator Iván Cepeda, a close ally of outgoing President Gustavo Petro and the lead architect of the administration’s Paz Total peace policy, finished second with just under 9.7 million votes. The two will face each other in a runoff election on June 21.

Senator Paloma Valencia, the candidate backed by former President Álvaro Uribe and the standard-bearer of his Uribismo movement, placed a distant third, receiving less than 7% of the vote — fewer than 1.7 million ballots. Former Medellín mayor and Antioquia governor Sergio Fajardo received just over one million votes, while former Bogotá mayor Claudia López finished below 1%, with approximately 225,000 votes. The remaining minor candidates combined for just over 1% of the total.

Under Colombia’s electoral system, the top two finishers advance to a runoff if no candidate surpasses 50% in the first round. The June 21 vote will determine who assumes the presidency on August 7.

Click above to watch the video!

The Candidates: Background and Context

Abelardo de la Espriella, 47, has never held elected office. He built a national profile over more than two decades as a high-profile defense attorney, founding De La Espriella Lawyers in 2002, with offices in Colombia and the United States. His client roster has included controversial figures: he represented Alex Saab, a Colombian-born businessman who became a close associate of Venezuelan President Nicolás Maduro and was implicated in a scheme to launder proceeds from Venezuela’s food-assistance program, the Comité Local de Abastecimiento y Producción (CLAP). Saab was extradited to the United States, convicted, and later granted clemency before being re-arrested in Venezuela in early 2026. De la Espriella also represented members of the Nule family in connection with the Carrusel de Contratos — a major contracting scandal tied to infrastructure works at Bogotá’s El Dorado airport corridor. He has additionally been reported to have represented individuals linked to organized crime.

De la Espriella has drawn comparisons to figures such as US President Donald Trump and El Salvador’s Nayib Bukele. His campaign has centered on hard-line security policy, including proposals for large-scale incarceration, expanded military operations against armed groups, and the rejection of negotiations with guerrilla organizations. He is reported to hold Italian and US citizenship in addition to his Colombian nationality, and is said to own property in Florida.

In a notable departure from his defense work, de la Espriella took the side of a victim in a high-profile acid-attack case, acting as a private prosecutor to secure a stronger sentence for the perpetrator — an episode that raised his public profile beyond the defense bar.

Iván Cepeda, 63, enters the runoff as the consolidated candidate of the Colombian left and Petro’s Pacto Histórico coalition. He is the primary legislative architect of Paz Total, the Petro administration’s policy of negotiating simultaneously with multiple armed actors, including the ELN and FARC dissident factions. Cepeda’s family background includes deep ties to the Colombian left: his father was secretary general of the Communist Party, and was assassinated. Cepeda himself studied in communist Bulgaria during the soviet era. The two finalists have an established legal and political history: Uribe attempted to bring criminal charges against Cepeda while both served in the Senate, but the Supreme Court determined that Uribe had fabricated the accusations and attempted to bribe witnesses — a case that resulted in Uribe’s criminal conviction.

“If nothing changes, Abelardo wins.” — Loren Moss, Finance Colombia

The Electoral Map

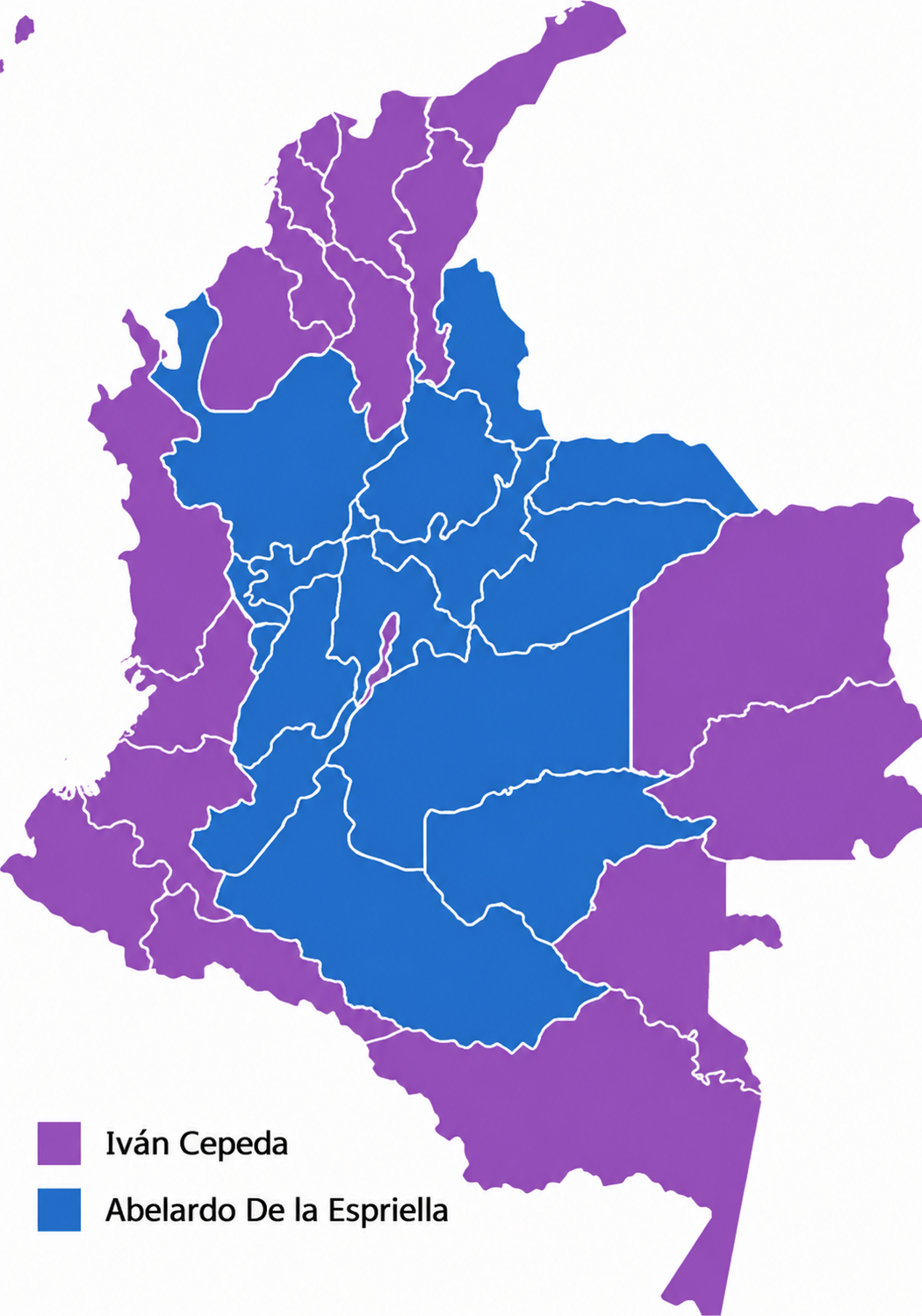

The geographic distribution of the vote reflects deep regional divisions. Cepeda carried Bogotá, which has trended left for years, particularly in lower-income districts on the city’s south and west sides. Antioquia — historically the heartland of Uribismo and home to Medellín, the country’s second-largest city — voted more than two to one for de la Espriella, a result that signals the weakening grip of Uribe’s movement even in its traditional stronghold.

The heart of coffee-growing country — the departments of Caldas, Risaralda, and Quindío also went to de la Espriella. Caquetá, a sparsely populated department in southern Colombia that has suffered sustained guerrilla violence from both the ELN and FARC dissident groups, voted for de la Espriella as well, a result we may interpret as a direct rejection of Petro and Cepeda’s Paz Total.

Cepeda carried Colombia’s Pacific coast, including the chronically neglected department of Chocó, as well as the sparsely populated Amazonas and Putumayo departments bordering Peru and Brazil, and the northern Caribbean coast. The Caribbean coast result is notable, as the region has historically suffered from underdevelopment, infrastructure deficits, and significant income inequality. Norte de Santander with its Catatumbo region on the Venezuelan border and experiencing severe armed-group activity — voted for de la Espriella, a result consistent with public exhaustion over security policy.

The Political Context: From Uribe to Petro and Beyond

Colombia’s current political trajectory is rooted in decisions made across the past two decades. President Uribe served two terms in the early 2000s and, together with then-Defense Minister Juan Manuel Santos, mounted a sustained military campaign against the FARC that significantly weakened the insurgency. Santos later broke from Uribe after assuming the presidency, governing independently and ultimately negotiating a peace agreement with the FARC — a deal that Uribe actively opposed. A plebiscite on the accord failed, but Santos used legislative maneuvering to implement it anyway.

Colombia 2026 1st round top two (Graphic: Sofi Imfeld for Finance Colombia)

Uribe’s next handpicked candidate, Iván Duque, won the 2018 election but finished his term with approximately 30% approval. Members of his own party publicly distanced themselves from him — Senator María Fernanda Cabal, a staunch Uribista, called Duque a “mamerto” (leftist idiot) while he was still in office. Under his administration, indicators on crime and guerrilla activity worsened, and armed groups including the ELN rebuilt operational capacity that had been degraded under Uribe and Santos.

Petro’s administration has not met initial fears of a Venezuelan-style democratic breakdown: Congress has largely blocked the most radical components of his agenda, including attempts to nationalize the private pension system and convert the healthcare system to a single-payer model. However, crime has increased, armed groups have expanded their operational footprints, and the security situation in several regions has worsened. Paz Total is widely seen as having produced few tangible results.

Uribe himself was convicted of witness tampering and attempted bribery in the case he had brought against Cepeda. Though released from house arrest after conviction, the judges who authorized his release are now reportedly under investigation for judicial corruption. Valencia’s poor performance in the first round — despite being Uribe’s chosen standard-bearer — suggests that Uribismo as a political force is waning, with its core constituency aging and new generations of voters disengaged from the Uribe legacy.

What to Expect Before June 21

Both campaigns will intensify mobilization efforts over the coming three weeks. Cepeda’s movement — Colombia Humana and the broader Pacto Histórico coalition — has historically relied on organized mobilizations, including indigenous community-led mingas, labor unions, and allied social movements. Cepeda’s running mate Senator Aida Quilcué is an indigenous activist, a choice expected to energize those constituencies. FECODE, the Federación Colombiana de Trabajadores de la Educación (Colombia’s main teachers’ federation), is expected to align officially with Cepeda, though individual teachers may not follow union leadership in their voting choices.

On the right, Paloma Valencia issued a public endorsement of de la Espriella immediately following the first-round results. Business community organizations, including ANDI (the Asociación Nacional de Empresarios de Colombia) and Fenalco (the Federación Nacional de Comerciantes), do not formally endorse candidates, but their members are widely understood to favor a government that supports private enterprise and market-oriented policy. De la Espriella holds no congressional constituency, meaning whichever candidate wins will face the same dynamic Petro encountered: a fragmented Congress that is likely to act as a check on executive authority.

The question of centrist voter alignment remains open. Fajardo and López are not expected to formally endorse either finalist, and the direction of their combined approximately 1.2 million votes is uncertain.

Winners and Losers by Sector

For international investors and executives operating in Colombia, the policy differences between the two candidates are substantive across several key sectors.

Petroleum and Natural Gas: De la Espriella has stated unequivocally that he will restart petroleum exploration and licensing, which the Petro administration blocked. Ecopetrol S.A. (NYSE: EC; BVC: ECOPETROL), Colombia’s state-controlled oil company, which also holds producing assets in the US Permian Basin and Gulf of Mexico, has operated under a government that halted new drilling permits. The consequences have included a decline in future production capacity at a time when global oil prices have risen due to Middle East tensions. Colombia has been forced to import natural gas at elevated prices to meet existing domestic demand — including from transportation fleets that were converted to natural gas under government incentive programs. Cepeda would be expected to continue or deepen current restrictions on fossil fuel expansion.

Healthcare: The Petro-Cepeda platform favors a government single-payer model. The administration has already taken over several Entidades Promotoras de Salud (EPS) — Colombia’s managed-care intermediaries — placing the healthcare system in legal and financial uncertainty. Private clinics, hospitals, and physicians who wish to operate outside a government-controlled framework would benefit from a de la Espriella administration. Cepeda’s healthcare agenda would accelerate the shift toward government-managed care.

BPO, Tech, and Call Centers: The BPO sector — which provides large volumes of formal employment, particularly in Medellín, Bogotá, Cali, and Barranquilla — was significantly affected by Petro-era minimum wage increases of 16% and 23% in successive years. These increases created contract renegotiation pressures with international clients, some of whom have shifted or considered shifting operations to competing jurisdictions including Honduras, Jamaica, the Dominican Republic, Mexico, and Guatemala. At the CX Summit, the industry’s main annual event held in Cartagena, the son of Álvaro Uribe appeared as an invited keynote speaker — a gesture that could be interpreted within the industry as an implicit signal of political alignment. A de la Espriella government, with its orientation toward labor market deregulation and reduced regulatory burden, would be viewed more favorably by this sector. Current Colombian labor law prohibits part-time employment contracts and places significant restrictions on dual employment, making workforce flexibility difficult for businesses that operate outside traditional 40-hour weekly structures.

Mining: The Petro administration has been less aggressive toward mining than toward petroleum, but sector participants expect a more permissive regulatory environment under de la Espriella, and continued constraints under Cepeda.

Security and Tourism: Both candidates have stated support for tourism promotion, but the sector’s trajectory is more directly linked to security conditions. Under current policies, several regions that were accessible to domestic and international travelers several years ago have experienced increased armed-group activity, effectively closing them to tourism. A de la Espriella administration is expected to pursue a more aggressive military posture toward the ELN and FARC dissident factions; a Cepeda government would likely continue dialogue-first approaches. The outcome will directly affect which parts of Colombia’s territory remain accessible to investment and tourism.

Foreign Relations: A de la Espriella government is expected to restore a broadly cooperative relationship with the United States, which deteriorated under Petro following several high-profile diplomatic incidents. De la Espriella has expressed admiration for US President Donald Trump, and reports indicate he holds US citizenship and owns property in Florida. Relations with Ecuador, which have been strained by mutual tariff escalations between Petro and Ecuadorian President Daniel Noboa, would be expected to normalize. Relations with Venezuela under Cepeda would likely continue along the current allied trajectory, while a de la Espriella government would be expected to take a more critical posture toward Caracas. China and Russia would find a more receptive diplomatic environment under Cepeda, and a cooler one under de la Espriella.

The Poor and Informal Workers: Cepeda’s campaign argues that minimum wage increases and expanded state services benefit lower-income Colombians. Critics counter that elevated formal labor costs have pushed more employment into the informal sector — which currently accounts for approximately half the Colombian workforce — depriving those workers of pension contributions, health benefits, and job security. De la Espriella’s platform, which emphasizes business formation, security, and labor market deregulation, would be presented as generating more formal-sector job creation. The actual distributional effects of either approach remain contested.

The Outlook

Assuming current polling trends hold and Uribista voters consolidate behind de la Espriella as expected following Valencia’s endorsement, de la Espriella enters the runoff as the frontrunner. Cepeda’s path to victory depends on driving high turnout among his base, securing support from centrist voters who did not vote for either finalist in the first round, and potentially benefiting from any missteps by de la Espriella in the final three weeks of campaigning.

The first-round results produced no major electoral violence. The ELN announced a temporary halt to armed actions during the voting period. Authorities detained some individuals reportedly attempting to purchase votes in rural areas, but no large-scale incidents were recorded.

The incoming president will face a Congress with no natural majority aligned to the executive, a healthcare system in partial administrative disarray, a petroleum sector whose future production trajectory is in question, and regions where state presence remains contested by armed groups. The June 21 runoff will determine which vision — market-oriented restructuring or continuation of the Petro project — Colombia pursues for the next four years.