Inside the Congolese Hotel Where Trump Deported 15 U.S. Migrants

They were shackled and sent to Kinshasa by the Trump administration. Now they face a dangerous choice: Go back to Latin America or stay in Africa.

At a time when children are increasingly indoors – absorbed by screens, separated from the street and distanced from the spontaneous rituals of neighborhood play – a new exhibition by the Banco de la República has launched at the Museo de Arte Miguel Urrutia (MAMU), and one that asks a deceptively simple question: what happened to playing outside with friends?

Having opened on April 23 at El Parqueadero and second floor of MAMU, Francis Alÿs, juegxs de niñxs 1999–2025 brings together 27 video works from the Belgian-born, Mexico-based artist’s celebrated long-running series documenting children’s games across the world.

Curated by Cuauhtémoc Medina and Virginia Roy, the exhibition proposes something more than nostalgia. It invites viewers to see play as a form of social architecture – a place where children create rules, resolve disputes and build entire worlds from whatever their environment offers.

Games, the curators suggest, are “social laboratories in miniature.”

For more than two decades, Francis Alÿs has traveled across cities, villages and conflict zones filming children at play. What began in 1999 evolved into an audiovisual archive spanning more than 50 short films across five continents, 27 of which are included in the Bogotá exhibition.

Children jump across hopscotch grids in Afghanistan, toss bones in India, spin tops in Mexico and invent rhythmic contests in narrow urban streets. One of the featured Colombian works, Trompos de semilla, Arara, Colombia, 2025, was filmed in the Amazon with support from Banco de la República’s Cultural Center in Leticia, capturing children in the Arara community playing with spinning tops made from seeds.

The games are simple, but the implications are not.

On the screen there are adults directing the action, no digital interfaces, no organized sports structures. Instead, children improvise with what is at hand – sticks, stones, crates, seeds, chalk, bottle caps – creating systems of cooperation and competition, rules and rebellion.

That act of invention lies at the center of Alÿs’s fascination.

![Francis Alÿs, Children’s Game #29: La roue [The Wheel], Lubumbashi, Democratic Republic of the Congo, 2021. Courtesy Photo: © Francis Alÿs](https://thecitypaperbogota.com/wp-content/uploads/2026/04/La_roue-2021-STILL-5-1-650x464.jpg)

Born in Belgium in 1959, Alÿs grew up with the image of Children’s Games (1560), the iconic painting by Pieter Bruegel the Elder depicting hundreds of children absorbed in play across a town square. According to the exhibition guide, the work became a lifelong reference point—an early visual map of how play reveals the structure of society itself.

Alÿs studied architecture at the Istituto Universitario di Architettura di Venezia before moving to Mexico in 1986 as part of an aid project to help install aqueducts in Oaxaca. He later settled in Mexico City’s historic center, where he developed the poetic and political language that would define his career.

His practice – spanning video, painting, installation and performance – often addresses borders, migration, urban fragility and the absurd mechanics of social order. Power dynamics, the commercialization of public space and the erosion of civic community remain central artistic preoccupations.

In Juegxs de niñxs those themes emerge quietly but powerfully.

Alÿs is not merely documenting childhood. He is observing how public life functions – and how children, often without adult mediation, rehearse the structures of society through play.

The exhibition reveals how games create temporary communities. They teach negotiation, competition, fairness and exclusion. They reflect both freedom and hierarchy. In some videos, the children play in ordinary neighborhoods filled with laughter and routine. In others, games unfold beside military checkpoints or in areas shaped by poverty, displacement and war.

Play persists, but never outside history.

The multi-screen installation at MAMU emphasizes these contrasts, showing both the universality of childhood and the inequalities that define it. Similar games appear across radically different geographies, suggesting what the curators describe as a kind of underground cosmopolitan culture of childhood – one that challenges the rigid identities of the adult world.

At the same time, the exhibition reflects on disappearance.

Traditional street games, some with roots stretching back to ancient Mesopotamia, are becoming less visible. Urban traffic has overtaken streets once used as playgrounds. Safety concerns have limited unsupervised outdoor play. Screens and digital entertainment increasingly dominate leisure time. Public space itself has become more regulated, commercialized and less available for improvisation.

Alÿs’s work does not romanticize the past, but it does capture transient moments of celebration.

What looks ordinary today – a spinning top, a hopscotch square, a game played with stones – may one day become a contemporary hieroglyph, evidence of how communities once formed themselves in public space.

As curator Cuauhtémoc Medina notes, games are not eternal. Their disappearance may signal something larger about the transformation of humanity itself.

If all the world’s a street, Alÿs has chosen not to place these collaborative works on the market, underscoring their documentary and communal nature. For the multi-medium storyteller, games, like art, are not commodities, but shared records of our collective experience.

This Bogotá presentation marks the exhibition’s fifth international stop following showings in Mexico City, Antwerp, Guadalajara and Santiago de Chile. In 2024, Alÿs also presented the project at the Barbican Art Gallery under the title Ricochets, marking the first time his work was shown in the United Kingdom.

At MAMU, the museum becomes more than a gallery – it becomes a space to reconsider childhood, the city and the fragile public spaces where both are formed.

Museo de Arte Miguel Urrutia. Calle 11 No.4-21.

Admission is Free.

In Colombia’s local fixed-income market, the Títulos de Tesorería (TES) fixed-rate curve appreciated across its entire structure over the last month. As of March, the total balance of TES in circulation stood at 747.9 trillion COP. Despite this positive market valuation, macroeconomic headwinds remain a central concern for the Ministerio de Hacienda y Crédito Público. The fiscal balance of the Gobierno Nacional Central (GNC) reported an accumulated deficit of 1.7% of GDP through February.

These persistent fiscal imbalances were cited as the primary driver behind the recent decision by S&P Global (NYSE: SPGI) to downgrade Colombia’s sovereign credit rating. The administration continues to manage these debt instruments against a backdrop of tight monetary conditions, which remain a primary focus for institutional investors holding Colombian sovereign paper.

Colombian fixed-income markets show valuation gains despite a recent S&P credit downgrade linked to ongoing fiscal imbalances.

The international fixed-income landscape experienced notable shifts between March 25 and April 23, 2026. The yield curve for US Treasury bonds displayed mixed performance, defined by a decrease in short-term rates and an increase in long-term yields. Analysts attribute this volatility primarily to conflicting signals regarding the ongoing conflict in the Middle East.

Economic indicators released by the Bureau of Labor Statistics show that annual consumer inflation, measured by the Consumer Price Index (CPI), accelerated by 0.9 percentage points to reach 3.3% in March. This data triggered a rebound in short-term inflation expectations within the Treasury bond market, while medium and long-term outlooks remained stable. Consequently, the Intercontinental Exchange (NYSE: ICE) MOVE index—which tracks public debt market volatility—and the Cboe (NYSE: CBOE) VIX—which monitors S&P 500 equity volatility—both registered significant declines during the period.

The upcoming monetary policy meeting of the Banco de la República, scheduled for April 30, takes place as the balance of financial risks has shifted significantly compared to the first quarter of 2026. Analysts from Bancolombia (NYSE: CIB) expect the Junta Directiva to increase the benchmark interest rate by 75 basis points, bringing the policy rate to 12.00%.

The convergence of elevated inflation, recent reversal episodes, and misaligned market expectations has reinforced the perceived need for a restrictive monetary stance. This strategy aims to contain domestic demand while preserving the institutional credibility of the central bank. Unlike previous sessions, the current decision-making process is influenced by a shifting global environment where markets have moved toward a higher-for-longer interest rate scenario amid increased uncertainty.

Recent discussions regarding the participation of the Ministro de Hacienda in the Junta Directiva sessions have introduced an additional element of analysis. However, current assessments suggest this does not alter the fundamental policy diagnosis, and no disruptions to the decision-making process are anticipated. Monetary policy is expected to maintain consistency, with the strategic focus shifting from reaching a contractive level to determining the necessary duration of that posture.

Analysts project Banco de la República will raise rates to 12.00% to combat inflation despite slowing domestic economic growth.

The international economic context provides a mixed backdrop for the Colombian decision. Private sector activity in the US appeared to accelerate in April, following a 1.7% monthly increase in retail sales during March. In contrast, the Eurozone reported a contraction in economic activity during April. Energy markets have also seen volatility, with US crude inventories rising in the second week of April while gasoline stocks saw a significant decline. Furthermore, crude prices surged following reports of new security incidents in the Strait of Hormuz.

Domestically, the Departamento Administrativo Nacional de Estadística reported that the Índice de Seguimiento a la Economía grew by 1.6% in February. While imports maintained growth during the same month, the urban unemployment rate across the 13 primary metropolitan areas continued a downward trend through March 2026. In the fixed income market, the central government reported debt levels at 64.2% of GDP for the first quarter, with internal debt accounting for 71.2% of that total.

Market movements reflected these broader trends as the US Treasury curve saw valuation increases driven by investor caution. In the region, Colombia, Brazil, and Uruguay emerged as the primary beneficiaries of the J.P. Morgan (NYSE: JPM) GBI index rebalancing in March. Locally, fixed-rate Títulos de Tesorería experienced devaluations across the entire curve last week. According to the April Encuesta de Opinión Financiera, these devaluations are expected to persist in the coming months. In currency markets, the COP appreciated last week against a backdrop of global and local factors, while the Euro lost ground against the USD.

Headline photo: Bogotá headquarters of Banco de la República (Banrepublica). Photo credit Juan Enrique Rodríguez, courtesy Banrepublica

Aris Mining (TSX: ARIS; NYSE: ARIS) confirmed the completion of an underground infrastructure connection at its Marmato gold mine in Colombia. The development involved connecting a new surface decline to the existing underground mining workings.

This cross-cut connection serves as a technical step for the ongoing expansion project, which includes the construction of a 5,000 tons-per-day carbon-in-pulp (CIP) plant. The company stated that the infrastructure is currently on schedule to support the initiation of gold production in the fourth quarter of 2026.

Neil Woodyer, Chair and CEO of Aris Mining, stated: “The on-schedule connection of the new surface decline to the existing underground development is a major milestone for Marmato and an important step in delivering our expansion plans.”

The Marmato expansion is part of a broader strategy intended to increase the company’s annual gold production. Aris Mining aims to achieve a combined output of approximately 500,000 ounces per year from its Segovia and Marmato operations. The Segovia mine previously expanded its operational capacity following the installation of a second mill in June 2025.

The company maintains a long-term production objective of approximately 1 million ounces of gold annually. This target incorporates potential production from the Toroparu gold project in Guyana, where a prefeasibility study is currently underway. Aris Mining expects a construction decision regarding the Toroparu project in early 2027.

Regarding its portfolio in Colombia, the company is finalizing environmental studies for the Soto Norte gold project. Aris Mining plans to submit these documents for the licensing process during the second quarter of 2026.

Photo (© Loren Moss) illustrative only (Not marmato mine)

Vancouver-based Aris Mining Corporation (TSX: ARIS; NYSE: ARIS) reported preliminary first-quarter 2026 gold production of 74,300 ounces from its two underground mines in Colombia, representing a 6% increase over the fourth quarter of 2025 and a 36% increase compared to the same period a year earlier.

The company said it sold 74,800 ounces of gold during the quarter at an average realized price exceeding $4,860 USD per ounce, generating gold revenue of more than $360 million USD. That figure marks a 20% increase from Q4 2025 revenue of $301 million USD and more than double the $154 million USD reported in Q1 2025. The company reported a cash balance exceeding $470 million USD as of March 31, 2026, an increase of approximately $80 million USD from the end of the previous quarter.

“We expect Q1 2026 gold revenue to exceed $360 million, a significant increase from $154 million in Q1 2025 and $301 million in Q4 2025, driven by higher gold prices and increased ounces sold.” — Neil Woodyer, Chair and CEO, Aris Mining Corporation

The production gains were concentrated at Aris Mining’s Segovia operation in the department of Antioquia, which produced 66,600 ounces during the quarter, up from 63,100 ounces in Q4 2025 and 47,500 ounces in Q1 2025. The year-over-year increase of 40% at Segovia was driven primarily by a notable improvement in ore grade. The average gold grade processed rose to 12.41 grams per ton from 9.37 grams per ton a year earlier, a 32% increase, while the volume of ore processed increased 5% to 175,000 tons. Recovery rates held at 95.3%, compared to 96.1% in both the prior quarter and Q1 2025.

The higher grades offset a decline in throughput compared to Q4 2025, when the mine processed 201,000 tons at an average grade of 10.10 grams per ton. Aris Mining completed installation of a second mill at Segovia in June 2025, increasing processing capacity by 50% to 3,000 tons per day, and the company has indicated that the ramp-up at the operation is continuing.

At the Marmato mine in the department of Caldas, production totaled 7,800 ounces in Q1 2026, an increase from 6,700 ounces in Q4 2025 and 7,200 ounces in Q1 2025. Marmato processed 77,000 tons of ore at an average grade of 3.53 grams per ton during the quarter, compared to 75,000 tons at 3.12 grams per ton in Q4 2025. Recovery rates at Marmato declined slightly to 89.6% from 90.8% in the prior quarter.

| Gold production and sales | Q1 2026 | Q4 2025 | Q1 2025 |

|---|---|---|---|

| Segovia (koz) | 66.6 | 63.1 | 47.5 |

| Marmato (koz) | 7.8 | 6.7 | 7.2 |

| Total production (koz) | 74.3 | 69.9 | 54.8 |

| Total sales (koz) | 74.8 | 71.7 | 54.3 |

Neil Woodyer, the company’s chair and CEO, said production growth in 2026 is expected to be weighted toward the second half of the year. The company is building a new bulk mine and carbon-in-pulp (CIP) processing plant at Marmato, with first gold expected in Q4 2026. At steady state, the expanded Marmato operation is expected to produce approximately 200,000 ounces per year.

Together, the Segovia and Marmato expansions are expected to increase Aris Mining’s annual gold production to approximately 500,000 ounces. The two mines produced a combined 257,000 ounces in 2025.

Beyond its operating mines, Aris Mining is advancing the Soto Norte gold project in the department of Santander, Colombia, where environmental studies are being finalized for submission in Q2 2026 to initiate the licensing process. The company also holds the Toroparu gold project in Guyana, where a prefeasibility study is underway and a construction decision is expected in early 2027. These projects form part of Aris Mining’s longer-term objective of reaching approximately 1 million ounces of annual gold production, though that target includes estimates from a preliminary economic assessment for Toroparu that the company has cautioned are based on inferred mineral resources and are speculative in nature.

The company expects to report full Q1 2026 financial and operating results on or about May 6, 2026. The quarterly results contained in the April 7 announcement are preliminary and may differ from final figures.

Aris Mining is listed on the Toronto Stock Exchange and the New York Stock Exchange under the ticker symbol ARIS. Company filings are available through SEDAR+ and the US Securities and Exchange Commission.

Economic activity in Colombia expanded at an estimated annual rate of 2.1% during the first quarter of 2026. According to the latest NowCast report issued by the Grupo Cibest, unit of Bancolombia (NYSE: CIB, BVC: BCOLOMBIA), this outcome reflects a loss of momentum compared to the rolling quarter ended in February. That previous period recorded a growth of 2.2%, which was revised downward by 10 basis points from an initial estimate of 2.3%.

The 2.1% growth rate for the quarter indicates a slowdown relative to both the market consensus average of 2.7% and the internal growth forecast of 3.3% held by the bank. On a month-over-month basis, the seasonally adjusted series of the NowCast index posted a 1.3% contraction in March 2026. When compared to March 2025, economic activity grew by 2% year over year, representing a 50-basis-point decline from the 2.5% reading recorded the previous month.

“Overall, these results suggest that the economy is beginning to lose steam, amid multiple sources of uncertainty.” — NowCast Bancolombia Report

Analysis at the sector level reveals a broadly weaker growth profile, with deceleration appearing across most productive areas. Slower momentum was identified in trade, manufacturing, recreation, real estate, and financial services. Manufacturing expansion cooled to 1.0% in March 2026, while financial services recorded marginal growth of 0.6%. The real estate sector maintained a steady growth rate of 1.9%.

Construction and communications were the only sectors to record negative growth during the period. The construction sector saw a significant downturn, contracting by 2.3% in March 2026 after having posted 1.4% growth in February. The information and communications sector contracted by 0.4%, marking its fourth consecutive month in contractionary territory. Conversely, acceleration was noted in public administration, which grew by 5.1%, agriculture at 3.7%, and mining at 0.8%.

The NowCast family of indicators is prepared by Grupo Cibest through the processing and aggregation of transaction data from the bank’s various payment channels. Using advanced quantitative tools, the index provides high-frequency estimates of Colombian productive activity to complement official data from the Departamento Administrativo Nacional de Estadística. The report was authored by Arturo Yesid González Peña, Head of Quantitative and Analytics, and Sebastián Ospina Cuartas, Data Controller.

The report also incorporates data from the Bloomberg platform and FocusEconomics Consensus Forecasts to provide broader economic context. While the national economy remains in expansionary territory, the analysts suggest that the current results indicate the market is losing steam due to various sources of domestic uncertainty.

On April 8, 2026, S&P Global Ratings (NYSE: SPGI) lowered its long-term foreign currency sovereign credit rating on Colombia to BB- from BB and its long-term local currency rating to BB from BB+. The outlook for both ratings is stable, reflecting expectations that the Government of Colombia will gradually reduce its fiscal deficit while sustaining moderate growth in the national gross domestic product.

The rating action follows persistent fiscal imbalances and a policy environment that has become less predictable since the pandemic-related recession. The government decision to suspend the national fiscal rule in 2025 marked a significant shift in the policy framework. Pro-cyclical fiscal policies have provided marginal support for employment and consumption, but have also contributed to higher inflation expectations and a wider current account deficit. S&P expects the general government fiscal deficit to reach 5.6% of the national gross domestic product in 2026, compared to 5.3% in 2025.

“We expect Colombia to have consistently large fiscal deficits over the next few years.” — S&P Global Ratings

Institutional stability remains a key factor in the rating, though challenges persist. A fragmented legislature followed the March 2026 elections, where Pacto Histórico and Centro Democrático emerged with the largest minorities. The upcoming presidential election, scheduled for May 31, 2026, adds further uncertainty. Candidates such as Iván Cepeda of Pacto Histórico, Paloma Valencia, and Abelardo de la Espriella have proposed varying approaches to fiscal consolidation. The new administration will inherit spending pressures related to domestic security, rising healthcare costs, and pension payments linked to minimum wage increases.

The Banco de la República, the independent central bank of the country, has maintained a tight monetary policy to combat inflationary pressures. Annual inflation reached 5.3% in February 2026, prompting the bank to increase reference rates to 11.25%. S&P anticipates that inflation will not return to the target range of 3% +/- 1% until early 2029. While the independent status of the central bank provides a buffer against external shocks, high interest rates and lower-than-expected revenue collections have contributed to the widening deficit since 2024.

Economic growth is projected at 2.5% for 2026, slightly below the 2.6% recorded in 2025. Per capita growth is estimated at $9,900 USD for 2026, with real growth expected to average just above 2% through 2029. Despite being a net energy exporter, the performance of the US economy and international energy prices continue to influence national outcomes. Hydrocarbon exports declined to 35% of goods exports in 2025, down from 67% in 2013, showing some diversification even as the sector remains a primary source of volatility.

Net general government debt is forecast to approach 66% of the national gross domestic product by 2029, rising from 60.4% in 2025. S&P notes that the government interest burden will average 12.3% of general government revenue over the next three years. The shift toward issuing shorter-term debt instruments has reduced reported interest payments but increased vulnerability to interest rate fluctuations. External indicators remain a concern, with narrow net external debt expected to stabilize at 130% of current account receipts through 2029. Foreign direct investment is expected to be the primary source for funding the current account deficit, which is projected to stabilize around 2.6% of the national gross domestic product.

Vise photo credit © Loren Moss

President Gustavo Petro has triggered a rare institutional confrontation with the Central Bank after he ordered to “break relations” following an modest interest rate increase, raising concerns over economic policy independence just two months before the May 31 presidential election.

The board of Banco de la República voted on March 31 to raise its benchmark rate by 100 basis points to 11.25 per cent, defying government pressure for looser policy. Finance minister Germán Ávila denounced the move as “disproportionate” and withdrew from the board, accusing policymakers of privileging financial sector interests over economic growth.

The decision marks an unprecedented rupture in Colombia’s macroeconomic governance framework. By stepping away from the board, Ávila has effectively deprived it of the quorum required to meet under existing statutes, raising the prospect of a policy deadlock just as inflation remains above target.

At stake is more than a disagreement over rates. The confrontation exposes deeper tensions between a government focused on growth and redistribution and a technocratic central bank committed to price stability. It also risks undermining one of Colombia’s most respected institutions at a time of heightened global uncertainty.

Governor Leonardo Villar defended the rate hike, insisting the bank’s constitutional mandate to control inflation could not be subordinated to political considerations. He said the board remained focused on steering inflation back to its 3 per cent target, noting that price pressures — currently running at 5.29 per cent annually — remain elevated despite signs of moderation.

“The decisions are based on technical criteria,” Villar said, rejecting accusations of bias towards the financial sector. He also warned that the government’s withdrawal runs counter to institutional norms.

Markets are now watching whether the government intends to sustain its boycott. Under Colombian law, the presence of a Finance Minister is required for board meetings, meaning continued absence could paralyse rate-setting decisions in the coming months. Three key meetings — in April, June and July — are scheduled before the end of Petro’s term, with the latter two falling after a decisive first-round of the presidential elections.

Business leaders have reacted with alarm. Camilo Sánchez, head of utilities association Andesco, described the breakdown in coordination as “dire”, warning that permanent dialogue between fiscal and monetary authorities is essential for economic stability.

Analysts say the government may be using institutional leverage to halt further rate increases, given that a majority of board members had signalled a tightening bias to anchor inflation expectations. A prolonged standoff could, however, carry significant costs.

Colombia has long been viewed by investors as a regional outlier for its strong central bank independence. Any perception that political pressure is eroding that autonomy could weigh on the peso, increase borrowing costs and deter foreign investment.

The dispute comes against a complex macroeconomic backdrop. Inflation has been fuelled in part by a sharp increase in the minimum wage and higher public spending, while external risks — including rising energy prices linked to the war in the Middle East and closure of the Strait of Hormuz by Iran.

For Petro, the rate hike reinforces a long-standing critique that tight monetary policy is stifling growth and employment. Writing on social media, the president accused the central bank of pursuing a “suicidal” policy that harms the wider economy.

Yet economists warn that weakening institutional credibility could ultimately prove more damaging than high interest rates. “The risk is not just policy error,” one Bogotá-based analyst said. “It is the erosion of the rules of the game.”

The coming weeks will test whether the standoff is a negotiating tactic or the start of a more fundamental shift in Colombia’s economic governance. Either way, the episode has already injected a new layer of uncertainty into one of Latin America’s most closely watched economies.

The Colombian peso (COP) experienced a 2.1% appreciation during March 2026, driven by a recovery in global oil prices and key domestic developments. According to the latest analysis from Bancolombia (BVC: BCOLOMBIA / NYSE: CIB), the performance of the currency coincided with the results of national legislative elections and recent monetary policy adjustments by the Banco de la República.

Global energy markets recorded a significant increase in crude prices throughout the month. Brent crude rose 63% to end March at $118 USD per barrel, while West Texas Intermediate (WTI) increased 51% to close at $101 USD per barrel. These price movements have been largely attributed to geopolitical tensions in the Middle East, which continue to influence international commodity flows and investor sentiment.

On the domestic front, the Gran Coalición por Colombia primary election recorded a turnout of more than 5 million voters. Market analysts indicated that the high participation rate was viewed as a positive indicator of institutional stability. Simultaneously, the Board of Directors of the Banco de la República increased the national policy interest rate by 100 basis points, bringing the benchmark rate to 11.25%. This decision aligns with regional efforts to manage inflationary pressures through tighter monetary control.

International market conditions also reflect a shift in expectations regarding the Federal Reserve. Due to ongoing conflict in the Middle East and persistent economic indicators, markets currently anticipate that the US central bank will maintain existing interest rates without cuts for the remainder of the year.

Looking forward to April, the research team at Bancolombia—led by Chief Economist Laura Clavijo, Macroeconomic Manager Jose Luis Mojica, and International and FX Analyst Maria Paula Gonzalez—projects that the exchange rate will trade within a range of $3,625 COP to $3,725 COP. This forecast accounts for continued volatility and heightened uncertainty in both global and domestic financial markets.

Bancolombia (photo © Loren Moss)

Ecopetrol S.A. (BVC: ECOPETROL; NYSE: EC) has entered into a formal payment agreement with the Government of Colombia to settle outstanding balances from the Fuel Price Stabilization Fund, known in Spanish as the Fondo de Estabilización de Precios de los Combustibles (FEPC). The agreement, reached through the Ministerio de Hacienda y Crédito Público and the Ministerio de Minas y Energía, addresses $1.6 trillion COP owed for the first quarter of 2025.

Under the terms of Resolutions 00368 and 00369 issued by the Dirección de Hidrocarburos, the total amount is divided between Ecopetrol S.A., which is owed $1.2 trillion COP, and Refinería de Cartagena S.A.S. (Reficar), which is owed $0.4 trillion COP. The repayment schedule began with a cash transfer of $2.89 billion COP on April 1, 2026. The remaining balance of approximately $1.55 trillion COP is scheduled to be paid on December 15, 2026, through the issuance of Treasury Securities, or Títulos de Tesorería (TES). The Colombian state has acknowledged the financial costs associated with the time elapsed until the final December payment.

“The Ecopetrol Group continues to work in close coordination with the Ministries of Finance and Public Credit and of Mines and Energy — the authorities responsible for fuel pricing policy — in the implementation of payment mechanisms and the reduction of FEPC balances.” — Ecopetrol S.A.

Concurrent with the subsidy settlement, Ecopetrol received authorization from the Ministerio de Hacienda y Crédito Público via Resolution 0666 to execute an external public debt management transaction totaling $1.25 billion USD. The five-year loan was secured through a consortium of international lenders including BBVA (BME: BBVA; NYSE: BBVA), Bank of America (NYSE: BAC), JP Morgan Chase (NYSE: JPM), and Bank of China (HKG: 3988). The credit facility carries a floating interest rate indexed to the Secured Overnight Financing Rate (SOFR) and will be repaid in four equal installments.

The proceeds from the $1.25 billion USD loan are designated for the repayment of existing obligations. Specifically, $1.2 billion USD will be used to settle a 2024 loan previously authorized for the acquisition of the state’s interest in Interconexión Eléctrica S.A. E.S.P. (ISA), while the remaining $50 million USD will be applied to an outstanding balance from a 2025 credit agreement. The loan agreement is governed by the laws of the State of New York and includes standard covenants regarding the borrower’s payment capacity and financial integrity.

These financial maneuvers are intended to optimize the maturity profile of the Ecopetrol Group, which remains responsible for over 60% of hydrocarbon production in Colombia. The company continues to operate integrated systems in transportation, refining, and petrochemicals, with additional international operations in the US Permian basin, the Gulf of Mexico, Brazil, and Mexico.

The resignation of Wilmar Mejía as chief of Colombia’s National Intelligence Agency has highlighted instability within the country’s main intelligence agency under the government of President Gustavo Petro, which has seen four leadership changes over the past three years.

Mejía confirmed his departure on April 1 in an interview with Canal 1. “When the Inspector General’s Office lifted my suspension, I went to sign my reinstatement document and within 15 minutes I submitted my resignation. I am no longer the director of intelligence,” he said.

The official had been suspended since December 23, 2025, by the Inspector General’s Office as part of a disciplinary investigation “for alleged links to and the provision of information to members of dissident factions of the former Revolutionary Armed Forces of Colombia (FARC).” The Inspector Office said at the time that the measure aimed to prevent possible interference with the process.

The case is related to the seizure of digital files belonging to Alexander Díaz Mendoza, known as “Calarcá Córdoba,” a leader of one of the dissident structures grouped under the Estado Mayor de Bloques y Frente (EMBF). Authorities say the documents point to possible contacts with the former intelligence chief.

Mejía has denied any involvement and has argued that the accusations are part of alleged “setups aimed at silencing reports of internal corruption.”

According to the Inspector Office, the investigation “includes possible acts such as the disclosure of military force communication frequency codes and support in the creation of security companies that could facilitate the legalization of weapons in the event of a breakdown in peace talks with the government.”

So far, neither the Inspector General’s Office nor the Attorney General’s Office has concluded its investigations, and no determination of responsibility has been made.

The case has raised concerns about state security and the institutional stability of the agency, considered a key body for the country’s strategic intelligence.

Local media outlets such as El Colombiano have reported that the situation has affected trust among international intelligence partners, suggesting that agencies such as the CIA (United States), MI6 (United Kingdom), and Mossad (Israel) have restricted the sharing of strategic information with Colombia.

Since Petro took office, the agency has had four directors, all of them close to the president through their past involvement in the M-19 guerrilla group, which signed a peace agreement in 1990.

The instability dates back to the beginning of Petro’s administration. Since August 2022, when Manuel Alberto Casanova Guzmán was appointed, the agency has undergone repeated leadership changes.

Casanova, who faced criticism over his lack of intelligence experience and background as a philosopher, was removed following allegations of involvement in a false extortion case linked to then-Foreign Minister Álvaro Leyva, as reported by Infobae.

He was succeeded by Carlos Ramón González, who later left the post amid investigations into his alleged role in the corruption scandal involving Unidad Nacional de Gestión de Riesgo y Desastres (UNGRD). He is currently in Nicaragua under political asylum, while Colombia has requested his extradition and Interpol has issued a red notice.

Finally, just before Mejía, the agency was led by Jorge Lemus, who served for nearly a year before resigning. He was subsequently appointed by Petro as director of the Unidad de Información y Análisis Financiero (UIAF), amid growing allegations of possible infiltration within the country’s security institutions.

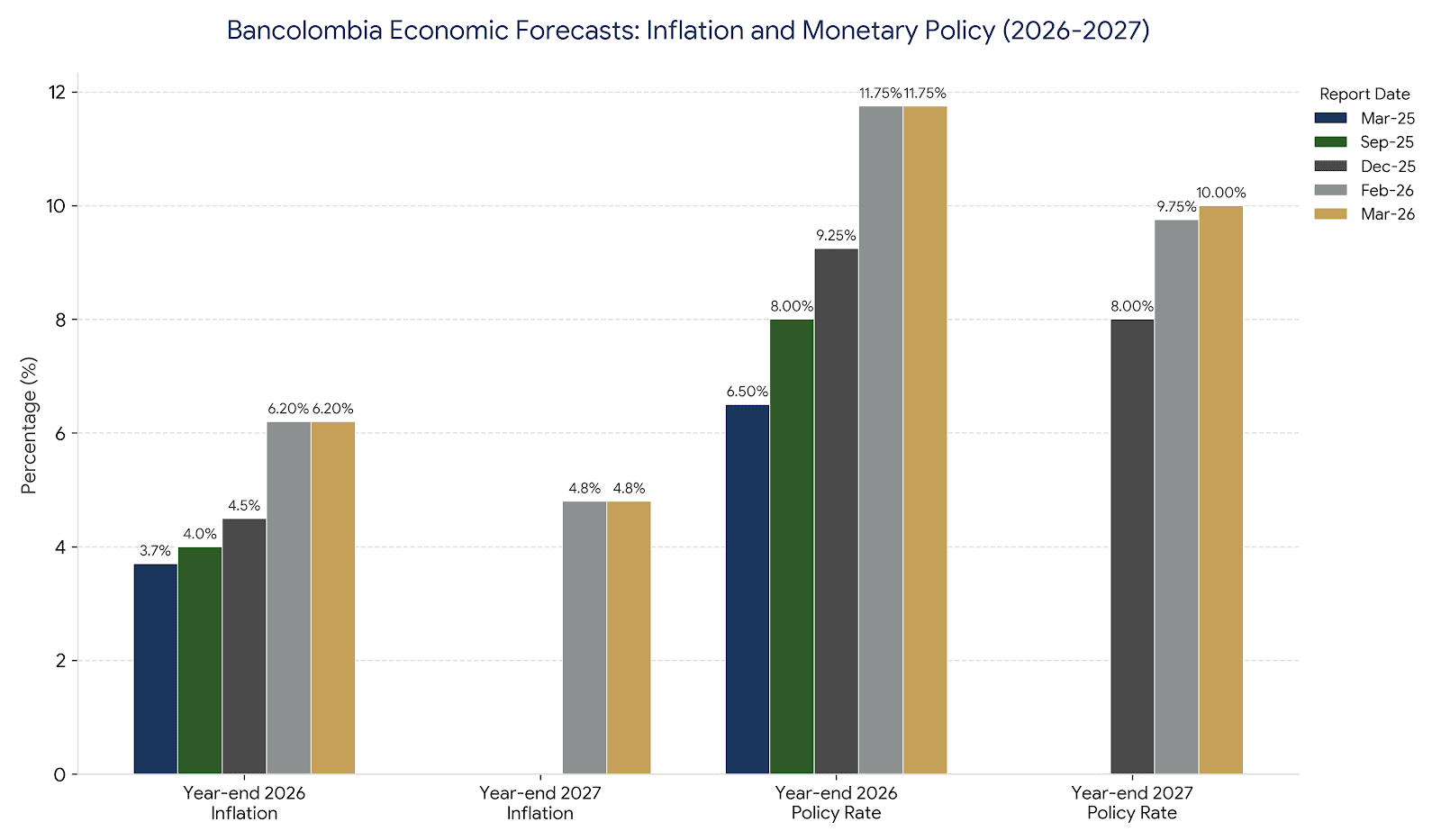

Colombia’s Banco de la República is preparing for a significant shift in monetary policy as inflationary risks deteriorate. According to the latest report from the Dirección de Investigaciones Económicas, Sectoriales y de Mercados at Bancolombia (NYSE: CIB), persistent internal pressures and a less favorable external environment are driving the need for a more restrictive stance.

Bancolombia’s analysts expect the Junta Directiva of the Banco de la República to increase its policy interest rate by 100 basis points, bringing it to 11.25 percent. This forecast suggests that the first half of 2026 will be characterized by a more aggressive tightening cycle than previously anticipated, with the rate potentially reaching 12.75 percent.

The international landscape is playing an increasingly decisive role in these local policy configurations. A recent week of central bank decisions globally revealed a shift in tone among major financial institutions, primarily due to rising uncertainty stemming from the conflict in Iran. This geopolitical tension has directly impacted costs for energy, transportation, and agricultural inputs.

“The increase responds to the need to send a clear signal of commitment to price stability.” — Dirección de Investigaciones Económicas, Sectoriales y de Mercados at Bancolombia.

In the US, economic activity shows signs of moderation, yet producer price inflation in February exceeded expectations. The yield curve for US Treasuries, managed by the US Department of the Treasury, has shown mixed behavior as the conflict escalates, with the spread between 10-year and 3-month bonds reaching levels not seen since 2023. Inflation expectations in the US have rebounded in the short term, though they remain anchored over longer horizons.

| Forecast Category | Mar-25 | Sep-25 | Dec-25 | Feb-26 | Mar-26 |

| Year-end 2026 Inflation | 3.7% | 4.0% | 4.5% | 6.2% | 6.2% |

| Year-end 2027 Inflation | — | — | — | 4.8% | 4.8% |

| Year-end 2026 Policy Rate | 6.50% | 8.00% | 9.25% | 11.75% | 11.75% |

| Year-end 2027 Policy Rate | — | — | 8.00% | 9.75% | 10.00% |

Domestically, the business indices from think-tank Fedesarrollo showed mixed results for February. However, there are positive indicators in the labor market, as the urban unemployment rate across the 13 primary metropolitan areas continued its downward trend. Additionally, goods exports recorded an advance during the same period.

In the local fixed-income market, the TES fixed-rate curve saw a recovery last week. However, the March Financial Institutions Survey suggests that devaluations of TES may persist in the short term. Long-term TES Class B placements in the first quarter reached 1.0 percent of the GDP.

Chart based on data from Grupo Cibest & the Banco de la República.

Energy markets remain volatile as crude oil inventories in the US increased beyond expectations in the third week of March. Despite this, the price of Brent crude rose toward the end of the week, driven by skepticism regarding a potential ceasefire in the Middle East. The Colombian peso appreciated over the past week, tracking the intensity of the regional conflict.

The equity market results for the fourth quarter of 2025 remained neutral and aligned with market expectations. Global volatility continues to be shaped by energy shocks, geopolitical strife, and a cautious approach toward investments in artificial intelligence.

The projected rate hike by the Banco de la República is intended to send a definitive signal of commitment to price stability. This adjustment reflects not only recent inflation trends but also a strategic effort to prevent the further deterioration of expectations in a high-risk environment.

Headline image: Bogotá headquarters of Banco de la República (Banrepublica). Photo credit Juan Enrique Rodríguez, courtesy Banrepublica

Wingo, a subsidiary of Copa Holdings (NYSE: CPA), has announced the launch of two new direct international routes from Medellín to Guatemala City, Guatemala, and Montego Bay, Jamaica. With this expansion, the carrier becomes the only airline to operate these specific nonstop segments from José María Córdova International Airport in Rionegro, which serves the Antioquia region.

The new service increases Wingo’s international portfolio to 10 destinations from the city, complementing its existing network of five domestic routes. According to data provided by the airline, Medellín has become a primary operational base in Colombia. In 2025, approximately 35% of the carrier’s total passenger traffic, representing 1.2 million travelers, originated from or arrived in the city.

“Medellín is a strategic city for Wingo, and these two new routes reflect our confidence in the potential of the city and the response of travelers.” — Jorge Jiménez, Commercial and Planning Vice President of Wingo.

The Alcaldía de Medellín, through the Secretaría de Turismo y Entretenimiento and the Bureau de Medellín y Antioquia, coordinated with airport concessionaire Airplan to facilitate the new frequencies. The Medellín to Guatemala City route is scheduled to begin operations on June 25, 2026, with three weekly frequencies on Tuesdays, Thursdays, and Saturdays. The airline expects to offer 30,000 seats annually on this route, with one-way fares starting at $108 USD, including taxes and fees.

The connection to Montego Bay is slated for a June 23, 2026, start date, also operating three times per week on Tuesdays, Thursdays, and Saturdays. Introductory fares for the Jamaican destination are positioned at $159 USD per trayect. This move follows a 2025 pilot program where Jamaica was marketed as a high-interest destination for Colombian travelers.

Jorge Jiménez, Commercial and Planning Vice President at Wingo, stated that these routes reflect confidence in the potential of the city and the response of travelers to direct, low-cost international options. Ana María López Acosta, Secretary of Tourism and Entertainment, noted that the collaboration between the public and private sectors continues to project the city as an attractive destination for tourism and investment.

The expansion comes as the Aeropuerto Internacional José María Córdova continues to increase its capacity as a logistical platform for the country. Javier Benítez, Manager of the airport, indicated that the arrival of these routes reaffirms the facility’s potential to facilitate international business and connection for the region.

The Ministerio de Comercio, Industria y Turismo (Ministry of Trade, Industry, and Tourism) hosted the first Foro de Reencuentro Económico CELAC–África at the Ágora Convention Center in Bogotá on March 20, 2026. The event, held as part of a broader high-level forum, aimed to strengthen commercial and investment ties between Colombia and the African continent. During the proceedings, officials identified various sectors for potential growth, including jewelry, agricultural machinery, construction materials, software, digital marketing, and food and beverages.

Minister of Trade Diana Marcela Morales Rojas stated that the forum represents a strategic shift toward trade equity and shared economic opportunities. Over the past four years, the Colombian government has sought to diversify its market reach through economic diplomacy, trade missions, and the establishment of new logistical routes to Africa. Data from 2025 indicates that these efforts have resulted in a significant increase in non-mining and non-energy exports to the continent.

“We aim for this forum to mark the beginning of a new stage: one of strategic cooperation, trade with equity, and the construction of shared opportunities.” — Diana Marcela Morales Rojas, Minister of Trade, Industry, and Tourism.

According to ministry figures, non-mining exports to Africa reached $296.5 million USD in 2025, representing a 112% increase compared to 2024. In terms of volume, these shipments totaled 209,273 tons, a 226.8% rise over the previous year. These goods accounted for 46.6% of Colombia’s total exports to the continent, signaling a shift toward a more diversified export basket. Key products driving this growth include coffee, bananas, machinery, paper, and apparel.

The number of Colombian firms participating in this trade has also expanded. In 2025, 165 companies exported non-mining goods to Africa with values exceeding $10,000 USD, up from 145 companies in 2024. This 15.2% growth in participating firms underscores a transition toward higher value-added exports. Vice President Francia Márquez Mina noted that the economies of Latin America and Africa are complementary, offering potential for the development of new value chains and the utilization of strategic mineral reserves necessary for the global energy transition.

A central component of the forum was a business matchmaking event held on March 17 and 18. Preliminary results from the session show expected trade operations totaling $16 million USD. Nicolás Mejía, Vice President of Exports at ProColombia, characterized the results as a validation of the current market diversification plan. Since the beginning of the current administration, the government has implemented the Estrategia África 2022–2026 to strengthen socioeconomic relations with the region.

Through commercial intelligence analysis, the Colombian government has prioritized nine specific markets for its diplomatic and economic deployment: South Africa, Angola, Mozambique, Nigeria, Ghana, Senegal, Egypt, Tunisia, and Algeria. These nations serve as the primary focus for the continued implementation of the 2022–2026 strategy.

Above photo: MinCIT/Ricardo Báez.

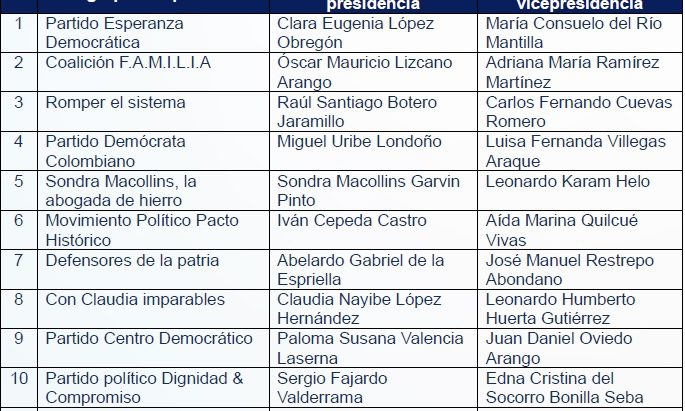

The Registraduría Nacional del Estado Civil of Colombia (RNEC), the entity responsible for organizing elections in the country, reported that a total of 14 candidates have officially registered to run in the country’s presidential elections, scheduled for May 31, 2026. In this vote, citizens will elect the President and Vice President of the Republic for the 2026–2030 term.

According to the electoral authority, the candidates represent a wide range of political perspectives, from left to right, including independent candidacies running through political movements. Here the list and brief profile of the candidates:

The RNEC also reported that “the draw to determine the position of presidential candidates on the ballot will take place on March 25 at the Ágora Bogotá Convention Center.”

This process marks the formal start of the final phase of the presidential campaign, during which candidates will seek to consolidate support ahead of the first round on May 31. If no candidate secures an absolute majority, a runoff between the two leading candidates will be held on June 21.

List of registered candidates for Colombia’s presidency. Photo courtesy of the Registraduría Nacional del Estado Civil.

Headline photo: Polling station in Colombia during last Congress elections in March 8, 2026. Photo courtesy of the Registraduría Nacional del Estado Civil.

Dominican airline Arajet has launched a “Hot Sale Colombia” promotion, offering discounted base fares for international travel originating from major Colombian hubs. The campaign targets passengers departing from El Dorado International Airport in Bogotá, José María Córdova International Airport in Medellín, and Rafael Núñez International Airport in Cartagena.

The promotional window is scheduled to run from March 16 through March 22, 2026. During this period, the airline is offering base fares starting at $1 USD. These rates apply to international routes within the carrier’s network and are available across all four of the airline’s service tiers: Basic, Classic, Comfort, and Extra.

According to the carrier, the travel window for tickets purchased under this promotion extends from April 15, 2026, to September 30, 2026. The availability of these fares is subject to seat capacity on specific flights. The initiative follows the carrier’s broader strategy to increase its market share in the Colombian aviation sector, which is regulated by the Unidad Administrativa Especial de Aeronáutica Civil (Aerocivil) under the Ministerio de Transporte.

Arajet commenced operations in September 2022 and currently maintains its primary hubs at Las Américas International Airport in Santo Domingo and Punta Cana International Airport. The airline utilizes an all-Boeing fleet, consisting of 14 Boeing 737 MAX aircraft (NYSE: BA). The carrier’s network connects the Dominican Republic with various destinations across North America, Central America, South America, and the Caribbean. In 2023, the airline was recognized as the “Best New Airline in the World” at the CAPA Aviation Trust Summit. The airline’s operations are overseen by the Instituto Dominicano de Aviación Civil (IDAC) in its home jurisdiction. Detailed pricing and baggage policies for the current promotion are available through the company’s digital booking platform.

Frontera Energy Corporation (TSX: FEC) has entered into a definitive arrangement agreement to divest its Colombian upstream exploration and production (E&P) portfolio to Parex Resources Inc. (TSX: PXT) for a total firm value of approximately $750 million USD. The transaction follows the termination of a previous agreement with GeoPark Limited (NYSE: GPRK). Frontera opted for the Parex proposal after the Calgary-based independent producer offered $525 million USD in equity consideration, a $125 million USD increase over the prior GeoPark bid. As part of the transition, Frontera has paid a $25 million USD breakup fee to GeoPark.

The $525 million USD equity consideration includes an immediate $500 million USD cash payment upon closing and a $25 million USD contingent payment. The latter is dependent on the execution of a contractual amendment or binding agreement to extend the term of the Quifa Association Contract within 12 months.

Beyond the cash equity, Parex will assume $390 million USD in existing Frontera liabilities. This includes $310 million USD in 2028 Senior Unsecured Notes and an $80 million USD prepayment facility with Chevron Products Company, a subsidiary of Chevron Corporation (NYSE: CVX).

Following the close of the deal, Frontera intends to distribute approximately $470 million USD to its shareholders, which equates to roughly $9.18 CAD per share based on current exchange rates and outstanding share counts. This distribution is subject to shareholder approval and the successful completion of the transaction.

Frontera is retaining its exploration interests in Guyana.

Upon completion, Frontera will pivot its corporate strategy to focus exclusively on energy infrastructure. Its remaining portfolio will be anchored by two primary Colombian assets:

The company will also retain its exploration interests in Guyana. Frontera’s infrastructure division generated approximately $77 million USD in distributable cash flow in 2025. Post-transaction, Frontera expects to maintain $50 million USD in cash reserves to fund growth projects, including a potential Liquefied Natural Gas (LNG) regasification project in partnership with Ecopetrol S.A. (NYSE: EC; BVC: ECOPETROL).

Orlando Cabrales, CEO of Frontera, noted that Parex is currently the largest independent operator in Colombia and a pre-existing partner in the VIM-1 block, which suggests operational continuity for the assets and employees involved.

The independent members of Frontera’s Board of Directors have unanimously recommended the deal. Major shareholders The Catalyst Capital Group Inc. and Gramercy Funds Management LLC, who collectively hold approximately 53% of Frontera’s outstanding shares, have signed support agreements to vote in favor of the arrangement.

The transaction is structured as a plan of arrangement under the Business Corporations Act of British Columbia. It requires the approval of at least two-thirds of the votes cast by Frontera shareholders at a forthcoming special meeting.

The deal is also subject to approval by the Supreme Court of British Columbia and relevant regulatory bodies in both Canada and Colombia. Parex will fund the acquisition through existing cash, credit facilities, and an underwritten financing commitment from Scotiabank (TSX: BNS; NYSE: BNS). Closing is anticipated in the second quarter of 2026.

Citi (NYSE: C) served as the financial advisor to Frontera, while BMO Nesbitt Burns Inc. provided a fairness opinion. Legal counsel was provided by Blake, Cassels & Graydon LLP and McMillan LLP.

Above photo: Frontera Energy’s Quifa field Meta Colombia. Photo credit: Frontera Energy.