Colombia Launches English-Language Portal to Attract Foreign Portfolio Investors

New microsite gives foreign investors English-language access to Colombian capital markets

A new English-language microsite aimed at foreign portfolio investors in Colombia’s capital markets went live June 3, the product of a public-private working group that has been operating since late 2023. The platform, called “Foreign Portfolio Investor,” is accessible through the website of the Financial Superintendency of Colombia (Superintendencia Financiera de Colombia, SFC) at superfinanciera.gov.co.

The microsite offers information in English on the structure of the Colombian capital market, its participants, operating procedures covering enrollment, ongoing participation and divestment, issuers and issuances, links to statistical data, applicable regulations, and frequently asked questions. The initiative operates under the broader program titled Mercado de Capitales en Colombia, Colombia Destino de Inversión (Capital Markets in Colombia, Colombia Investment Destination).

The web page can be reached at: https://www.superfinanciera.gov.co/publicaciones/10115712/foreign-portfolio-investor/

“Historically, foreign investors have faced the challenge of understanding the functioning of the Colombian securities market,” said SFC Financial Superintendent César Ferrari (above photo). “The new microsite is a first step in addressing this challenge by offering, in clear English, information necessary to make foreign portfolio investments in Colombia.”

The working groups behind the project brought together several government bodies, including the Banco de la República, the Financial Regulatory Unit (Unidad de Regulación Financiera, URF) of the Ministry of Finance, and the National Tax and Customs Directorate (Dirección de Impuestos y Aduanas Nacionales, DIAN). From the private sector, the Securities Market Self-Regulator (Autorregulador del Mercado de Valores, AMV) and the Colombian Stock Exchange (Bolsa de Valores de Colombia, BVC: BVC) contributed to the platform’s development.

Carlos Emilio Betancourt Galeano, Director General of the DIAN, said the microsite addresses a core barrier to attracting foreign capital. “Providing clear and easily accessible information reduces barriers, improves understanding of the regulatory environment and strengthens the confidence of international investors,” he said.

URF Director Larisa Caruso said the platform addresses language as a structural obstacle to market participation. “This microsite represents an important milestone to strengthen the internationalization of the Colombian capital market and will allow foreign investors to better understand the regulation and the particularities of the local market, promoting greater transparency, trust and access to information, while contributing to reducing entry barriers associated with language,” she said.

AMV President Hernán Alzate described the launch as part of a longer-term positioning effort. “It represents a decisive step to position Colombia as an attractive and reliable destination for international investment,” he said. “Facilitating access to clear and timely information is critical to strengthening foreign investor confidence in an increasingly interconnected world.”

Andrés Restrepo Montoya, CEO of the BVC, framed the microsite as part of the exchange’s ongoing efforts to draw international capital. “To attract investment we must also facilitate access to clear and reliable information,” he said. “This is an important step to bring foreign investors closer to the Colombian capital market.”

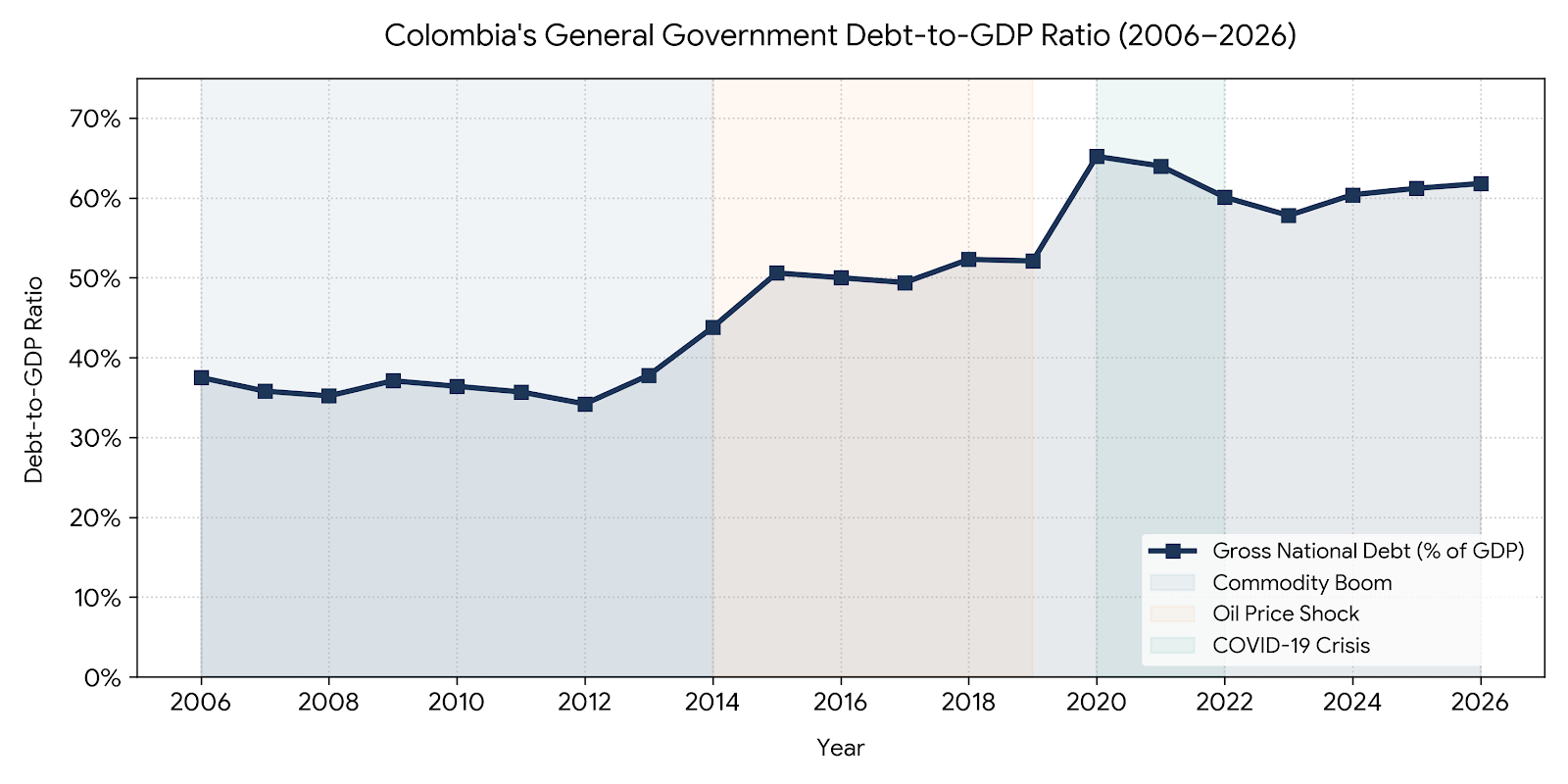

The initiative comes as Colombia’s capital markets face scrutiny from international investors and ratings agencies over the country’s fiscal trajectory. The working group structure that produced the microsite has been active since late 2023, with the SFC serving as lead coordinator across multiple public and private stakeholders.