Colombia Presidential Election Heads to a Runoff

1 June 2026 at 23:35

The candidate, Abelardo de la Espriella, will face a senator from the left-wing party of the departing president, Gustavo Petro, in a June runoff.

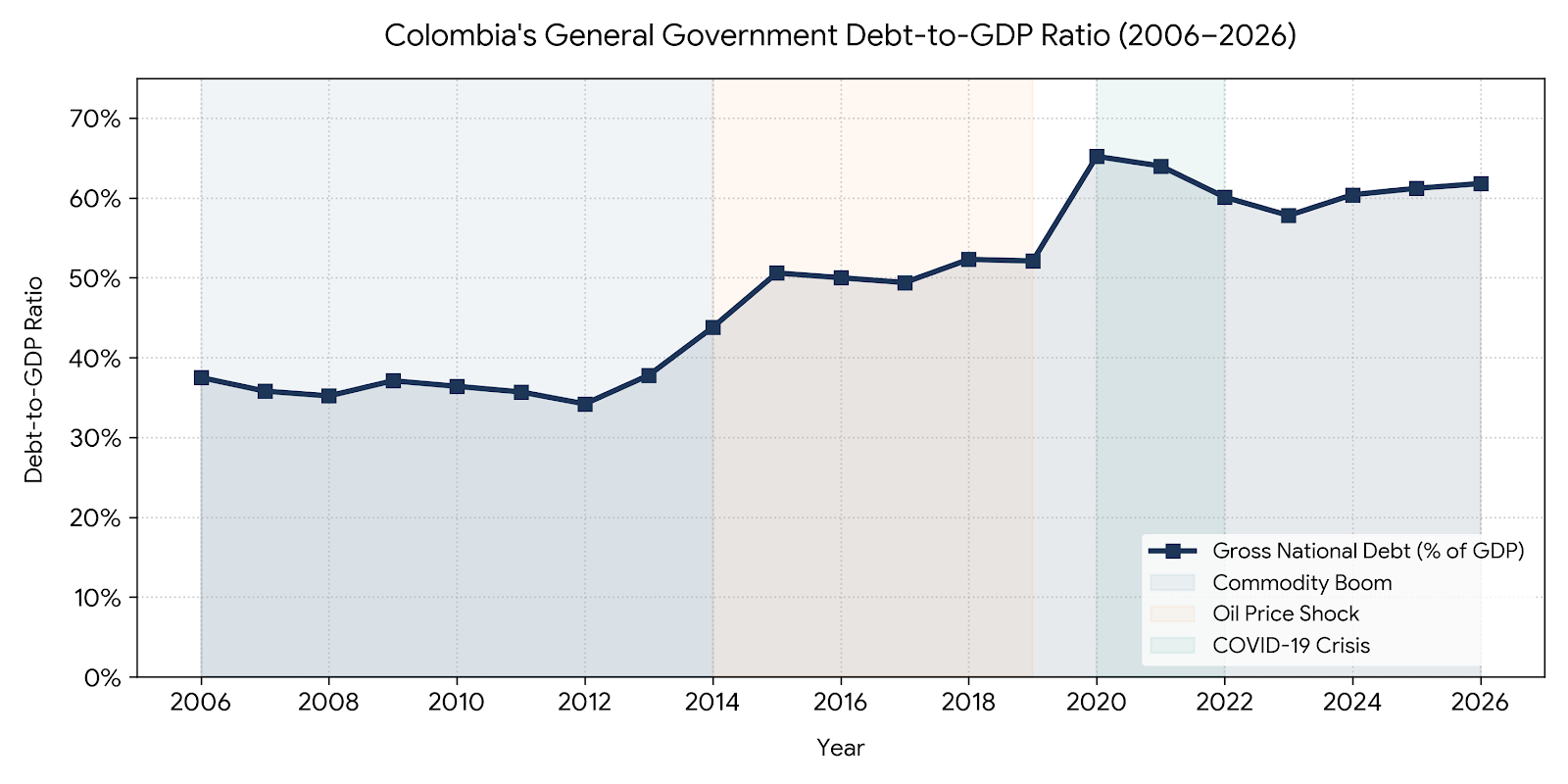

Two decades of fiscal data show that Colombia’s gross general government debt has moved through four distinct macroeconomic phases, ending the current cycle at a level that is materially higher than its pre-pandemic baseline. Persistent annual fiscal deficits, currency volatility, an emergency spending shock and weaker-than-projected tax revenues have combined to push the ratio of public debt to gross domestic product from the mid-30s percent range in the mid-2000s to a band of roughly 60 to 62 percent at the start of 2026, according to figures published by the Ministerio de Hacienda y Crédito Público and the Banco de la República.

The shift carries direct implications for sovereign bondholders, multinationals operating in Colombia and any investor pricing country risk in the Andean region. All three major rating agencies — S&P Global Ratings, Moody’s Ratings and Fitch Ratings — now place Colombia in speculative-grade, or junk, territory, with consecutive downgrades through 2025 and into early 2026.

“The activation of the escape clause confirms that the deterioration observed in 2024 will not be corrected in 2025.” — Renzo Merino, sovereign analyst, Moody’s Ratings

During the global commodity supercycle, Colombia benefited from sustained gross domestic product growth and steady government revenue. Hydrocarbon and mining receipts — channeled through Ecopetrol (NYSE: EC; BVC: ECOPETROL) and the broader extractive sector — supplied a substantial share of national tax intake. The debt-to-GDP ratio remained relatively stable during this period, generally hovering between 34 and 38 percent. Even with chronic primary deficits, nominal growth in the denominator absorbed new borrowing, masking the underlying structural imbalance that the Comité Autónomo de la Regla Fiscal (CARF) would later flag as the persistent driver of fiscal stress.

The mechanics of the ratio changed sharply when Brent crude prices collapsed in late 2014. Reduced hydrocarbon royalties widened the fiscal gap just as the Colombian peso depreciated against the US dollar. Because a significant share of Colombia’s sovereign liabilities is denominated in foreign currency, the peso’s slide automatically inflated the local-currency value of outstanding external debt when measured against domestic GDP. The combined effect — wider deficits funded by new borrowing, plus a valuation effect on existing dollar-denominated obligations — pushed the ratio steadily higher through the late 2010s.

The structural revenue weakness that surfaced during this period has remained a recurring theme in subsequent fiscal assessments from Fedesarrollo and the Pontificia Universidad Javeriana Observatorio Fiscal, both of which have noted that successive tax reforms failed to fully close the gap between commitments and ordinary income.

The combination of emergency social spending under the Ingreso Solidario program, expanded health outlays and a sharp contraction in nominal GDP drove the ratio to a historic peak above 65 percent in 2020. The Ministerio de Hacienda reports the all-time high at 65.3 percent of GDP that year. The government activated the escape clause of the regla fiscal — Colombia’s fiscal rule, codified in Law 1473 of 2011 and modified by Law 2155 of 2021 — to accommodate the spending response, suspending the rule for 2020 and 2021.

That episode also triggered the first sovereign downgrade cycle: S&P Global Ratings cut Colombia’s long-term foreign currency rating to BB+ from BBB- in May 2021 after the administration of then-president Iván Duque withdrew a tax reform bill following street protests, costing the country its investment-grade status with that agency.

Strong post-pandemic nominal growth briefly pulled the debt ratio down toward 57 percent in 2023. The decline did not hold. Structural spending pressures, elevated international interest rates and tax collections below budgeted projections pushed the ratio back up, establishing a new operating band around 60 to 62 percent of GDP. The Ministerio de Hacienda reported government debt to GDP at 61.3 percent for 2024.

The administration of President Gustavo Petro and Finance Minister Germán Ávila Plazas activated the regla fiscal escape clause for a second time in June 2025, with the Consejo Superior de Política Fiscal (Confis) approving a three-year suspension covering 2025 through 2027. The decision came despite an unfavorable technical opinion from the Comité Autónomo de la Regla Fiscal, which concluded that legal conditions for activating the clause were not met outside of a national emergency. The clause had previously been invoked only during the COVID-19 pandemic.

According to the Marco Fiscal de Mediano Plazo (MFMP) presented by the Ministerio de Hacienda, net public debt to GDP is projected to rise from 53 percent in 2023 to 61.3 percent in 2025 and approximately 63 percent in 2026. The fiscal deficit for 2025 was initially projected at 7.1 percent of GDP and later revised to roughly 6.2 percent of GDP, with the administration targeting a deficit below 6 percent of GDP for 2026.

The cost of servicing this debt has reshaped the structure of the national budget. The 2026 draft budget presented by Minister Ávila totals $557 trillion COP, equivalent to roughly $134.7 billion USD, and represents 28.9 percent of GDP. Of that, debt servicing costs are projected at $102.5 trillion COP, or 5.3 percent of GDP, down from 6.2 percent of GDP in 2025.

The figures published by the Ministerio de Hacienda for domestic debt service in 2026 are higher when measured against tax intake alone: of an estimated $130 trillion COP in domestic debt service, $79 trillion COP corresponds to principal that can be rolled over through new issuances, while $51 trillion COP represents interest payments funded directly from the budget. Against projected tax revenue of approximately $300 trillion COP, that implies roughly one in every three pesos collected by the central government is allocated to interest on existing debt.

The rating cycle has accelerated alongside the fiscal trajectory. Moody’s Ratings downgraded Colombia to Baa3 and subsequently into junk territory in 2025, citing the suspension of the fiscal rule. S&P Global Ratings issued a further downgrade in April 2026, its second cut in less than a year, on the same persistent deficit and debt concerns. Fitch Ratings also moved Colombia deeper into speculative grade in December 2025.

The Banco de la República reported external debt — combining public and private liabilities — at $238.7 billion USD at the close of November 2025, equivalent to 54.8 percent of GDP, an increase of $15.8 billion USD from January of the same year. The Colombian economy is currently valued at approximately $435 billion USD.

The Comité Autónomo de la Regla Fiscal has stated in its most recent reports to Congress that the 2025 primary balance target was missed by a wide margin even after the escape clause was activated, and that incoming projections for 2026 raise the bar for any return to the original fiscal rule by 2028. Business groups including Fenalco and the Consejo Gremial Nacional have publicly opposed the suspension and signaled potential legal challenges.

The 2026 financing plan disclosed by the Ministerio de Hacienda includes approximately $4.6 billion USD in global bond issuances, primarily to refinance a one-year Swiss-franc Total Return Swap operation valued at roughly $9.3 billion USD. The ministry has stated that the issuance does not constitute net new external debt. Updated debt and deficit targets are scheduled for release in the next iteration of the Plan Financiero.

For executives operating in Colombia or evaluating new investment, the baseline shift from a mid-30s to a low-60s debt-to-GDP environment alters several variables simultaneously: peso volatility tied to refinancing cycles, the trajectory of corporate tax policy as Congress weighs successive reform proposals, and the path of domestic interest rates set by the Banco de la República as it manages inflation alongside elevated sovereign funding costs. Detailed historical and forward-looking debt data is published by the Investor Relations Colombia office of the Ministerio de Hacienda.

Colombia’s General Government Debt-to-GDP Ratio (2006-2026) (image: Google)

Colombia votes on May 31 with its presidential race concentrated around three candidates whose platforms diverge on nearly every dimension of economic and security policy relevant to foreign investors. For corporate executives, institutional investors, and multinational operations with Colombian exposure, the choice between senator Iván Cepeda, senator Paloma Valencia, and defense attorney Abelardo de la Espriella carries direct, measurable implications for the regulatory environment, foreign direct investment (FDI) conditions, energy sector licensing, and geopolitical alignment through at least 2030.

No candidate is projected to clear the 50%-plus-one threshold required to win outright on May 31, making a runoff election on June 21 the expected outcome. The question that will determine the direction of that runoff — and by extension the next administration — is which of the two opposition candidates finishes second.

Click above to play the video!

The final-week polling picture shifted substantially, and the trajectory matters as much as the snapshot. The CONDOR weighted aggregate — which incorporates surveys from six polling firms and applies greater weight to more recent data — placed the race as of May 23 at: Cepeda 36.3%, De la Espriella 29.1%, Valencia 16.7%.

Invamer, one of Colombia’s most established polling firms, surveyed 3,800 respondents across 152 municipalities between May 13 and May 20, registering Cepeda at 44.6%, De la Espriella at 31.6%, and Valencia at 14.0%. The Centro Nacional de Consultoría (CNC) published a survey conducted May 22 and 23 showing Cepeda at 33.4%, De la Espriella at 30.9%, and Valencia at 12.6%.

Comparing those figures to the Fundación Génesis Crea survey from May 4 through May 11 — which placed Cepeda at 35.1%, Valencia at 25.4%, and De la Espriella at 21.6% — indicates a multi-poll trend of De la Espriella gaining approximately nine to ten percentage points in three weeks while Valencia shed a comparable share. AS/COA’s poll tracker confirms the directional consistency across firms.

Atlas Intel, which published figures more favorable to De la Espriella, is currently under investigation by Colombia’s Consejo Nacional Electoral (CNE) for potential methodology violations and could face suspension of its operations. Those figures are treated with caution in this analysis.

Runoff modeling diverges between firms. Fundación Génesis Crea showed Valencia defeating Cepeda 49.1% to 44.7% in a second-round matchup — meaning she was the stronger opposition candidate in that scenario. The Guarumo/Ecoanalítica survey found Cepeda losing all hypothetical runoff scenarios, including against De la Espriella. Two minor candidates — former senator Clara López and former Chocó governor Luis Gilberto Murillo — withdrew and endorsed Cepeda before the first round, a consolidation that appears to have had limited effect on his polling numbers.

Finance Colombia reported in May that the campaign has been marked by an unusual absence of traditional televised debates. Cepeda declined to participate in events organized by major media outlets, stating that proposed formats lacked neutrality. Former Bogotá Mayor Claudia López, herself a candidate, said publicly that Cepeda’s refusal was motivated by an unwillingness to defend his record as the architect of President Gustavo Petro‘s Paz Total security negotiation strategy.

Public security is the top voter concern heading into the election. InSight Crime documented that the Ejército de Liberación Nacional (ELN) launched a major offensive against FARC dissident factions in Norte de Santander in early 2025, resulting in mass civilian casualties in the Catatumbo region. In Chocó and Antioquia, the ELN and the Autodefensas Gaitanistas de Colombia (AGC), commonly known as the Clan del Golfo, are competing for control of illegal gold mining corridors and drug trafficking routes. In Cauca, FARC dissident factions have established territorial control in areas where state presence has collapsed.

Cepeda’s approach to security is defined by his role as the principal legislative architect of Paz Total. As chair of the Senate‘s peace commission, he designed the framework that extended negotiating status to the ELN, FARC dissident groups, and the Clan del Golfo. His stated rationale is that targeting the financial leadership of drug networks rather than foot soldiers produces more durable results — a position that has academic backing in narcotics policy literature. In practice, Paz Total produced ceasefires that were repeatedly violated, and security indicators in conflict-affected departments deteriorated during the Petro administration. A Cepeda presidency is expected to continue the negotiated settlement model, with the military operating under political constraints.

Cepeda’s approach to security is defined by his role as the principal legislative architect of Paz Total. As chair of the Senate‘s peace commission, he designed the framework that extended negotiating status to the ELN, FARC dissident groups, and the Clan del Golfo. His stated rationale is that targeting the financial leadership of drug networks rather than foot soldiers produces more durable results — a position that has academic backing in narcotics policy literature. In practice, Paz Total produced ceasefires that were repeatedly violated, and security indicators in conflict-affected departments deteriorated during the Petro administration. A Cepeda presidency is expected to continue the negotiated settlement model, with the military operating under political constraints.

Valencia’s security platform is based on reinstating Seguridad Democrática, the doctrine associated with former president Álvaro Uribe’s administrations from 2002 to 2010. The core elements are expanded military presence in rural conflict zones, dismantling of rural criminal networks, and resumption of extradition agreements with the United States — which Petro suspended, effectively shielding cartel leadership from US federal prosecution. The Uribe-era approach resulted in measurable reductions in homicide rates, forced displacement, and ELN and FARC territorial control, though human rights organizations documented serious abuses by security forces during that period.

De la Espriella has stated explicitly that his government would have no peace process. He advocates for a model similar to El Salvador’s under President Nayib Bukele: mass incarceration, construction of high-security prison facilities, classification of guerrilla and cartel organizations as foreign terrorist organizations, and broad military offensives. He has not detailed how such operations would be financed or how the mass detention model would interact with Colombia’s Constitutional Court, which has repeatedly constrained executive security powers.

For the armed groups operating in Norte de Santander and Cauca, the historical record indicates that Colombia’s criminal organizations respond more acutely to sustained, institutionally grounded military pressure and functioning extradition pipelines than to political rhetoric. By that measure, Valencia’s platform — which rebuilds the institutional security apparatus incrementally — represents a more structurally credible threat to the ELN and the Estado Mayor Central (EMC) FARC dissidents. For the Clan del Golfo leadership, extradition to the United States has historically been the principal deterrent, and Valencia’s program explicitly restores it.

The Petro administration enacted a series of minimum wage increases totaling more than 60% over four years — including a 16% increase for 2023, the largest single-year hike in Colombian history, and a 23.78% increase for 2026 — restructured labor regulations to expand premium pay requirements for night, weekend, and holiday shifts, and raised corporate tax rates to fund social spending programs. The Asociación Nacional de Empresarios de Colombia (ANDI) characterized the regulatory environment as adverse to private investment. Finance Colombia tracked a material decline in FDI in the extractive sector over the same period.

Cepeda supported those labor and fiscal reforms throughout their legislative passage. His platform extends the Petro model: increased state social spending, continued land redistribution programs, and maintenance of the current wage and labor cost structure. For companies with established Colombian operations, the regulatory environment is manageable; for companies evaluating market entry or operational expansion, the cost structure adds friction.

Valencia’s economic program emphasizes corporate stability and private sector investment as the primary mechanisms of job creation. Her vice-presidential running mate, Juan Daniel Oviedo — former director of DANE, Colombia’s national statistics agency — represents a technocratic orientation focused on reducing structural market distortions, streamlining public procurement, and scaling back state administrative overhead. Oviedo’s appointment is a direct signal to the business community that economic management would be data-driven rather than ideologically directed. Oviedo also publicly identifies as a member of the LGBTQ+ community, a departure from the traditional social conservatism of Centro Democrático.

De la Espriella’s economic orientation is pro-business with protectionist elements. His vice-presidential candidate, José Manuel Restrepo — who served as Colombia’s Finance Minister and Commerce Minister — provides institutional credibility on fiscal and trade policy. Restrepo’s presence on the ticket signals commitment to fiscal discipline and regulatory reduction in the extractive and commercial sectors. De la Espriella’s personal style, however, introduces operational uncertainty; his campaign has generated multiple high-profile controversies, including a public altercation with Caracol Noticias journalist María Lucía Fernández during a live broadcast and a formal apology following misconduct allegations by journalist Laura Rodríguez of Piso 8 FM.

Ecopetrol holds a 31.5% stake in the Gunflint oil field in the Gulf of Mexico.

The extractive sector is the most consequential economic policy dimension for international capital. Ecopetrol (NYSE: EC; BVC: ECOPETROL) — Colombia’s state-controlled energy company and the largest corporation in the country — has operated under exploration restrictions during the Petro administration, which has opposed new fossil fuel contracts on climate grounds.

Cepeda’s position extends the Petro framework: mandatory transition away from fossil fuels, heavy restrictions or outright prohibitions on new oil and gas exploration contracts, and stringent environmental licensing requirements for open-pit mining operations. Foreign investment would be directed by policy toward green hydrogen, ecotourism, and smallholder agriculture. For the multinational oil majors with Colombian operations and for institutional investors in the mining sector, a Cepeda presidency represents a continuation of the current constraints and, in some contract scenarios, an accelerated wind-down of Colombian portfolios.

In a related development, Finance Colombia reported in May that Ecopetrol’s president, Ricardo Roa, has been formally charged in connection with alleged campaign spending violations during Petro’s 2022 presidential campaign. The case will be inherited by whoever takes office in August.

Valencia’s position is that hydrocarbon revenues are essential to Colombia’s macroeconomic stability and that the country cannot exit the sector before alternative revenue structures exist. Her platform actively encourages FDI in petroleum exploration, is open to regulated fracking, and commits to clearing the environmental licensing backlog that has stalled multiple large-scale gold and copper mining projects. For energy and mining companies currently blocked by administrative delays, this represents the most direct path to project advancement.

De la Espriella’s position goes further: essentially deregulating the environmental licensing process for major extraction projects on the grounds that Colombia’s economic sovereignty takes precedence over environmental restrictions he characterizes as externally imposed. The practical constraint is whether a De la Espriella administration would have the institutional coherence and congressional support to deliver regulatory rollback, given that his movement has no established political party structure and entered the race through an independent signature campaign.

The US Embassy in Bogotá is said to be the 3rd largest US mission in the world (photo: Loren Moss)

Colombia’s relationship with the United States deteriorated materially under Petro, who aligned Colombia with Venezuela’s Nicolás Maduro, pursued closer ties with China and Russia, and suspended extradition agreements. US counternarcotics cooperation was strained throughout the period.

Cepeda is committed to what he describes as a multipolar foreign policy — maintaining functional diplomatic channels with Washington and Brussels while deepening strategic and commercial relationships with China and Russia. His alignment with regional left-of-center governments in Mexico, Brazil, and Bolivia would position Colombia as part of a Latin American bloc that has grown increasingly skeptical of US regional leadership. For US companies operating in Colombia, this trajectory does not mean immediate operational disruption, but it reduces Colombia’s utility as a reliable counterpart on security cooperation, counter-narcotics intelligence sharing, and trade dispute resolution.

Valencia positions a return to the Western alignment as a core objective. She would prioritize restoring the US-Colombia relationship, reinforcing the bilateral Free Trade Agreement, and reestablishing intelligence-sharing mechanisms that were reduced under Petro. Her framing positions Colombia as a democratic anchor in a region experiencing authoritarian pressures.

De la Espriella takes the most explicit pro-US position in the race. La Silla Vacía reported that De la Espriella or entities linked to his campaign donated more than $90,000 USD to the US Republican Party, a fact that raises questions about the nature and expectations of those relationships. He has publicly aligned himself with the populist right in the United States, takes a hostile posture toward China, Russia, and Venezuela, and has characterized his security approach as consistent with a transactional alliance with Washington focused on counter-narcotics enforcement and cartel designation as foreign terrorist organizations.

“Ese pisco robó a 200 mil colombianos.” — Claudia López, former Mayor of Bogotá, referring to presidential candidate Abelardo de la Espriella’s legal representation of DMG pyramid scheme founder David Murcia Guzmán, during a presidential campaign event.

All three candidates have stated commitments to fighting corruption, though their approaches and focal points differ in ways that are material to the institutional environment for business operations.

Cepeda’s legislative record includes serious, documented work investigating paramilitary infiltration of Colombia’s political institutions — the period known as parapolítica — and pursuing accountability for those cases. His blind spot, his critics argue, is corruption within the current administration. When Ecopetrol’s Ricardo Roa was formally charged in connection with Petro’s 2022 campaign, the response from the Pacto Histórico coalition was subdued. Cepeda has been Álvaro Uribe’s primary judicial antagonist in the Senate; a Cepeda administration would offer no institutional protection to Uribe and would be expected to support the full progress of judicial proceedings against him. For left-wing politicians facing legal exposure, including former Medellín mayor Daniel Quintero, a Cepeda administration would be expected to be more receptive to amnesty frameworks.

Valencia’s approach to anti-corruption is structural rather than prosecutorial: strengthening the independence of the Contraloría General de la República and the Fiscalía General de la Nación, implementing digital transparency in public procurement, and reducing informal executive influence over judicial processes. She would be expected to apply political and rhetorical pressure on behalf of Uribe — her political mentor and a close ally — though her legislative track record indicates a degree of institutional independence from Centro Democrático party orthodoxy.

De la Espriella’s anti-corruption rhetoric centers on severe criminal penalties for corrupt officials. The credibility of that position is complicated by his professional history, which is examined in detail below.

De la Espriella’s campaign has faced sustained scrutiny over his client history as one of Colombia’s highest-profile criminal defense attorneys. The record is documented in reporting by El Colombiano, El Espectador, and the investigative outlet Corrupción al Día.

Abelardo de la Espriella (screen capture from Twitter video)

His documented client roster includes Salvatore Mancuso, the former supreme commander of the Autodefensas Unidas de Colombia (AUC) paramilitary network; multiple legislators convicted in the parapolítica scandal, which established systematic infiltration of Colombia’s congress by paramilitary organizations; David Murcia Guzmán, the operator of the DMG pyramid scheme that defrauded an estimated 200,000 Colombian investors; the Nule Primos, convicted of large-scale public contract fraud; and Álex Saab, the Colombian businessman extradited to the United States on charges of acting as the primary money launderer for the Maduro government in Venezuela. According to Corrupción al Día, De la Espriella’s legal fees from Saab reportedly reached $12 million USD and included private aircraft travel.

De la Espriella’s response to this line of criticism rests on due process principles: that every accused person is entitled to vigorous legal defense regardless of the charges, and that his ability to navigate Colombia’s criminal code at its most complex levels demonstrates the expertise required to enforce the law from the executive branch. The argument has legal validity as a principle. The specific issue for foreign compliance officers and US government counterparts is the Saab representation: the same Nicolás Maduro whose regime De la Espriella’s campaign now characterizes as an ideological enemy received legal services from De la Espriella’s firm when the representation was commercially available.

The Fiscalía investigated De la Espriella in connection with alleged paramilitary links in 2009 and again in 2012; both investigations were dismissed for insufficient evidence, and he carries no convictions or active investigations on those matters.

Iván Cepeda (from Twitter)

Critics of Iván Cepeda, including Enrique Gómez of the Salvación Nacional party, have argued that his family background constitutes evidence of structural alignment with guerrilla movements. The record on this point merits examination.

Cepeda is the son of Manuel Cepeda Vargas, who served as Secretary-General of the Colombian Communist Party and as a senator for the Unión Patriótica (UP), a left-wing political movement that was systematically exterminated by a combination of state actors and paramilitary organizations during the 1980s and 1990s. Manuel Cepeda Vargas was assassinated on August 9, 1994. The Inter-American Court of Human Rights subsequently found the Colombian state responsible for his murder. The FARC-EP named its Frente Urbano Manuel Cepeda Vargas — an urban front operating within the Bloque Occidental — in the elder Cepeda’s honor.

The Fundación Paz y Reconciliación (PARES) has documented that Iván Cepeda’s relationship with his father’s political positions was more complex than the family lineage alone suggests. After studying in Bulgaria in 1981, Cepeda broke from his father’s Soviet-oriented communist framework and aligned with democratic leftists including Bernardo Jaramillo Ossa, who publicly rejected the FARC’s armed strategy. Cepeda has repeatedly stated his repudiation of the FARC’s use of his father’s name. No documented evidence connects him to operational coordination with current armed groups.

What the family history does establish is the ideological framework through which Cepeda processes security policy: a belief, grounded in personal and political experience, that the Colombian state’s institutional violence has been as destructive as guerrilla violence, and that negotiated settlements are structurally preferable to military solutions. That framework generates Paz Total. It also generates a posture toward ELN and FARC dissident negotiators that prioritizes process continuity over verified compliance — a disposition that armed groups have demonstrably exploited to maintain territorial and operational positions while negotiation frameworks provided legal cover.

Paloma Valencia (image Twitter)

The comparison to former president Iván Duque (2018–2022) comes up regularly in discussions of Valencia’s political independence. Duque, who had limited independent political standing before Uribe selected him, was perceived throughout his term as governing within constraints set by his patron — a dynamic that Colombian political cartoonists characterized as ventriloquism.

Valencia’s profile differs materially. She is the granddaughter of former Colombian president Guillermo León Valencia, carries her own political lineage, and has served in the Senate for over a decade, building positions on agrarian reform, judicial modernization, and indigenous land rights that have placed her at variance with standard Centro Democrático positions on those issues. She won the Gran Consulta por Colombia primary on March 8 with more than 45% of the vote — over 3.2 million Colombians — establishing a democratic mandate distinct from any party endorsement.

She would be expected to use institutional and rhetorical channels to support Uribe in the ongoing judicial proceedings against him, and to apply pressure on the trajectory of those cases. Whether that constitutes political interference with judicial independence or normal advocacy within democratic norms is a question on which observers disagree. What the legislative record does not support is the characterization of Valencia as incapable of independent governance.

Press freedom carries an indirect but measurable correlation with rule-of-law quality, which in turn affects operational risk for companies that rely on regulatory predictability and transparent legal processes.

Cepeda has maintained a posture toward critical media that mirrors President Petro’s practice of characterizing adversarial outlets as acting in the interests of economic elites. Under Petro, this produced a systematic exclusion of critical media from official information flows and persistent rhetorical delegitimization of independent journalism, though the press remained legally free to operate. A Cepeda administration would be expected to continue this pattern.

Valencia’s background in Colombia’s traditional political and intellectual establishment, combined with a decade in a party that has faced sustained critical coverage from Colombia’s major outlets, points toward a conventional institutional relationship with the press — adversarial at times, but within professional norms.

De la Espriella’s conduct during the campaign provides direct evidence of his approach. He publicly called Caracol Noticias journalist María Lucía Fernández “ignorant” in a live interview. He issued a formal apology after journalist Laura Rodríguez of Piso 8 FM made allegations of inappropriate conduct. His campaign strategy has drawn comparisons to the approach of Argentine president Javier Milei and US president Donald Trump in its use of direct digital channels to circumvent traditional media while publicly attacking outlets that publish critical coverage. The press would remain legally protected under a De la Espriella administration, but the operational environment for investigative journalism would be hostile.

The question of which candidate is most aligned with free-market principles requires a distinction that the international business press frequently elides: the difference between economic deregulation and political authoritarianism. These can, and in this election do, exist independently.

De la Espriella’s platform is often described in international coverage as the most pro-market. His deregulation proposals for the extractive sector and his corporate tax rhetoric support that reading in the economic domain. His security platform, however, involves a substantial expansion of state coercive power: mass detention operations, a mega-prison construction program, and the suspension of standard due process protections to facilitate rapid incarceration of criminal suspects. The Cato Institute‘s framework of economic freedom as inseparable from civil liberties would categorize a state powerful enough to detain people without standard procedural protections as a state that represents an institutional risk to property rights and contract enforcement as well.

Valencia’s platform, anchored by Oviedo’s technocratic program of structural market reform — reduced administrative barriers, streamlined procurement, smaller state overhead, maintained civil liberties — represents the closest approximation to coherent market liberalism available in this field. It does not carry the rhetorical force of De la Espriella’s deregulation proposals, but it has more institutional grounding.

Cepeda’s platform is the furthest from market liberalism by any standard measure: state-directed investment allocation, wealth redistribution through tax and transfer mechanisms, state expansion in healthcare and pension administration, and agrarian land redistribution. His program is continuous with the Petro administration’s economic framework.

Claudia López, senator of Colombia. (Credit: Patty Suescún)

Several other candidates remain on the ballot and are drawing small but potentially consequential vote shares in a first round where the margin between second and third place could be narrow.

Claudia López, former mayor of Bogotá running under the Con Claudia Imparables coalition, positions herself as a progressive centrist with a documented anti-corruption record. Her polling has not broken 3.5% in major surveys, and her high polarization ratings from her mayoral term limit her growth ceiling. Her attacks on De la Espriella during the campaign — she publicly called him a “defender of the mafia” in reference to his client history — have been among the most pointed in the race, and factually grounded on the public record.

Sergio Fajardo, making his third consecutive presidential run under Dignidad y Compromiso, continues to represent a technocratic, education-focused centrism grounded in his work transforming Medellín in the early 2000s. He has not broken 3.5% in any major poll in this cycle.

Roy Barreras, running under La Fuerza de la Paz following his Frente por la Vida primary victory, is one of the most experienced political operatives in Colombia, having been part of multiple coalition governments across ideological lines over two decades. He polls below the threshold for meaningful first-round impact.

Miguel Uribe Londoño, running under Partido Demócrata, represents a younger-generation conservative platform emphasizing fiscal discipline and private sector growth, broadly consistent with Valencia’s program. He also polls below 3.5%.

Carlos Caicedo, running on a regionalist platform emphasizing decentralization away from Bogotá, draws support primarily from the Costa Caribe. His structural argument about Colombia’s administrative over-centralization is substantively grounded, though his national profile is insufficient to affect the first-round outcome.

For international capital with Colombian exposure, the three-way race produces three materially different operational scenarios.

A Cepeda victory — which remains the single most likely first-round outcome based on available polling — would signal continuity of the Petro-era regulatory framework: sustained capital outflow pressure, high corporate tax rates, no new fossil fuel exploration contracts for Ecopetrol (NYSE: EC; BVC: ECOPETROL) or private operators, continued labor cost escalation, and a foreign policy trajectory away from Washington. Colombian equity valuations would be expected to remain under pressure. The mining licensing backlog would continue to accumulate. A Cepeda administration would not replicate Venezuela’s economic trajectory — Colombia’s independent central bank, Banco de la República, its functioning constitutional court, and its institutional depth provide meaningful buffers — but the investment headwinds would be structural rather than cyclical.

A Valencia victory would represent the sharpest regulatory reversal available in this field. Ecopetrol exploration contracts would be expected to advance. The mining licensing backlog would be addressed. US bilateral relations would be restored, reactivating security intelligence cooperation and trade facilitation mechanisms. The Colombian peso would be expected to strengthen as country risk premium declined. The path to that outcome now requires her to either close the gap significantly on De la Espriella in the first round or rely on runoff polling that showed her as the stronger second-round candidate — data that predates the most recent polling shift.

A De la Espriella victory introduces the widest distribution of possible outcomes. The upside scenario involves Restrepo managing fiscal and trade policy competently, genuine regulatory rollback in the extractive sector, aggressive extradition resumption, and security operations that reduce the physical risk premium in conflict-affected departments including Cauca, Norte de Santander, and Chocó. The downside scenario involves recurring crises generated by De la Espriella’s personal conduct, conflicts of interest arising from his former client relationships, and authoritarian security measures that attract international human rights attention and complicate bilateral relationships. Restrepo’s presence on the ticket reduces the probability of the downside scenario but does not eliminate it.

The current polling trend indicates that right-wing voters are consolidating around De la Espriella at Valencia’s expense. Whether that consolidation produces a runoff between De la Espriella and Cepeda — and whether the runoff produces a left or right-wing government — remains uncertain. What the polling data does not support is the scenario, widely assumed until recently, of a Cepeda-Valencia runoff in which Valencia was positioned as the structurally stronger opposition candidate.

Subscribe to Finance Colombia to remain updated on key developments and impartial analysis.

Holland & Knight has named José Vicente Zapata executive partner of its Bogotá office, the firm announced on May 4, 2026. Zapata will oversee day-to-day management of the office while continuing to lead his energy practice, which focuses on corporate, contractual, and commercial matters, with an emphasis on spin-offs and mergers and acquisitions. He succeeds Enrique Gómez Pinzón, who has served as executive partner since the office opened in 2012 and will now take the title of executive partner emeritus while continuing his corporate, M&A, finance, and international arbitration practice.

Zapata has been with Holland & Knight for nearly 12 years and co-chairs the firm’s Venezuela Focus Team, a group of partners who advise clients with interests in that country. His regulatory work covers environmental, energy, and natural resources matters, as well as corporate compliance, including the design of ethics programs and compliance with Colombia’s Sistema de Autocontrol y Gestión del Riesgo Integral de Lavado de Activos y Financiación del Terrorismo (SAGRILAFT) anti-money-laundering and counter-terrorism financing regime. He also handles liability cases involving contractual and non-contractual damages.

“I look forward to continuing to strengthen our team’s offerings in advising Colombian companies and guiding international clients to navigate entry into the Colombian market.” — José Vicente Zapata, Executive Partner, Holland & Knight Bogotá

Zapata earned his LL.M. in Sustainable Development and International Business Law from McGill University in Montreal and his J.D. from the Pontificia Universidad Javeriana in Bogotá. He has been ranked in Energy & Natural Resources: Environment by Chambers Global and Chambers Latin America since 2014, was named to The Legal 500 Latin America Hall of Fame in Environment in 2025 and 2026, and is regularly listed in The Best Lawyers in Colombia.

“I look forward to continuing to strengthen our team’s offerings in advising Colombian companies and guiding international clients to navigate entry into the Colombian market,” Zapata said in a written statement.

Bob Grammig, Holland & Knight’s chair and chief executive officer, said Zapata’s appointment was intended to focus the office on growth in Colombia and across Latin America. Gómez Pinzón said he would continue to support the office in his emeritus role.

The Bogotá office now houses nearly 70 lawyers. Its practice covers cross-border deals and international trade; mergers, acquisitions, and joint ventures; oil, gas, and mining projects; environmental assessments, liability, and compliance; taxation; labor law; intellectual property, trademark, and patent registration; antitrust and consumer law; capital markets, venture capital, and private equity; international licensing and franchising; project finance and foreign investment; corporate reorganizations and financial restructurings; litigation and international arbitration; and private wealth services.

Holland & Knight’s Latin America Practice Group includes more than 200 attorneys working on cross-border M&A, joint ventures, private equity and financing transactions, and disputes involving Latin America. The firm overall counts approximately 2,200 lawyers and other professionals across 35 offices. Founded in 1889, it provides representation in litigation, corporate and finance, real estate, healthcare, and government matters.

The leadership transition comes as international firms continue to deepen their footprint in Bogotá to serve foreign investors entering Colombian energy, infrastructure, and natural resources markets, and to advise Colombian corporates pursuing transactions abroad.

Frontera Energy Corporation (TSX: FEC) (OTCQX: FECCF) reported first-quarter 2026 net income from continuing operations of $13.1 million USD and adjusted EBITDA of $28.5 million USD, as the Calgary-based company moves to close the sale of its Colombian exploration and production portfolio to Parex Resources Inc. (TSX: PXT) and reposition itself as a standalone Colombian infrastructure company anchored by its pipeline and port assets.

Total revenues from continuing operations were $26.8 million USD in the first quarter, compared with $26.9 million USD in the fourth quarter of 2025 and $25.1 million USD in the first quarter of 2025. Net loss for the period, including discontinued operations, was $15.4 million USD, reflecting a $28.5 million USD net loss from the Colombian E&P assets now classified as held for sale.

“In total, this strategy will have unlocked approximately $1.3 billion of capital for investors.” — Gabriel de Alba, Chairman of the Board, Frontera Energy Corporation

On April 30, 2026, Frontera shareholders approved a plan of arrangement under which Parex Resources, through a wholly-owned subsidiary, will acquire all of Frontera’s Colombian upstream business — including its oil and gas exploration and production assets, a reverse-osmosis water-treatment facility, and a palm-oil plantation. The transaction carries an enterprise value of $750 million USD. The cash purchase price consists of $500 million USD payable at closing, subject to customary adjustments, plus an additional $25 million USD contingent payment tied to specified development milestones to be achieved within 12 months of closing.

At the same shareholder meeting, investors approved a reduction of Frontera’s capital account of up to $647 million CAD (approximately $470 million USD) to fund a return of capital to shareholders from the net proceeds of the transaction. The Supreme Court of British Columbia issued its final order approving the arrangement on May 4, 2026. Closing remains subject to the satisfaction of remaining conditions and is expected in May 2026.

Chairman Gabriel de Alba said the company would retain roughly $50 million USD of cash to support growth opportunities at the remaining infrastructure business, including an LNG regasification project being developed in partnership with Ecopetrol (NYSE: EC) (BVC: ECOPETROL). “In total, this strategy will have unlocked approximately $1.3 billion of capital for investors,” de Alba said.

Frontera holds a 35 percent equity interest in the Oleoducto de los Llanos (ODL) crude oil pipeline, which connects the Rubiales, Quifa, Caño Sur, Llanos-34, and other production blocks to the Monterrey and Cusiana stations in the department of Casanare. ODL’s share of income contributed $14.2 million USD to Frontera in the first quarter, compared with $15.1 million USD a year earlier, with the year-over-year decline reflecting higher depreciation, amortization, and operating costs.

ODL transported 233,875 barrels per day in the first quarter of 2026 at an average tariff of $4.70 USD per barrel, compared with 236,387 barrels per day at $4.73 USD per barrel in the first quarter of 2025. The pipeline declared $185 million USD in total dividends, of which $64.7 million USD is net to Frontera. The company expects to receive those distributions during 2026 in installments of approximately 40 percent in the second quarter, 35 percent in the third quarter, and 25 percent in the fourth quarter.

Long-term debt at Frontera totaled $167.8 million USD at the end of the first quarter and is expected to decline to approximately $131 million USD by year-end 2026, primarily through scheduled amortizations and cash-sweep mechanisms tied to ODL cash flows. From May 2025 through December 2026, long-term debt is expected to fall by more than $100 million USD.

Puerto Bahía, the multipurpose maritime terminal located in Cartagena adjacent to the Bocachica access channel and near the Reficar refinery, generated $12.7 million USD in revenue in the first quarter of 2026, compared with $10.0 million USD in the same period a year earlier. The 150-hectare facility comprises a hydrocarbons terminal with nominal capacity of 2,672,000 barrels and a general cargo terminal. Frontera holds a 99.97 percent equity interest in the port.

General cargo growth offset weaker liquids volumes. The general cargo terminal handled 38,067 roll-on/roll-off (RORO) units in the first quarter, more than double the 18,223 units handled a year earlier, alongside 3,851 twenty-foot equivalent units (TEUs) of containerized cargo, up from 1,256 TEUs in the first quarter of 2025. Break-bulk volumes declined to 25,216 tons/m³ from 41,198 tons/m³. RORO dwell times shortened from 40 days to 31 days year over year.

The liquids terminal handled 36,937 barrels per day in the first quarter of 2026, down from 51,579 barrels per day a year earlier. Ecopetrol volumes accounted for 26,273 barrels per day, Frontera-related volumes for 7,389 barrels per day, and other third-party volumes for 3,275 barrels per day. The company attributed the decline mainly to lower third-party throughput and the absence of certain trading flows.

Operating costs at the port rose to $7.6 million USD in the first quarter from $5.0 million USD a year earlier, driven by increased infrastructure maintenance in the liquids terminal and higher cargo volumes in the general cargo facility.

Puerto Bahía’s liquefied petroleum gas (LPG) project began initial operations in March 2026, providing capacity to handle up to 10,000 tons per month. The terminal is targeted to become fully operational during the first quarter of 2028. Capital expenditures during the first quarter totaled $1.0 million USD, including $0.4 million USD for major tank maintenance and $0.3 million USD for the LPG project.

The company is also advancing an LNG regasification project at Puerto Bahía in partnership with Ecopetrol, intended to support Colombia’s domestic gas supply as domestic production declines. Frontera is also pursuing expansion of containerized cargo operations.

Following the execution of the arrangement agreement, the Colombian E&P assets are now classified as discontinued operations under IFRS 5. Colombian production averaged 36,700 barrels of oil equivalent per day in the first quarter of 2026, comprising 25,394 barrels per day of heavy crude, 8,653 barrels per day of light and medium crude combined, 5,706 thousand cubic feet per day of conventional natural gas, and 1,652 barrels of oil equivalent per day of natural gas liquids. That compares with 39,010 barrels of oil equivalent per day a year earlier.

The operating netback from the discontinued Colombian operations was $41.79 USD per barrel of oil equivalent in the first quarter of 2026, compared with $34.22 USD per barrel of oil equivalent in the first quarter of 2025, supported by a higher Brent reference price of $78.38 USD per barrel against $74.98 USD per barrel a year earlier.

Frontera retains exploration and development interests in Guyana through subsidiaries that include CGX Energy Inc. (TSXV: OYL), which is not part of the Parex transaction. The company’s go-forward portfolio will be anchored by the ODL pipeline stake and Puerto Bahía, with the infrastructure business generating approximately $77 million USD of distributable cash flow in 2025, according to the management information circular dated March 30, 2026.

Above photo courtesy Frontera Energy Corporation.

Non-resident visitor arrivals to Colombia grew 6.7% in March 2026 compared to the same month of the previous year, and the country received 1,584,378 non-resident visitors during the first quarter, according to figures from Migración Colombia processed by the Ministerio de Comercio, Industria y Turismo.

In March alone, 541,720 non-resident visitors entered the country. Of that total, 419,150 were foreign non-resident visitors, representing 5.3% year-over-year growth, while the cruise segment recorded 58,186 passengers, a 41.2% increase over the same month in 2025.

For executives and investors evaluating Colombia’s tourism, hospitality, and aviation sectors, the data indicate continued recovery in international arrivals and a measurable expansion of cruise traffic, two segments that directly affect hotel occupancy, retail spending in coastal cities such as Cartagena and Santa Marta, and the pipeline of inbound foreign exchange.

“Colombian tourism is going through a significant period of international expansion. Colombia is recording sustained growth in visitor arrivals while strengthening its connectivity and expanding its presence in strategic markets,” said Diana Marcela Morales Rojas, Minister of Commerce, Industry and Tourism.

According to the Aeronáutica Civil de Colombia (Aerocivil), 4,483,077 passengers were transported on scheduled flights in February 2026, a 9.4% increase compared to the same month of the prior year. International arrivals grew 11.9% while domestic traffic increased 7.3%.

Between January and February 2026, scheduled flights moved 9,906,749 passengers, an 8.2% increase over the same period in 2025. The figures reflect ongoing expansion in commercial aviation capacity into Colombian airports, including the principal international gateways in Bogotá, Medellín, Cartagena, and Cali.

Following Colombia’s participation as guest of honor at the Tianguis Turístico de México, the Ministerio de Comercio, Industria y Turismo signed an agreement with more than 20 Mexican airports to display the country’s “Descubre la Diversidad de Colombia, El País de la Belleza” campaign during the FIFA World Cup season.

The campaign will run in terminals operated by the Mexican federal government, including airports in Mexico City, Toluca, Tulum, and Cancún. The Mexican market represents one of the larger sources of regional intra-Latin American travel and is expected to see elevated transit volumes during the World Cup, which Mexico will co-host with the United States and Canada in summer 2026.

“Colombia is positioning itself as an increasingly visible and competitive destination in international markets. These alliances allow us to expand the country’s presence in strategic global venues, increase visitor arrivals, and continue positioning tourism as an engine of economic development for the regions,” Morales Rojas said.

The ministry indicated that Colombia’s presence at the Tianguis Turístico also produced bilateral conversations on expanding air connectivity and promotional cooperation with Mexican tourism operators, though specific route announcements or carrier commitments tied to the agreement were not disclosed.

Above photo: Mexico pavilion at the 2015 ANATO Vitrina Turistica trade show in Bogotá (photo: Loren Moss)

Ecopetrol S.A. (NYSE: EC, BVC: ECOPETROL) reported first-quarter 2026 consolidated revenues of 28.6 trillion COP, a decline of 8.7% from 31.4 trillion COP in the year-earlier period, as lower crude oil prices and reduced hydrocarbon production compressed the top line for Colombia’s state-controlled oil and gas company. Against that backdrop, a marked recovery in refining margins and disciplined cost management lifted EBITDA by 1.5% to 13.5 trillion COP, yielding a 47% EBITDA margin and partially offsetting the revenue headwind. At the Q1 2026 average exchange rate of approximately 3,700 COP per USD, the quarter’s revenues translate to roughly $7.73 billion USD and EBITDA to approximately $3.65 billion USD.

Embattled Ecopetrol CEO Ricardo Roa was appointed to the position by Colombian President Gustavo Petro after managing his political campaign. (photo: Ecopetrol)

Net income for the quarter reached 2.9 trillion COP (approximately $784 million USD), down 7.7% year-over-year, reflecting the combined drag of lower revenues, a sharply elevated effective tax rate of 37.1%, and a one-time charge of 1.2 trillion COP for the impuesto al patrimonio — Colombia’s government-mandated wealth levy on large corporations established to fund post-disaster reconstruction measures. The company is also subject to a 10% income tax surcharge applicable for fiscal year 2026, which is embedded in the reported effective rate. The aggregate tax burden absorbed a disproportionate share of operating improvement relative to prior periods, limiting the flow-through of refining gains to the net income line.

Total hydrocarbon production averaged 725.2 thousand barrels of oil equivalent per day (kboed) in Q1 2026, below the 745 kboed recorded in the 2025 annual average cited by management during the March 2026 general shareholders’ meeting. Domestic crude output represented the largest component at approximately 520 thousand barrels per day (kbd). Ecopetrol’s Permian Basin operations in the United States contributed 91.8 kbd, underscoring the continued strategic importance of the international segment. Gas production continued a multi-year declining trend that poses a medium-term domestic supply challenge; management has sought to address this partially through regasification capacity additions at Puerto Bahía and on the Pacific coast, expected to come online in the second half of 2026 with a combined contribution of up to 430 billion BTU per day.

The refining segment delivered the quarter’s most pronounced operational outperformance. Ecopetrol’s domestic refineries, led by Refinería de Cartagena, processed 417.5 kbd of crude throughput. The integrated refining margin rose to $17.3 USD per barrel, a 60% improvement over the same quarter of 2025, driven by favorable differential pricing between domestic crude benchmarks and refined product values alongside ongoing operational efficiency improvements. The Comisión de Regulación de Energía y Gas (CREG) and the Ministerio de Minas y Energía remain central to the regulatory framework governing downstream margins over the medium term.

The balance sheet carries significant structural and contingent risk items of direct relevance to institutional credit and equity holders. Gross debt stood at 108.1 trillion COP (approximately $29.2 billion USD), representing a leverage ratio of 2.3 times trailing EBITDA — a level that leaves limited room for further deterioration before debt covenants or rating agency thresholds become binding. Ecopetrol holds a receivable of 4.2 trillion COP (approximately $1.14 billion USD) from the Fondo de Estabilización de Precios de los Combustibles (FEPC), a government fuel price stabilization mechanism that represents a claim on the Colombian treasury with timing and recovery risk. A dispute with the Dirección de Impuestos y Aduanas Nacionales (DIAN) over value-added tax assessments totals 12.26 trillion COP (approximately $3.31 billion USD) in aggregate, of which 10.22 trillion COP relates to Ecopetrol’s consolidated operations and 2.04 trillion COP to Refinería de Cartagena. Both cases are under administrative and judicial review; no provisions have been recognized in the financial statements pending resolution, but the potential liability represents a material contingency relative to the company’s quarterly net income.

On the corporate development front, Ecopetrol disclosed three significant transactions during or following the quarter. The company agreed to acquire producing assets from Gran Tierra Energy (NYSE: GTE, TSX: GTE) for $92.4 million USD, adding Colombian upstream production inventory in basins where both companies have operated. In Brazil, Ecopetrol launched a tender offer for shares of Brava Energia (BVMF: BRAV3) at 23 BRL per share, seeking to expand its footprint in that country’s oil and gas sector. And in a transaction that would reshape the mid-size independent landscape in Colombia, the company reached an agreement to acquire Parex Resources (TSX: PXT) for $250 million USD; Parex is a Colombia-focused producer with a complementary asset base across the Llanos and other producing basins. Collectively, the three transactions signal that Ecopetrol’s capital allocation strategy under the current government continues to favor upstream consolidation despite the elevated leverage profile.

The exploration portfolio generated positive news announcements. The Copoazú-1 exploratory well, drilled in Colombia’s Llanos foothills region, was confirmed as a commercial discovery, adding to the domestic reserve base. The Sirius offshore project advanced through the Consulta Previa process — a legally mandated prior consultation with indigenous and Afro-Colombian communities required before development of projects in or near their territories — reaching a milestone in community engagement that brings the project closer to formal development sanction. The Agencia Nacional de Hidrocarburos (ANH) oversees the licensing framework within which both projects operate.

“Ecopetrol is listed on the New York Stock Exchange; we are governed by the strict regulations of US federal agencies. Agencies like OFAC and the SEC could intervene in the company and could even accelerate the payment of financial obligations, which would be extremely grave for Ecopetrol.” — Martín Ravelo, President, Unión Sindical Obrera (USO)

The ISA transmission segment, managed through Ecopetrol’s majority stake in ISA — Interconexión Eléctrica S.A., contributed stable regulated cash flows during the quarter. ISA completed 46 transmission reinforcement works across its Latin American concession portfolio. The segment also completed the acquisition of 100% of IE Madeira in Brazil, consolidating its position in that country’s power grid interconnection infrastructure. ISA further submitted a competitive bid for the Río Bueno–Puerto Montt high-voltage transmission line concession in Chile, demonstrating the group’s appetite for long-duration, inflation-linked infrastructure assets across the Andes region. For institutional investors evaluating Ecopetrol as a blended hydrocarbons-and-infrastructure holding, ISA’s consistent cash generation provides partial diversification from crude price volatility, though it does not insulate the consolidated entity from headline governance risk.

The most consequential variable for the investment thesis over the near term is Ecopetrol’s prolonged governance crisis. At the company’s general shareholders’ meeting on March 27, 2026, held at the Corferias convention center in Bogotá, minority shareholders loudly heckled president Ricardo Roa — with audible shouts of “¡Fuera, fuera!” reverberating through the hall — as debate over his leadership erupted into open confrontation. The meeting approved a dividend of 121 COP per share for minority holders and a 4 trillion COP distribution to the Colombian government as majority shareholder, payable in two installments by June 30, 2026. Despite the financial business conducted, governance overshadowed the proceedings.

Roa faces two separate judicial proceedings. The Fiscalía General de la Nación formally charged him in connection with alleged influence peddling related to the purchase of an apartment in northern Bogotá — charges he has denied. Separately, the Consejo Nacional Electoral (CNE) is examining whether campaign spending limits were violated during President Gustavo Petro’s 2022 presidential campaign, which Roa managed — an investigation that Finance Colombia has covered in detail. Angela Maria Robledo, Chair of the Board of Directors, defended the board’s decision to retain Roa at the March assembly, citing the constitutional presumption of innocence. However, four of the nine board members had already formally recorded their support for his removal at that point, exposing a divided governance structure at a time when strategic and operational decisions require unified leadership.

The Unión Sindical Obrera (USO), which represents approximately one-third of Ecopetrol’s workforce, issued a production strike ultimatum timed to a March 30 board meeting. Martín Ravelo, president of the USO, framed the leadership crisis explicitly in terms of US regulatory risk: “Ecopetrol is listed on the New York Stock Exchange; we are governed by the strict regulations of US federal agencies. Agencies like OFAC and the SEC could intervene in the company and could even accelerate the payment of financial obligations, which would be extremely grave for Ecopetrol.” Ravelo further warned that the company’s outstanding international debt — which he placed at approximately $30 billion USD and which is exacerbated by elevated interest rates — left Ecopetrol exposed to potential covenant triggers or early repayment demands in a scenario where the Securities and Exchange Commission (SEC) or the Office of Foreign Assets Control were to take enforcement action.

Following sustained pressure from the USO, minority shareholders, and opposition political figures, Ecopetrol’s board approved an extended leave of absence for Roa beginning April 7, 2026. Under the arrangement, Roa used accrued vacation through May 27, followed by 30 calendar days of unpaid leave beginning May 28, extending his absence through the end of June — a period encompassing Colombia’s presidential first round on May 31 and a potential runoff on June 21. Juan Carlos Hurtado Parra, the company’s executive vice president of hydrocarbons and designated first alternate to the presidency since November 2025, was appointed acting president. Hurtado Parra holds an MBA in International Oil and Gas and brings more than 28 years of energy sector experience to the acting role, having previously served as vice president of exploration, development, and production.

The political calendar creates a structural transition risk that sits above the operational and financial results as the primary concern for long-duration investors. Colombia’s incoming government, to be inaugurated August 7, 2026, is widely expected to appoint a new Ecopetrol board and select a new company president. That transition may bring material shifts in strategic priorities — including the pace of upstream investment, the approach to the FEPC receivable recovery, the trajectory of energy transition spending, and the capital allocation balance between the hydrocarbons segment and the ISA infrastructure platform. The Ministerio de Hacienda y Crédito Público and the Ministerio de Minas y Energía will both play key roles in establishing the post-election policy framework under which Ecopetrol operates. Institutional investors holding exposure to Ecopetrol via NYSE: EC or BVC: ECOPETROL must weigh Q1’s genuine operational improvement — most visibly in refining margins and EBITDA stability — against a governance and policy transition risk profile that is unlikely to be resolved before the August handover.

Ecopetrol’s Cartagena refinery (photo courtesy Ecopetrol)

Tecnoglass, Inc. (NYSE: TGLS) reported first-quarter 2026 revenue of $249.0 million USD, a 12.0% year-over-year increase and a first-quarter record for the Barranquilla, Colombia-based window and architectural glass manufacturer. Despite the top-line growth, net income fell to $31.9 million USD, or $0.71 per diluted share, from $42.2 million USD, or $0.90 per diluted share, in the same period of 2025, as elevated US aluminum costs linked to import tariffs, mandatory minimum wage increases in Colombia, and a strengthening Colombian peso combined to compress gross margins by 540 basis points to 38.5%.

Multi-family and commercial revenues rose 20.4% year-over-year, driven by continued activity across key markets including geographies beyond Florida, which has historically dominated the company’s US revenue mix. Single-family residential revenues were relatively flat on a year-over-year basis, with management attributing the result to the timing of order conversion into revenue rather than underlying demand, noting that order growth in the segment remained positive into April 2026. On a geographic basis, the US accounted for $237.1 million USD, or approximately 95% of total revenues, up 11.6%. Colombia generated $7.5 million USD, up 17.2%, and other international markets contributed $4.4 million USD, up 27.3%.

Gross profit declined to $95.8 million USD from $97.5 million USD in Q1 2025 despite the higher revenue base. The company cited an unfavorable revenue mix driven by a greater proportion of installation-related revenue, higher raw material costs — with US aluminum tariffs representing an incremental headwind of approximately $6.4 million USD in the quarter — higher salary expenses resulting from annual minimum wage adjustments in Colombia, and the effect of a stronger Colombian peso on costs incurred locally. Pricing actions and operating leverage on higher volume partly offset these pressures.

“We see a clear path to fully offsetting the impact of tariffs in 2027, when full-year pricing across both businesses and incremental automation savings are expected to be realized.” — Santiago Giraldo, Chief Financial Officer, Tecnoglass

Selling, general, and administrative expenses rose to $50.9 million USD, or 20.4% of revenues, from $42.5 million USD, or 19.1%, in Q1 2025. The increase reflected higher personnel costs from annual salary adjustments, peso appreciation, and higher transportation and commission costs tied to revenue growth. The period also included a one-time charge of $2.9 million USD related to Colombia’s *impuesto al patrimonio*, a government-imposed wealth tax levied on large corporations to fund measures addressing recent climate-related events in the country.

Adjusted EBITDA — which excludes non-cash foreign exchange gains and losses, the bad-debt provision, non-recurring charges, and equity-method adjustments related to the company’s joint venture in Vidrio Andino with Saint-Gobain (EPA: SGO) — came in at $61.5 million USD, or 24.7% of total revenues, compared to $70.2 million USD, or 31.6%, in Q1 2025. Adjusted net income was $34.6 million USD, or $0.78 per diluted share, versus $43.1 million USD, or $0.92, in the prior-year quarter.

Cash provided by operating activities was $6.7 million USD, a significant decline from $46.9 million USD in Q1 2025, driven in part by a deliberate build-up of US-sourced aluminum inventories — up $34.3 million USD in the quarter — as part of the company’s tariff mitigation strategy. Capital expenditures of $17.3 million USD reflected scheduled payments tied to previously announced capacity and automation projects. During the quarter, Tecnoglass returned $16.5 million USD to shareholders through share repurchases and paid $6.7 million USD in cash dividends. As of May 7, 2026, approximately $92.5 million USD remained available under the current share repurchase program. The company ended the quarter with total liquidity of approximately $425.0 million USD, comprising $91.1 million USD in cash and cash equivalents and more than $330.0 million USD in revolving credit facility availability, against total debt of $200.3 million USD.

The company’s order backlog reached a record $1.36 billion USD at quarter-end, up 19.1% year-over-year, extending multi-family and commercial pipeline visibility into 2027. Tecnoglass cited continued expansion of its dealer network and showroom footprint as supporting geographic diversification and market share gains, with vinyl product lines identified as an incremental growth driver broadening the company’s addressable market.

José Manuel Daes, chief executive officer, commented on the results: “First quarter results were in line with our expectations, with resilient performance across our key metrics reflecting the continued strength of our vertically integrated business model despite a dynamic cost environment. Demand for our product offerings remains strong, as demonstrated by another quarter of record backlog and healthy order activity, with momentum continuing into the second quarter. Our previously announced pricing actions are now in place, and the broad-based nature of industry cost pressures supports our confidence in executing these increases while preserving our competitive positioning.”

Christian Daes, chief operating officer, addressed the tariff response and the company’s assessment of a potential US manufacturing presence. “Our pricing initiatives and cost mitigation efforts are well underway, including logistics improvements, further automation across our operations, and ongoing supply chain optimization,” he said. “We are also advancing our assessment of a proposed US manufacturing initiative, with a well-located site identified and significant state and local incentives secured that strengthen the project’s potential economics if we decide to move forward based on market demand.”

Santiago Giraldo, chief financial officer, reaffirmed full-year 2026 guidance and outlined the company’s tariff offset timeline. “Based on our strong execution to start the year, we are reiterating our full year revenue outlook in the range of $1.06 billion to $1.13 billion USD and Adjusted EBITDA outlook in the range of $225 million to $245 million USD,” Giraldo said. “This reflects the impact of the recently implemented 10% tariff on finished aluminum window imports as previously disclosed, which is expected to be partly offset in 2026 through pricing actions effective on orders from early May forward, with additional efficiency initiatives from logistics optimization and automation underway and expected to begin contributing benefits by year end. We see a clear path to fully offsetting the impact of tariffs in 2027, when full-year pricing across both businesses and incremental automation savings are expected to be realized.”

On the corporate structure front, Tecnoglass’ board of directors has approved a plan to redomicile the company from the Cayman Islands to the United States, subject to shareholder approval. If approved, the redomiciliation is expected to be completed during Q2 2026. The company stated that the move is intended to simplify its organizational and regulatory structure, improve the tax efficiency of dividend distributions, and expand its potential investor base to include funds and accounts limited to US-domiciled securities. Tecnoglass will retain its Miami, Florida headquarters following the change.

Separately, the company is conducting a feasibility study for a potential new US manufacturing facility. A site meeting project specifications has been identified and substantial state and local tax credits have been secured. The proposed facility is described as highly automated and intended to support future growth while also improving lead times, reducing transportation costs for certain markets, enhancing supply chain efficiency, and enabling the company to compete for Buy America-eligible projects and rapid-turnaround contracts. Tecnoglass expects to complete the purchase of land for the potential facility during Q2 2026, at an estimated cost of $20 million to $25 million USD to be financed through available credit facilities. The company noted that the land purchase does not constitute a commitment to proceed with construction, which would occur in phases contingent on demand, market conditions, and return profiles. The company’s 5.8-million-square-foot vertically integrated manufacturing complex in Barranquilla, Colombia, would continue to serve as its primary production base.

Above photo: Tecnoglass facilities in Barranquilla

Colombia’s gross domestic product expanded 2.2% in the first quarter of 2026 compared to the same period of 2025, surpassing prevailing market estimates, according to data released May 16 by the Departamento Administrativo Nacional de Estadística (DANE) and presented by the Ministerio de Comercio, Industria y Turismo. The results reflected positive performance across production, industry, and domestic commerce.

The manufacturing sector was among the quarter’s strongest contributors, posting year-over-year growth of 2.9% and adding 0.3 percentage points to the annual variation in GDP. The sector’s performance placed it among the primary drivers of national economic output for the period.

Within manufacturing, two subsectors recorded particularly pronounced gains. Motor vehicle production expanded 27.8% year-over-year, while metallurgy grew 6.6%. Both categories function as inputs to broader industrial supply chains, and their recovery carries implications for upstream and downstream productive linkages, including employment in skilled manufacturing roles.

“What is notable about the first-quarter results is not solely the magnitude of the growth, but its composition. The performance of sectors such as motor vehicles, metallurgy, and machinery is particularly significant because it demonstrates a recovery of industrial capacities with greater effects on productive linkages, skilled employment, and economic sophistication.” — Diana Marcela Morales Rojas, Minister of Commerce, Industry, and Tourism of Colombia

Separate monthly data from statistical agency DANE’s índice de producción industrial (IPI) showed that real industrial output grew 3.9% in March 2026 compared to March 2025. The expansion was distributed across multiple subsectors, including motor vehicles, metallurgy, machinery and equipment, chemicals, pharmaceuticals, rubber, plastics, and non-metallic minerals, indicating that the manufacturing recovery was not concentrated in a single production category.

Wholesale and retail trade expanded 6.0% in the first quarter, reflecting increased domestic market activity and business commerce. The trade sector’s performance complemented the manufacturing gains and contributed to the overall breadth of the quarter’s expansion.

Not all sectors contributed positively. Construction contracted 5.4% compared to the first quarter of 2025, the weakest result among major economic categories for the period. Public administration, defense, social security, education, and health services grew 5.7%, and reporting by Colombian media citing DANE data indicated that public spending accounted for approximately 46% of total first-quarter growth — a concentration that introduces a structural caveat to the headline figure, as private-sector momentum remains uneven across the economy.

Diana Marcela Morales Rojas, minister of the Ministerio de Comercio, Industria y Turismo, addressed the composition of the results in a statement issued alongside the data release. “What is notable about the first-quarter results is not solely the magnitude of the growth, but its composition,” she said. “The recovery of manufacturing, metallurgical, and industrial production activities demonstrates a greater role for sectors associated with transformation, productive capacity, and value-added generation within the national economic dynamic. The performance of sectors such as motor vehicles, metallurgy, and machinery is particularly significant because it demonstrates a recovery of industrial capacities with greater effects on productive linkages, skilled employment, and economic sophistication. These are meaningful indicators of strengthening of the manufacturing structure and national production.”

The first-quarter data were released as Colombia continues to manage elevated monetary policy rates and fiscal pressures that have weighed on investment activity in recent quarters. The Ministerio de Comercio, Industria y Turismo indicated that the quarter’s results reflect progress on an agenda oriented toward strengthening industry, domestic production, and commercial activity, though the degree to which private-sector industrial recovery can sustain these gains independently of public spending remains a key variable for subsequent quarters.

Headline photo credit: Tecnoglass